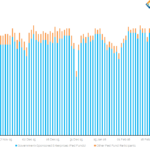

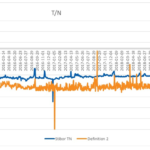

SOFR Fixed at 5.25%. What happened to the volumes?

We are all repo traders now. SOFR has been volatile in the past week fixing from 2.20%, 2.43%, 5.25% (!) before back to 2.55% yesterday. We analyse the volumes that make up the fixing and the SOFR IRS volumes. For those that missed it, SOFR fixed at a scarcely believable 5.25% on 17th September. Surrounding […]

Four Things to Understand about USD SOFR

USD SOFR is made up of both general collateral (GC) and non-GC trades. Recent data suggests that there is a difference (a “basis”) between GC and non-GC repo trades. USD SOFR combines Dealer to Dealer and Dealer to Customer trades. Only a limited history of SOFR is available. USD SOFR Components The transactions that make […]

USD Fed Funds and the FHLBs

Get ready to geek out on some short-end USD Rates background. Fed Funds Fed Funds (as I know it), or the more official sounding “Effective Federal Funds Rate (EFFR)”, is a key overnight interest rate for USD. It didn’t quite cut the mustard as the official Risk Free Rate though – that title goes to […]

‘Dear CEO’ letters – Customer Impacts

Last month I wrote a blog that described the ‘Dear CEO’ letters sent to many financial firms from regulators in UK, EU, Switzerland, Australia and Hong Kong. Also the US FED has added a Libor component to their regular supervisory requirements to assess the transition from Libor to other benchmarks for firms they supervise. In […]

The ‘Dear CEO’ letters – a time to accelerate preparations

Several regulators and central banks have written to the CEOs of firms in their jurisdictions to emphasise the fact that Libor cessation is very real. In most cases (UK, EU, Switzerland and Australia) a written, often board-approved response is required. In other cases, the response is left open (USA, HK and Singapore) and firms were […]

ARRC Vendor Workshop June 28, 2019

The Alternative Reference Rates Committee (ARRC) hosted a vendor workshop recently at the Federal Reserve Bank of New York, which I attended and in this article I cover some of the key points from the workshop. Required SOFR interest rate characteristics Required trade economics and processing for SOFR-based derivatives and cash instruments Compound in arrears […]

Term Risk Free Rates from FX Forwards

The case for a Term Risk Free Rate (TRFR) to support the transition of cash instruments and products has been made by BoE and US ARRC over the past year. The TRFR is defined as a rate known in advance (similar to the current Libors) but based on RFRs in the relevant currency.

But the issue of how to construct an IOSCO-compliant TRFR has been a challenge for market participants and benchmark administrators.

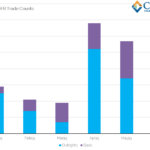

USD SOFR Volumes June 2019

SOFR traded notional hit $50bn in monthly notional for the first time. We take a look at the details of some of the block trades that drove this notional higher. LCH data shows that the amount of risk traded has been between $4m and $10m DV01 during May and June. We show how our data […]

SEK STIBOR Reform

The Swedish Banker’s Association is looking to introduce an Alternative Reference Rate for SEK markets. At the moment, STIBOR is the underlying index for SEK swaps. There are on-going consultations to introduce a Risk Free Rate in Swedish markets. We take a look at the details. SEK Markets Today As it stands today, there are […]

Mechanics and Definitions of Singapore Benchmark Rates (SGD SOR and SGD SIBOR)

Singapore has unique benchmark interest rates. SOR is an FX-derived synthetic SGD interest rate from FX swaps. SOR will therefore be impacted by changes to USD LIBOR as a result of the latest ISDA consultation. Cross Currency in SGD trades versus the SOR index. Why isn’t the basis therefore zero? Singapore Interest Rates In response […]