With Cross Currency Swap blogs continuing to perform well on the Clarus Blog each year, let’s take a look at what traded during 2022.

SDRView Volumes

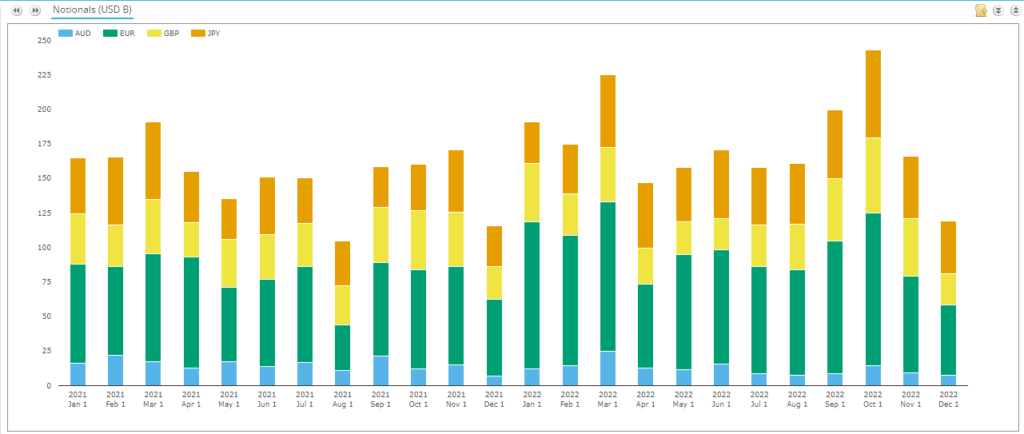

SDRView shows the monthly volumes transacted of Cross Currency Basis swaps. These are, on the whole, the vanilla interbank type of mark-to-market cross currency swaps.

Showing;

- Monthly volumes in XCCY Basis swaps for the past two years. Please check our previous Cross Currency blog to see the big stories for 2021!

- Seasonality was alive and well in Cross Currency markets in 2022.

- The traditional “issuance seasons” – January, around Easter and September/October saw the largest volumes in 2022.

- Large cross-border issuance is likely the main driver of demand.

- Q1 in 2022 was the largest volume period, with event risk driving repositioning of risk.

- Comparing the two years, volumes were about 15% higher in USD equivalents last year than in 2021.

- EURUSD saw the largest increase in volumes, at about 30% growth, whilst AUD volumes decreased by about 20%.

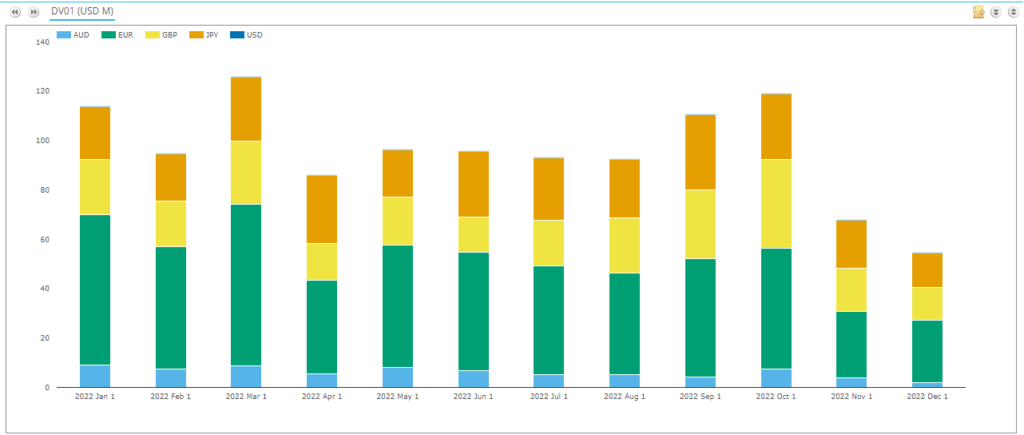

SDRView also shows the DV01 of cross currency swaps traded:

The overall pattern of volumes is somewhat similar between the two charts in 2022. January really is a big risk month for XCCY basis, and March was a real peak for risk – it wasn’t only short-end repositioning. The drop-off in December was even more marked on a DV01 basis as well.

