A short while ago I saw the letter written by Javelin to the CFTC regarding MAC swaps and margin. The press release can be found here. My brief synopsis:

- Swap futures are equivalent (in terms of risk) to cleared OTC MAC contracts

- Swap futures enjoy 2-day VaR margining (SPAN or SPAN like)

- OTC MAC contracts are more expensive to carry, given the 5-day VaR treatment

- Despite the reduced cost to carry futures, the deeper liquidity remains in OTC MAC (and other IMM)

- The margin imbalance is not justified and is a detriment to SEF order books

- In order to promote fairness and SEF activity (particularly in an order book), OTC MAC contracts (and some other specific IMM) should be margined the same as Swap futures (2-day VaR)

- Javelin formally requests the CFTC order a reduction in the liquidity period to 1 day (which leads to the 2-day VaR)

ARE THEY REALLY EQUIVALENT?

Equivalency. That’s a loaded question. This needs to be broken down.

Generally speaking, the swap futures contracts in the Americas indeed resemble an OTC MAC swap. That is:

- The start dates are IMM

- The maturity of the futures are fixed tenors. Futures are the liquid 2, 5, 7, 10, 30 year, OTC MAC contracts include those as well as 1, 3, 15 and 20 year swaps.

- There is a common, fixed coupon

- The economics, valuation and risk characteristics, from what I can understand, are modeled to match an OTC MAC swap

Operationally of course, coupons do not get settled on the futures contract as it is nested in the price calculation. But then again, in cleared OTC, all of that coupon processing, PAI, etc is bundled into your VM flow too. Much of a muchness. The OTC world has mimicked futures processing here.

From an execution perspective, they are currently different. There are order books on OMS/EMS platforms aggregating the CME and Eris order books for swap futures. In OTC MAC swap land, I feel comfortable in guessing it’s been substantially RFQ. I will however, point out, that there have been MAC order books launched on at least 3 SEFs over the past month (as I discussed in my previous blog here) but those have not shown much activity yet.

Lastly, margin. Indeed the CME and Eris Standards (the MAC variety) are “2-day” VaR. OTC MAC swaps cleared at CME and LCH are indeed 5-day. And if you really want a sensational headline, client-cleared swaps at one of those DCO’s can be the equivalent of 7-day VaR.

WHAT IS 2-DAY VAR ?

Before we begin, let’s first understand the premise of all initial margin methodologies is that the participant needs to post enough funds to cover them for an adverse, but plausible, market movement. These funds should be adequate to allow the CCP enough time (the liquidation period) to liquidate the positions after a default. In OTC-land, the liquidation period has often been designed not as a direct liquidation but rather a hedging and auction process.

OTC HVaR margin regimes deployed the world over look at a reasonable history of market movements. Typically these observe the last 5 or 10 years worth of curves, and determine changes in this data over 5 day periods. As such, todays (Monday) 5-day returns would be computed on what happened in the market starting from last Monday’s close until tonight’s close. You have 1250 (5 years worth) or 2500 (10 years worth) of these 5-day scenarios. Revalue your portfolio for each of these scenarios, find the tail (some of the worst losses), and somewhere in there, depending upon the methodology, is your HVaR loss.

So clearly, the magnitude of your possible losses increases the longer that window (or “horizon”). 2 day horizon losses will be less than 5 day, and 5 day will be less than 7 day.

I like to think that Futures margining regimes (SPAN) back into this logic. Futures have the benefit of being standardized, so you have a finite list of contracts to evaluate. If we only have 5 contracts, we can compute some “worst case” losses for those 5 hypothetical trades/contracts, and we have effectively short-cut the HVaR model.

Futures margining begins to break down when looking at intrinsic correlations, unless they are explicitly accounted for. SPAN is very mature and hence does account for them (inter and intra commodity spreads), but it needs to be tinkered with, and regardless of how good the tinkering is, will break down when the number of contracts goes beyond a reasonable number, when the amount of correlated products grows beyond just a few, or when correlations break down.

All of this detail aside, the point is that the SPAN margining has, at its heart, a 2-day horizon baked into those scenarios and parameters.

SO WHATS THE DIFFERENCE?

I keyed a couple MAC swaps into CHARM. I chose to look at a 5YR and 30YR OTC MAC swap, cleared at either CME or LCH. Both of them 10,000,000 USD.

Any discrepancies between LCH and CME here are inconsequential. We can conclude that our OTC MAC swap will be on the order of 2% margin for the 5YR and 6% for the 30YR.

Using SPAN for the CME DSF and Eris Standard futures, we find that in both cases the 5YR is 100,000 and the 30YR is 200,000 (so 1% and 2% respectively).

Determining 2-day HVaR requires 2-day returns to be used, however in the interest of time here I will scale the 5-day VaR to a 2-day VaR, as that has been proven to be very accurate.

What this says, is that a shift to 2-day HVaR for OTC MAC contracts would indeed bring the initial margin down into the realm of Futures SPAN margin.

BUT IS THIS REAL?

So great, everyone’s margin will drop by ~ 40%, right?

