- Q4 2020 saw $7.0bn DV01 of new USD-LIBOR* linked activity written in OTC derivatives markets.

- It is a similar story in GBP ($4.5bn DV01), JPY and CHF markets.

- Why is so much new risk being written against these indices when they are due to cease imminently?

- Responses to the IBA consultation on a possible cessation of LIBOR are due on the 25th January 2021. We expect market participants to highlight this continued new risk generation.

- Market participants should look to incorporate Clarus data to explain how it fits into their transition efforts.

*includes a small amount of Fed Funds risk generated in the quarter.

IBA Consultation on the Cessation of LIBOR

For those of you responding to the key LIBOR consultations from ICE Benchmark Administration (IBA), here is a run-down of the consultation itself:

Deadline

Deadline for consultation responses: 17:00 LDN Monday January 25th 2021.

Currency Specific Content

LIBOR fixings cover 7 tenors in each of 5 currencies, making up 35 specific fixings in total. Here is what IBA said about each specific LIBOR currency:

EUR LIBOR: This is the least used of the LIBOR currencies, as most EUR contracts reference EURIBOR instead. Outreach by IBA has shown “little support” for the continuation of EUR LIBOR and an “insufficient number” of banks have communicated an intention to “continue contributing” to EUR LIBOR after end-2021.

CHF LIBOR: There is a “particularly low activity” in actual transactions making up CHF LIBOR fixings, meaning panel banks rely on “expert judgement”. Again, an “insufficient number” of panel banks intend to contribute after end-2021.

JPY LIBOR: In a similar state to CHF, panel banks rely on “expert judgement” for their contributions. IBA specifically asked JPY LIBOR panel banks to “consider providing JPY LIBOR submissions for a temporary extension period beyond end-2021.” However, an “insufficient number of banks” intend to contribute after end-2021.

GBP LIBOR: IBA also asked banks to consider a temporary extension period of GBP submissions. In the same vein as JPY, although possibly also linked to the “FCA enhanced powers” an insufficient number of banks intend to do so.

IBA are therefore consulting on the intended cessation of all EUR, CHF, JPY and GBP LIBOR tenors.

USD LIBOR: It looks like panel bank willingness to continue contributing to USD LIBOR is much higher than in other currencies. IBA believe that a sufficient number of panel banks intend to contribute to USD LIBOR until June 30 2023 in each of the Overnight, 1, 3, 6 and 12 month tenors. This means that IBA are consulting on the intended cessation of 1 week and 2 month USD LIBOR tenors at end-2021. Importantly, IBA believes there will be a “representative panel” for the continuation of other tenors. All other tenors in USD LIBOR are therefore intended to cease on June 30 2023.

Consultation Question

As is the way with these consultations, the posed questions to the market finally come to the fore on page 16, after a lot of carefully worded content. This is actually pretty concise compared to other consultations we work on, so our compliments to IBA for saving us some time!

The question posed by the consultation is very clear:

IBA requests feedback from stakeholders on its intention to cease publication of [specific LIBOR fixings] after Friday December 31st 2021 and after Friday June 30 2023 for USD LIBOR overnight, 1, 3, 6 and 12 month fixings.

That’s it. A single question!

Responding to the Consultation

Consultation responses like this one can be quite open-ended! We would have been happier if IBA had made some specific data-related requests. We have found that responses to consultations such as these receive far more attention when they are backed up with data, not anecdotes. When the responses are made public, we expect to see some public data for the first time on the industry’s efforts to transition legacy portfolios.

Some data on net LIBOR risk outstanding, for example, would be very helpful. As would overall gross transition efforts on legacy portfolios.

In terms of new risk, we believe that derivatives markets continue to be the largest generators of new LIBOR-based risk. This is why we created the ISDA-Clarus RFR Adoption Indicator, to track both how much risk is traded as an RFR, but to also monitor new activity linked to LIBOR.

