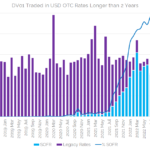

The Most Popular SOFR Trades

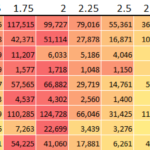

Transparency data allows us to look at the distribution of risk across the curve. We may be used to seeing activity concentrated in benchmark tenors such as 2Y, 5Y, 10Y and 30Y in US markets, but have SOFR swaps developed in a similar manner? As a starter the ISDA-Clarus RFR Adoption Indicator shows the amount […]

Most Active Names in Credit and Equity Derivatives – Jan2023

Late last year I looked at the SEC Securities Based SDRs (SBSDRs) for the Most Active Names in Credit and Equity Derivatives in Oct22, so today I will update that blog for the entity names that were most actively traded in the month of January 2023. CDS on Sovereigns Using SBSDRView, we can find the […]

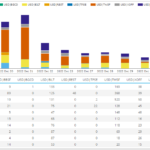

SDR – Trading Venues and Packages

Late last year, on Dec 5th, US Swap Data Repositories (SDRs) went live with CFTC’s amended swap data reporting framework (a.k.a CFTC re-write). This incorporates CPMI-IOSCO harmonised data elements (e.g. UTI and UPI) and introduces new data elements. For CFTC Part 43 public dissemination, there are two very interesting new data elements: Let’s look at […]

Most Active Names in Credit and Equity Derivatives – Oct22

Earlier this summer we looked at the SEC Securities Based SDRs (SBSDRs) for the Most Active Equity Total Return Swaps and Most Active CDS Single-names. Today I will use SBSDRView to look at which names have been most active in October 2022. CDS on Sovereigns Let’s start with the twenty most active sovereigns by trade […]

Most Active Equity Total Return Swaps

Since our First Look at Total Return Swaps blog, we have added a Most Actives view in SBSDRView. This identifies the most active stocks on which TRS are transacted and below I look at what this data shows. Number of trades The two main derivative products in SBSDRs for Equities are Total Return Swaps (TRS) […]

Most Active CDS Single-names

We recently published the blog Most Actives in CDS Trading, which covered the use of our API to access SEC SBSDR transaction data. This included python code to perform look-ups on security identifiers and build a table of the most active names traded in a given period. While simple enough to do for those with […]

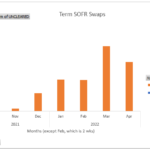

BSBY and Term SOFR Swap Volumes Update

In Feb 2022, I looked at BSBY and Term SOFR Swap Volumes, so today is an update for March and April. Term SOFR Using SDRView, exporting USD FixedFloat Swaps (so not OIS), filter on Term SOFR Reference Indices. The number of trades in a month increasing from: <10 in Oct 2021 342 in Dec 2021 603 […]

A First Look at Total Return Swaps

We are now getting our hands dirty with new public transparency data. Amir has covered this in a couple of blogs recently, and I have also used the Russian Federation CDS data from SBSDRs. For this blog, we’ll look in more detail at Total Return Swap data for Equities. What Is a Total Return Swap? […]

SBSDR – A look at Equity Total Return Swaps

Following on from my blog, SEC Security-Based Swap Data Repositories Are Now Live, I wanted to take a look at Equity Total Return Swap volumes. OTC Equity Derivatives (USD) Let’s start by using SBSDRView to see the products and volumes reported for trades denominated in USD. TRS with @ 70,000 trades on each of Apr 6, […]

Swaption Volumes by Strike Q1 2022

Swaptions activity has reacted to the huge sell off we have seen in Fixed Income markets during Q1 2022. There are no volume records being broken in Swaptions but we update one of our popular blogs from 2021 with fresh data. We take a look at Swaption strikes traded throughout the quarter. And we break-down […]