SOFR Market Developments

Last month I wrote about SONIA market developments and how trading is progressing ahead of 2022 when Libor is expected to end. In this blog I extend this analysis to the USD markets. Much like SONIA, SOFR has seen some growth over the past year, which is to be expected as USD Libor is also […]

Mechanics and Definitions of ISDA IBOR fallbacks

If an ‘IBOR rate, e.g. USD LIBOR, ceases to publish, we now know the exact methodology that will be used in derivatives contracts to calculate a replacement rate. The calculation uses compounded in-arrears Risk Free Rates, which are decided at a currency level. A spread will be added to these compounded rates, which will be […]

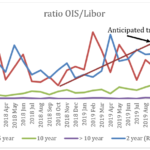

SONIA Term Rates – which is best?

Four providers have entered the race to provide term SONIA fixings. These terms fixings are intended to ease the uptake of SONIA and made the transition easier for end-user cash markets. The providers are LSEG, ICE, Refinitiv and Markit. We look at their proposals. Looking at the SDR data we find that 80% of SONIA […]

SOFR Discounting for Cleared Swaps

CME and LCH propose to change USD Swaps discounting and Price Alignment Interest (PAI) from Fed Funds (EFFR) to SOFR on October 17th 2020. By creating SOFR discounting risk from that date, this change should result in a need to hedge SOFR risk and drive increased liquidity as well as extend the tenors of SOFR Swaps […]

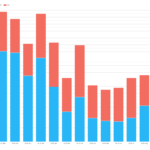

SONIA Market Volumes – What is Going On?

SONIA has seen some growth over the past year or so which we expected. Edwin Schooling Latter, Director of Markets and Wholesale Policy at the FCA in January 2019 and Andrew Bailey, Chief Executive Officer at the FCA in July 2019, both commented on the growth of SONIA derivatives markets. In summary the market volume […]

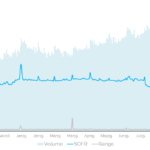

What does SOFR volatility mean for LIBOR Fallbacks?

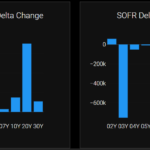

SOFR fixings have exhibited an elevated level of volatility in recent weeks. We look at the impact this may have on LIBOR fallback spreads for 1 month USD LIBOR. We use our IBOR Transition Management apps that we recently announced. The data shows that there are sustained periods where the realised spread has been negative, […]

CAD Rates Markets and CORRA Reform

Canadian Rates markets look to be in an especially strong place from a market infrastructure viewpoint. CAD IRS trades versus a term rate, CDOR, which is based on real quotes from six panel banks. The underlying market for CDOR, Banker Acceptances, is a growing market of significant size (CAN$85bn outstanding). Meanwhile, OIS trading vs CORRA […]

Tools for IBOR Transition Management

Today we put out the press release, Clarus Financial Technology releases IBOR Transition Management Tools and in this blog I wanted to provide more details on our offering. Before I do that, another point to note is that we recently authored a whitepaper with our friends at Finastra, titled “IBOR Transition Made Simple“, which is […]

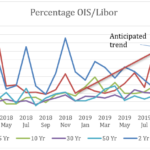

ISDA September 2019 Consultation on Final Parameters

The final piece of the LIBOR-cessation puzzle is about to be completed. We’ve previously looked at how RFRs can be used to replace a range of ‘IBOR indices. Now we look at the exact parameters that will be used to calibrate the ‘IBOR- RFR spreads. Historic Calibration Market consultations from ISDA have led to the […]

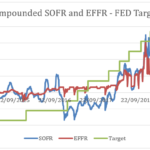

SOFR and FedFunds Rate Comparisons

SOFR has been topical for over a year as markets become more used to the near-new USD Risk Free Rate (RFR). The ARRC identified SOFR as the preferred replacement for USD Libor in 2017 and has stated: ‘The ARRC has identified the Secured Overnight Financing Rate (SOFR) as the rate that represents best practice for […]