Combining the two charts with the number of trades transacted each month gives us some idea as to “standard” trades in XCCY swap markets in 2022.

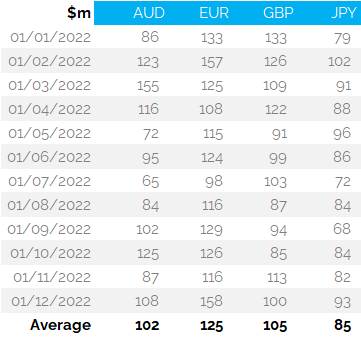

First up, average trade sizes in $Millions equivalent for each currency pair:

Showing that the average trade sizes for the year ranged from $85m in JPYUSD to $125m in EURUSD. The averages did vary a lot month-on-month however -for example, despite low volumes, average trade size was $158m in EURUSD in December.

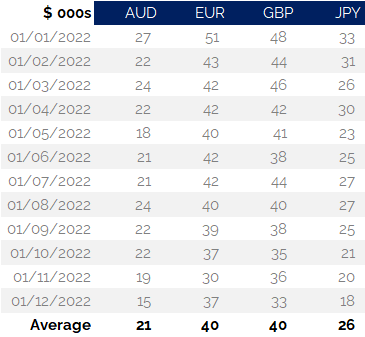

And next average DV01 traded in thousands of $ for each currency:

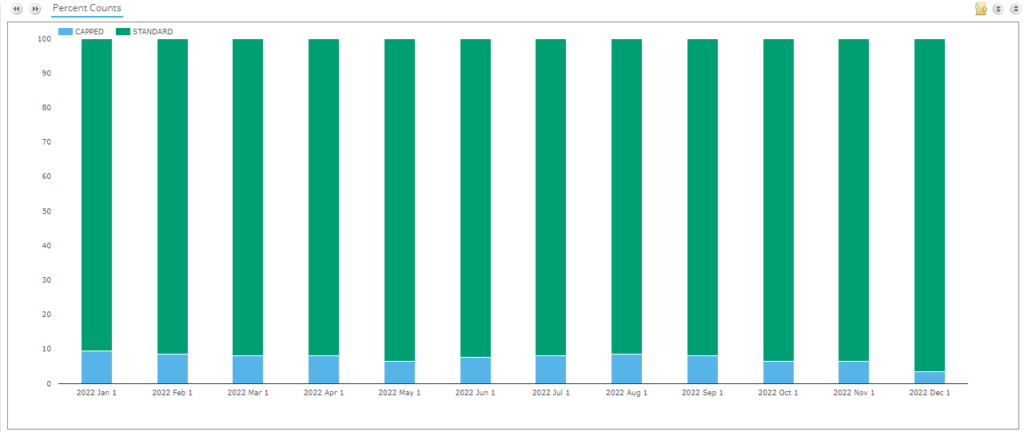

Now, each of these tables are subject to the block reporting thresholds – so they are certainly understated, representing more of a “median” average than the “mean”. Anything from 3% to 10% of XCCY trades were reported above the block threshold each month:

Assuming block trades are evenly spread across all maturities (is that fair?), we can state that:

- In EURUSD, average trade size is larger than $125m, representing at least $40K DV01 of risk. This implies an average maturity of about 3.4 years (i.e. $125m of 3.4Y is equivalent to $40K of DV01 risk).

- In GBPUSD, notional sizes are smaller at $105m equivalent, but still equal to an average of $40K DV01. This implies a longer average maturity of 4.1 years.

- JPYUSD is a smaller market. Average notional size is just $85m and $26K DV01, implying average maturity of 3.1 years.