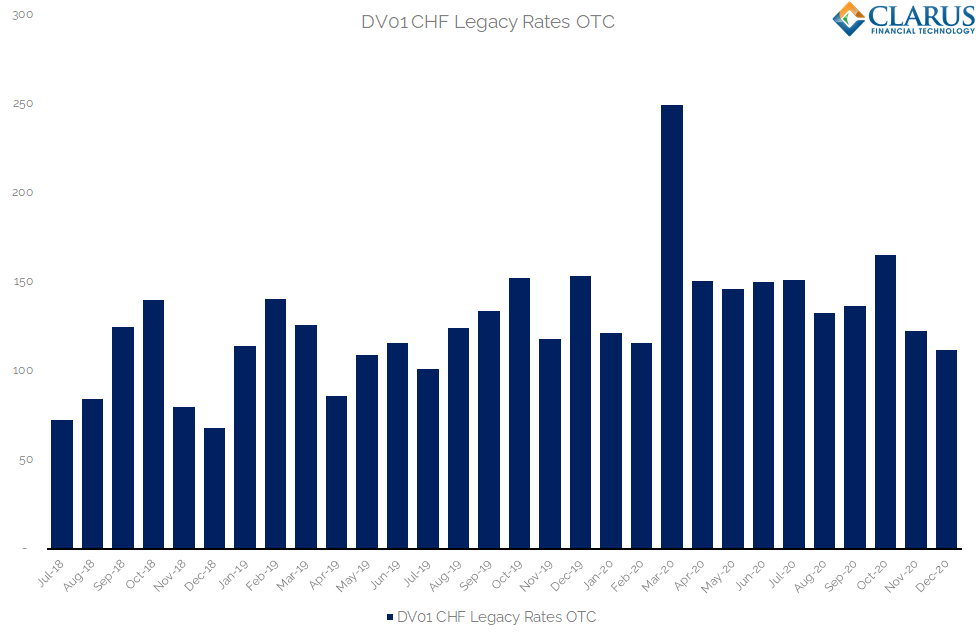

Clarus Data: CHF LIBOR

As we work to finalise the December 2020 version of the ISDA-Clarus RFR Adoption Indicator, we can share some preliminary data below.

For example, this is how much new CHF LIBOR risk has been traded each month:

Showing;

- The RFR Adoption Indicator normally focuses on the numerator – how much RFR risk is trading each month?

- However, we also have the data for the denominator of the equation – i.e. how much total risk, including versus legacy rates, is being transacted.

- The chart above shows only OTC volumes. Let us assume that Futures (ETD) volumes can be more easily transitioned using rulebook changes.

- For CHF markets, the amount of new CHF LIBOR risk transacted in Q4 2020 was within ~5% of the amount of CHF LIBOR risk transacted in Q4 2019 ($420m equivalent versus $425m last year).

- Even in a small market like CHF, $400m in DV01 each quarter is a hell of a lot of risk being transacted versus an index that is at risk of cessation.

As part of consultation responses, we expect market participants to highlight this. It would be extremely helpful if they could explain why this is the case. What proportion of this new LIBOR risk is being transacted as part of transition efforts? What proportion of client trades are SARON and what proportion are CHF LIBOR? Same for interbank business? Platforms such as Tradeweb, Bloomberg and the IDBs should be sharing this data as part of these consultation responses.

