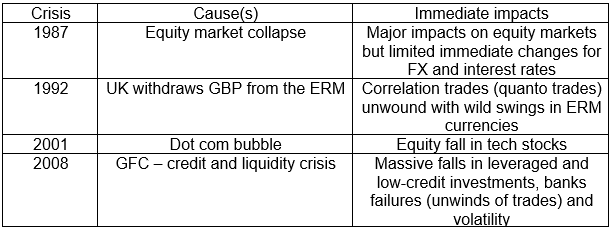

Over the course of my trading career I have had the ‘opportunity’ to be part of the trading process during market crises, both as a junior trader and as a manager of trading teams. My previous experiences were:

- 1987 equity crash;

- 1992 correlation unwinds;

- 2001 tech bubble burst; and

- 2008 global financial crisis

The one common theme is that each started in a different way and played out differently for a trading desk.

In this blog I will look briefly at each crisis as I remember the impacts on the markets and the way trading desks adapted to the circumstances.

The Past

This is not a complete history of meltdowns and market dislocations but rather my recollections of what happened during the crisis and the days that followed. I do emphasise, these are very brief and for those interested in the details I really recommend further reading. Firstly, a short description of each event.

Each had massive impacts over the following days and weeks as traders struggled for liquidity and price discovery with most markets whipsawing on low trading volumes. The consequent reduction in trading risk which participants were prepared to accept further reduced liquidity and increased volatility.

In particular, the GFC event stood out in my mind mainly because so many markets were affected at the same time. The Lehman Brothers collapse forced many of their (former) counterparties to re-hedge the trades that were now non-existent.

FX, interest rate derivatives, credit derivatives, basis swaps had to be unwound which forced traders to buy/sell FX and pay/receive derivatives to reduce the risk they had just acquired. I assumed Lehman were relatively square when they defaulted which should mean balanced buying/selling but the timing of the re-hedging varied across the surviving firms. This led to massive volatility as large parcels hit the markets at different times.

Common threads

Most of the events above were in financial markets which had finally ‘snapped’ after broader economic problems: the run for the (small) door caused a sudden dislocation.

In all cases there was a noticeable run to quality mainly USD, gold and government-issued securities. Everything that could be sold was unloaded to create liquidity for margin calls etc. and then placed in USD.

Chris Barnes noted this effect in a recent blog on cross currency swaps. Also, short-dated FX swaps from overnight and tom/next become massively skewed as markets race to borrow USD which spilled into the longer-dated cross currency markets.

Quality was everything as markets and investors focused on keeping their capital intact rather than returns. The sudden wave of selling caused temporary market dislocations.

But eventually everything returned to ‘normal’.

The COVID-19 Crisis

The current crisis appears to be somewhat different to previous ones. Or is it?

Before the previous crises the underlying economic conditions were generally deteriorating and the financial market crisis marks a point where the traders realized this and made a run for the exit.

On the surface, the recent economic conditions appeared quite favorable in most countries and global trade was strong notwithstanding a few tensions (e.g. USA and China, Brexit).

Then it all stopped as the pandemic was announced and governments took drastic action to attempt to contain the rate of spread. Businesses are shuttered, trade has slowed, international travel is largely banned and large gatherings of people are no longer possible.

And now there is serious talk of an extended period of economic downturn from which some businesses (e.g. airlines) may not recover.

Perhaps the underlying conditions may have been more fragile than we thought; only time will reveal if this was true.

However, the market impacts are very similar to all that preceded COVID-19.

Already the CME has seen the default of Ronin Capital a direct futures clearing member and auctioned it’s positions on Friday.

What is happening in markets?

Equity markets are taking a very solid beating in most countries except China. This is expected as traders unwind positions and look forward to tougher economic conditions.

The FX markets saw USD rally against most currencies as cash (from equity and investment sales) in other currencies was sold and the USD purchased. Initially USD government securities saw price rises but these slowed and then fell again.

But, as is customary in these circumstances, we did see a rapid spike in USD cash rates over the past week. For example, overnight USD cash in the UK time zone has spiked to 5 – 7% (with US target at 0 – 0.25%) yielding super profits or losses for traders – it depended on how you were positioned.

I do note that SOFR and EFFR were actually quite well behaved with SOFR trading (99 percentile) as high as 2% on 16th March. So, it appears the US market had sufficient liquidity and the only real squeeze in USD cash occurred before US open.

Emergency target rate easing by central banks have seen short-term interest rates rally substantially. The rallies in futures and OTC markets have been relatively steady as traders become increasingly convinced of central bank intentions.

Credit spreads have pushed out (as usual) led by the LIBORs and IBORs against the cash rate (OIS) markets. For example, the USD LIBOR/OIS spread was around 10 – 15 basis points in February but is now closer to 50 – 50 basis points (3 months). This is typical of the credit/liquidity spread: it increases in times of financial stress.

Longer-term rates have generally fallen but have seen substantial volatility as traders sold non-USD currencies (e.g. AUD government bonds) and bought USD thereby causing occasional rapid rises in yields before the trend to lower rates exerted its authority.

And on top of everything, we have seen a massive fall in the oil price totally unrelated to COVID-19.

One of the more unusual aspects of this event is the lockdowns in many countries. In the past, traders have been at their desks and markets have been open if somewhat dis-functional.

But this time is very different: traders are at home working remotely with limited access to each other. Markets remain open (for now) and appear to be coping well with the volatility and the changed circumstances of many participants.

Summary

One thing I have learned over several crisis event is that they are never quite the same. Each one has its own idiosyncratic way of playing out and finally dissipating.

They start for different reasons but follow the same path of a disorderly unwind of leverage.

But they do end.

USD has always been the ‘go to’ and gold remains a perceived safe haven. The old adage ‘Up by the stairs and down by the elevator’ may be true.

But every time I have been in a crisis event it has felt more like ‘Up by the stairs and down by the elevator shaft’.

But it always ends and this time will be no different.