- Finally, AUDUSD figures suggest a surprisingly chunky average trade size. At $102m it is in line with GBPUSD, but the average DV01 is much lower at just $21K. This creates an average maturity of just 2.2 years – which seems low? I know the long-end of AUDUSD over about 15Y really struggles for liquidity, but I am surprised the average come out so short.

These averages can also be further refined by splitting the data between block trades and “normal” trades – let us know if you are interested in this type of analysis. I should also highlight that block thresholds will be changing in Q1 2023 – see my old blog for more on this:

SEF Trading

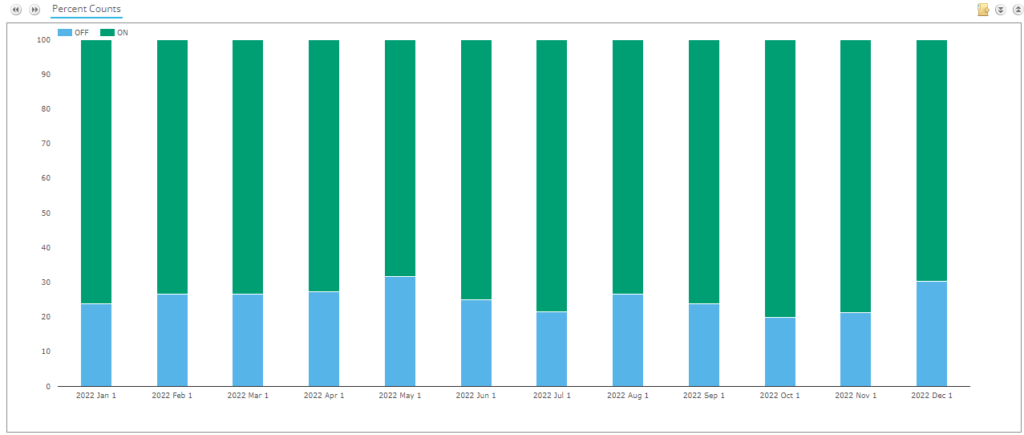

In terms of SEF Trading in vanilla XCCY basis, the proportion of SEF trading by trade count has been pretty stable in each month of 2022. Only 24-32% of trades were reported as off-SEF:

As a reminder, this doesn’t cover the whole global market – so it is difficult to say whether SEF trading in XCCY has seen a particular benefit from e.g. Brexit. We would need European (or UK!) transparency data to make a definitive judgement call.