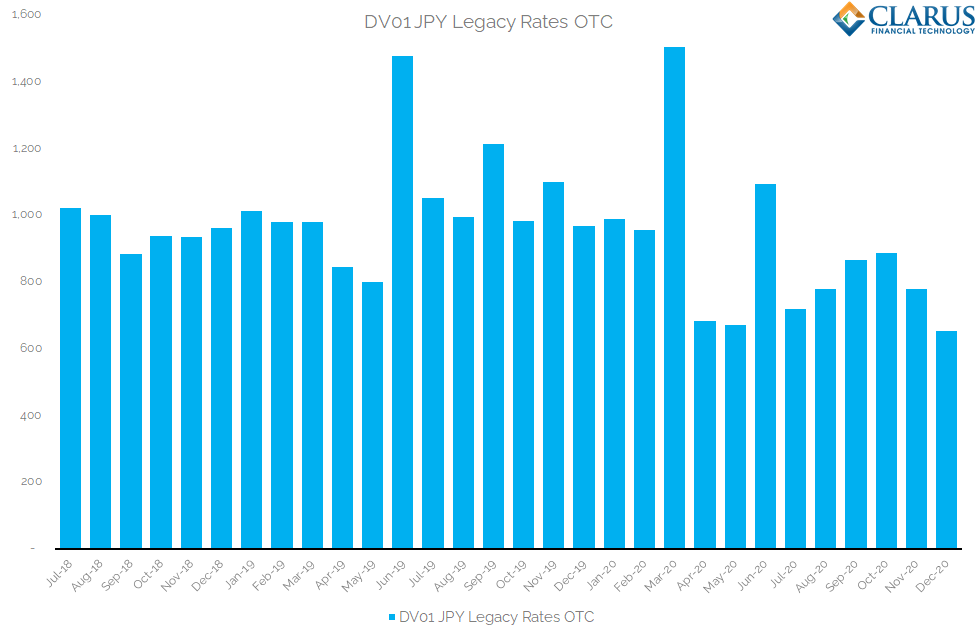

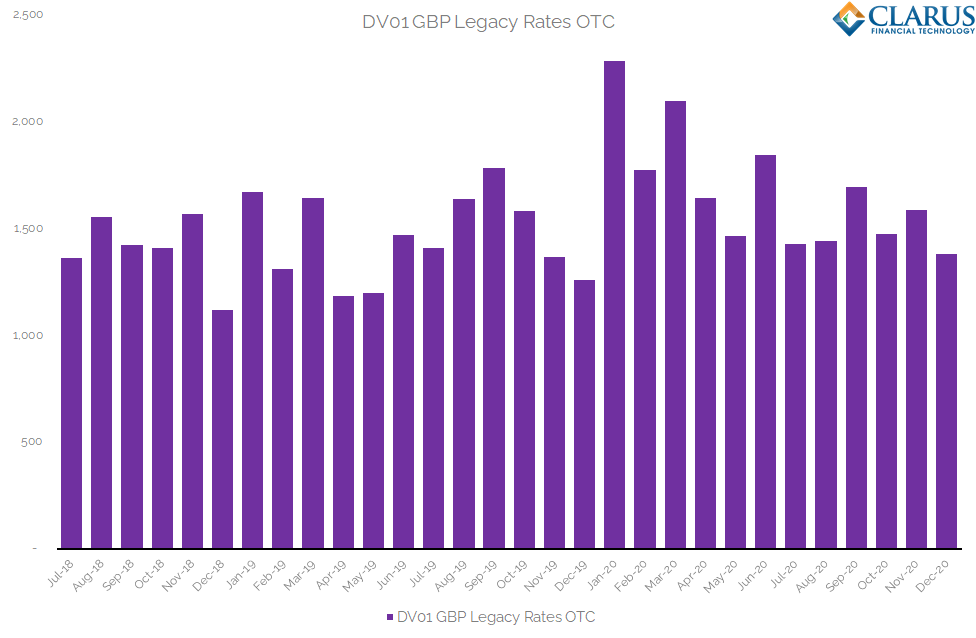

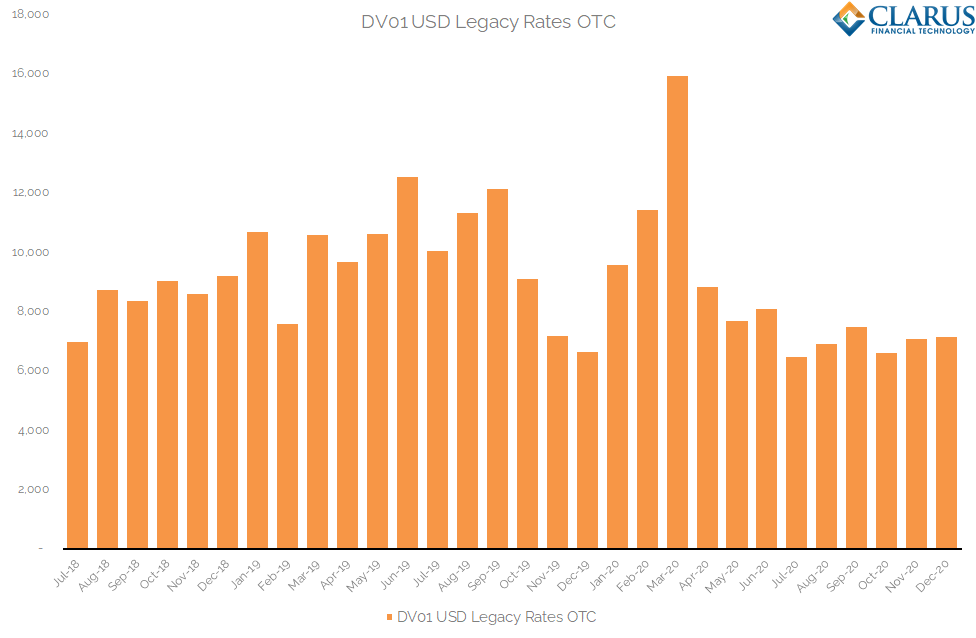

Clarus Data: GBP, JPY and USD LIBOR

Whilst this activity in CHF LIBOR is expected to be relatively concentrated amongst market participants, the other currencies represent far larger markets. The headlines read:

- Q4 2020 DV01 risk in JPY legacy rates: $2.3bn

- Q4 2020 DV01 risk in GBP legacy rates: $4.5bn

- Q4 2020 DV01 risk in USD legacy rates: $7.0bn!

Those are huge amounts of new risk being transacted, and all of the charts show they are not materially different to Q4 2019:

JPY

GBP

USD

These charts suggest that JPY markets have shrunk the most, despite TONA (the JPY RFR) continuing to make up just ~4% of overall JPY volumes (chart 5). This suggests that the JPY derivatives market is simply shrinking. Not good if that means less risks being hedged.

Equally surprising is that there was a relatively large amount of activity in GBP LIBOR markets in Q4 2020, despite IDB markets working to transition to SONIA as the main index. Are these all risk reducing trades? Market participants need to paint a picture in terms of what is happening to their net LIBOR risk!

The USD picture is clearly skewed by a massive spike in activity in Q1 2020, where liquidity was all that mattered. Activity is somewhat down on the year vs Q4 2019, but is it material enough to paint a positive transition story?

Data Driven Conclusions

We are huge proponents of the transition to RFR rates here at Clarus, as evidenced by our prior consultation responses. We believe markets will be simpler, more transparent and easier to trade in an RFR world for all market participants. The transition will be hard, but ultimately rewarding.

However, we think it is important that the data on how much new LIBOR risk continues to be generated is highlighted. Responses to the IBA LIBOR consultation seem to be the most opportune moment to do so. We just ask consultation responses to highlight why this is the case, when transition away from LIBOR is such a regulatory focus.