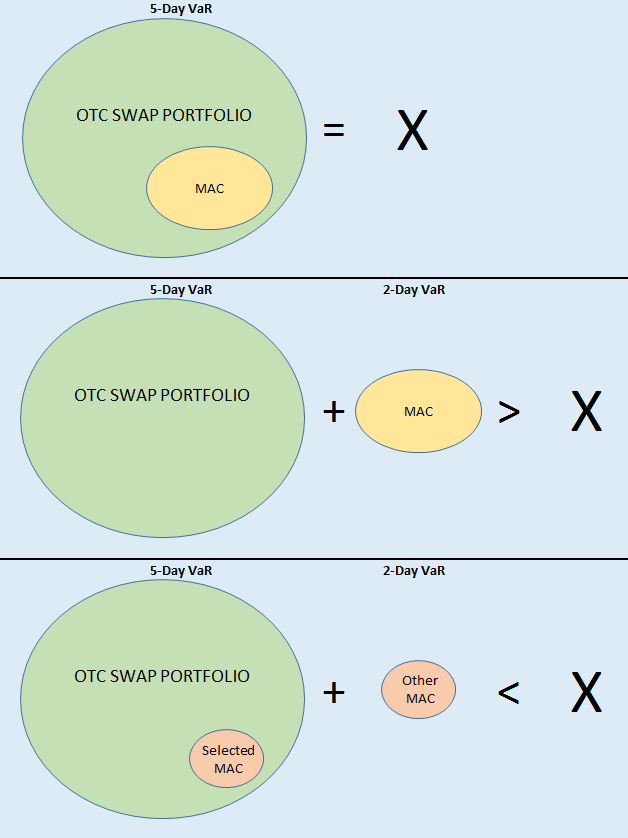

Well, not quite. That analysis is on a single trade. But it does nicely illustrate what the impact would be if your entire book was MAC swaps, or if your entire book was futures.

Having a MAC swap in a portfolio of non-MAC swaps would have the same operational burden that we see today for portfolio margining futures and OTC: you’d need to pluck out just the MAC swaps that are not already offering portfolio offsets to your other OTC products.

To support this, CME and LCH would need to have buckets for this 2-day regime. Further, they would need to offer, or the FCMs would need to offer, some way to pluck out the right swaps and stick them into the “2-day” bucket.

To illustrate this, I would offer the following. Simply putting your MAC swaps into its own bucket, granted they are 2-day VaR, would increase your margin costs.

Oddly, I would support this whole endeavor if for no other reason than this would be yet another reason participants would require our CHARM product to optimize their margin and capital. Unfortunately I don’t think maximizing Clarus’ revenue is at the top of the CFTC agenda.

YOU CATCH MORE FLIES WITH HONEY THAN VINEGAR

This whole topic rang a bell. If you recall back in April of 2013, Bloomberg also suggested that the costs of clearing OTC should be more on par with futures. The manner they went about it, however, was to bring a lawsuit against the CFTC.

This lawsuit was thrown out in June of 2013 because Bloomberg didn’t justify that it would “lose money”.

Javelin’s approach does seem more tactful.

RACE TO THE FUTURE

I recall a few years ago the talk of the “race to the bottom” in clearing. The theory was that clearing houses, in an attempt to gain business, would compete on the costs of initial margin. Logic being if DCO #1 was charging X to maintain a swap, DCO #2 would just say they’d do it for ½ X. Then when the next crisis hits, DCO #2 finds it has not collected enough margin and has one or more defaulting members, and the world falls apart again.

I’ve been pleased to find that in fact the opposite is true. FCMs do a tremendous amount of due diligence on their counterparties, and have required DCO’s to demonstrate that the margining regimes are adequate. More aggressive initial margins at a DCO do not fill FCM’s with confidence – rather they invoke images of their default fund contributions going towards the default of an over-leveraged member.

To support this proposal, the DCO’s would need to demonstrate that a default could be processed in an orderly fashion, presumably in a crisis situation, given a 2-day horizon buffer. Is there enough liquidity in MAC contracts to do this? Don’t forget though that OTC defaults tend to promote hedging of the portfolio first, and the subsequent unwind or auction can take place many days later.

Having typed that, it makes me wonder – is 5-day VaR already too long of a window for all vanilla OTC? And is 2-day (SPAN) too short a window for futures?

So I am interested to see the response from the DCO’s and FCM’s on this topic.

SUMMARY

On the surface, the proposed margining of MAC contracts makes perfect sense. Futures get it, why don’t the OTC equivalents get it.

The real winners here would be the participants that trade only, or primarily, very standardized IMM swaps. Participants with only a portion of their portfolio being standardized would not reap any benefits unless there were some optimization taking place. But perhaps that is the point – yet another carrot to move the market towards a standardized product.

If DCO’s can justify it with their risk management principles, I would be in support.

Regardless, I’m interested to see how the market reacts.

Thx for the background on where we are w/ MACs… Additionally the laughs are always appreciated 🙂

One question-

As you rightly indicated, competing over margin may raise concerns more than it will entice participants due to the assumed leverage or increased maximum potential loss scenario.. But the same is not true of the lower margin requirements for listed MAC v OTC Swap.

Do you think this line of thinking should also enter a market participants mind when they get lower IM for MACs vs the Vanilla OTC counterpart? My thinking here is, folks IM is based on the 2day VaR as opposed to the necessarily higher IM required for the ‘riskier’ 5day VaR. I also second your question about liquidity of MAC futures and their ability to truly withstand a liquidation scenario.

I feel like that was poorly worded, but you probably know what I’m getting at 🙂

I think I know what you’re getting at. I do think there are firms that could justify a swaps business if margins were lowered (and order books were active, etc, etc Chicken and the egg). I feel for the DCO’s because while they might say “sure we could default manage MAC’s with 2-day VaR” – is it commercially viable to do this (set up a new bucket for just MACs and offer optimization etc)? So arguarbly the CFTC might say sure thats ok, but the DCO’s may still not do anything about it.