- If an ‘IBOR rate, e.g. USD LIBOR, ceases to publish, we now know the exact methodology that will be used in derivatives contracts to calculate a replacement rate.

- The calculation uses compounded in-arrears Risk Free Rates, which are decided at a currency level.

- A spread will be added to these compounded rates, which will be calibrated according to realised historic levels of ‘IBOR versus the compounded Risk Free Rate.

- The average of these spreads, calculated across a five year look-back period using a median methodology, will be applied.

- The spread will vary per index tenor – e.g. 1 month USD LIBOR will have a different spread to 3 month USD LIBOR.

Background

We have written at length on the topic of IBOR Fallbacks, starting with LIBOR reform and following the consultations through to the final one from ISDA in September 2019. You can catch up on the blogs below:

https://www.clarusft.com/category/indexfix/

This blog is intended for readers who don’t want to know all of the gory details about how we got here. We just provide a simple overview of what will happen if an ‘IBOR rate ceases to exist.

Final IBOR Cessation Parameters

The spread that will be applied to the Risk Free Rates following an ‘IBOR rate no longer being published will be:

- Averaged using a median methodology.

- Calculated using a look-back period of five years.

- Negative spreads will be included.

- Outliers will be included.

- A two-day backward shift adjustment will be applied for operational and payment purposes.

This spread will be added on to the Risk Free Rate (RFR) for the appropriate currency. The methodology that will be applied to the Risk Free Rate is as follows:

- An overnight, Risk Free Rate per currency is identified.

- These overnight rates will be observed for each interest period, daily compounded and paid at the end of the accrual period.

- The spread above will be added to this compounded interest amount to create the full coupon.

- As per above, this coupon period will be adjusted backwards by two days to allow for payments to occur on time.

Note that on (4), this means that the observation period will now be shifted two days backwards (both start date and end date) for each coupon, preserving the original payment dates of the contract. This is because ISDA stated it was difficult to implement a Delayed Payment as part of its’ changes to the Rate definitions, but it is possible to implement a change to the observation period.

This process applies to all derivatives that are governed by an ISDA agreement. I believe that both counterparties will need to sign up to a protocol of some sort to update their ISDA definitions.

Some industry participants will have to fulfill a fiduciary requirement to calculate these fallback rates themselves. If you are one of those, please contact us and ask for a demo of our IBOR Fallback App:

Which Indices are Covered by these Rules?

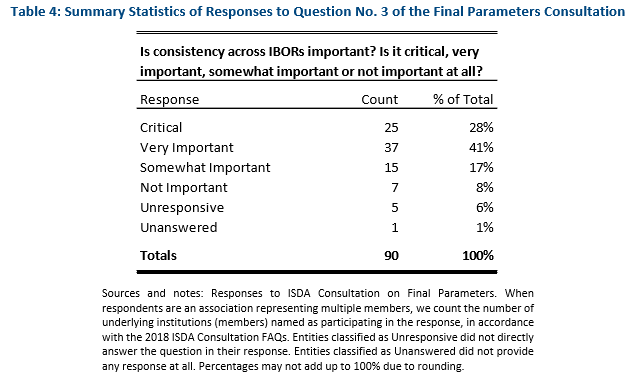

As of this point in time, we can assume that all ‘IBORs that cease to publish will have the same set of rules applied to their fallback rates. Whilst it is still possible that different rates end up with different methodologies, 86% of respondents stated that consistency across different ‘IBORs is preferable:

Particular kudos to the European bank and the American pension fund who stated that this is particularly preferable for Cross Currency Swaps (as did we):

“[w]e view the consistency across IBORs as very important to avoid creating unnecessary dislocations in the basis market thereby allowing these markets to remain a dependable source of information for end users. Consistency is very important to minimize risks of distortion in cross-currency hedging and limit regulatory arbitrage across jurisdictions.”

Page 18, ISDA Consultation Responses

What Did People Say This Time?

For those who have followed the whole story with us (I count eight blogs that explicitly reference ISDA Fallbacks) it is somewhat interesting to dwell on the reasons that a five year look back period and the median was chosen by market participants. The reasons why can be summarised as:

- Shorter period means more reflective of current market conditions. This is a consideration to minimise value transfer.

- Median methodology is stable over time.

- Trimmed mean is too complicated to agree on the methodology.

- Bank funding dynamics may have changed over time, changing the spreads.

- Transparency and simplicity of a median approach was deemed preferable over a (complicated?) trimmed mean.

- SOFR data is better the shorter it is (hence five year period).

What Happens Next?

Right now, we are in a waiting phase for the following to happen:

- We wait for an index cessation to be announced. Let’s assume a 9 month notice period, so this could be as early as March 2021?

- We watch how the LIBOR-OIS basis converges to the (current) five year median levels.

- We wait for Bloomberg to start publishing the data on compounded rates and spreads. From the original announcement, I think this is most likely to happen in Q1 2020.

One point to note: there is no transition period in the final parameters. So the value on the cessation date will be the same value applied to all fixings from that point on. So we can calibrate it pretty accurately from now.

For the calibration, it will be interesting to see if we end up at the five year median as of today, or whether we assume the forwards are realised on the basis curves, and a cessation date of January 2022. That would currently give us a mixture of ~three years actual observations plus two years projections.

The End

From our stand-point, that really is everything you need to know about the ISDA IBOR Fallbacks and what happens if an ‘IBOR now ceases to publish.

I’m glad it’s over. I think Fallback Fatigue has really become a thing. Anyone else feel the same?

Fortunately, the day that LIBOR ceases to publish is very unlikely to be an anti-climatic end to this saga. What a huge industry change that promises to be!