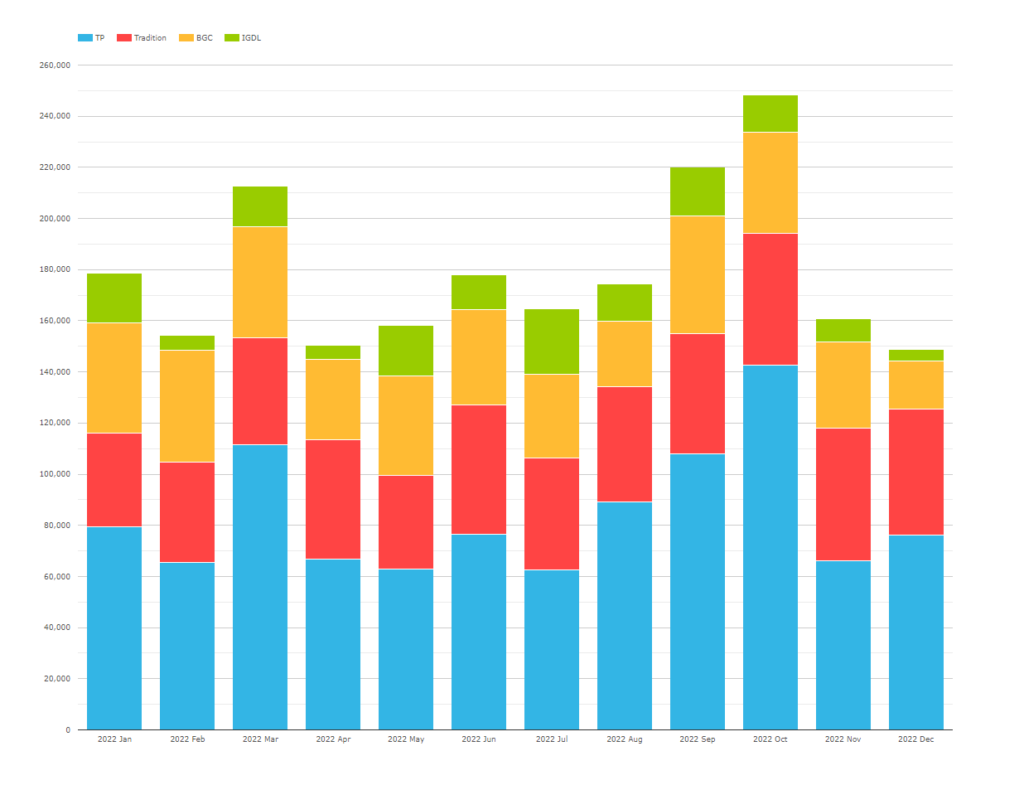

Over on SEFView, we have the overall 2022 market share stats for Cross Currency Swaps per SEF:

Showing;

- Only 4 SEFs reported volumes in Cross Currency Basis in our four currency pairs last year.

- In notional terms, Tulletts reported the largest market share, at 47%.

- Tradition were second at 25% for the year.

- BGC in at third with 20%.

Two things to note with this data:

- The Tulletts and ICAP XCCY desks must be sending all of their SEF trades to a single venue.

- This data isn’t necessarily representative of the whole market, only the portion traded on-SEF.

For the portion of the market that IS traded on-SEF, we now have trade-level transparency as to where a swap has traded. As per Amir’s blog below, which looked at USD Swaps:

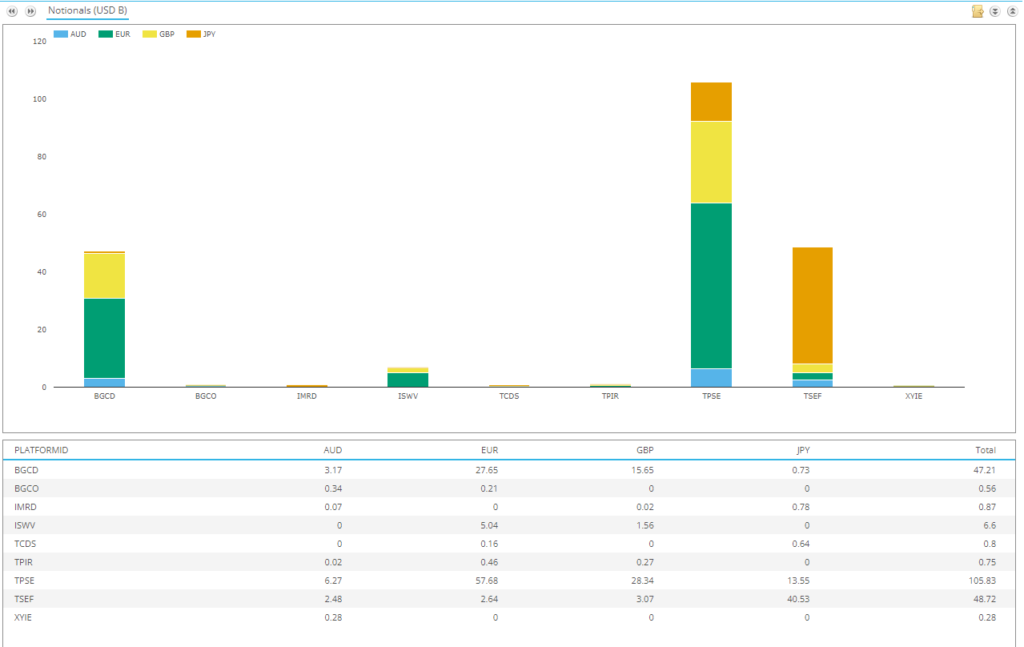

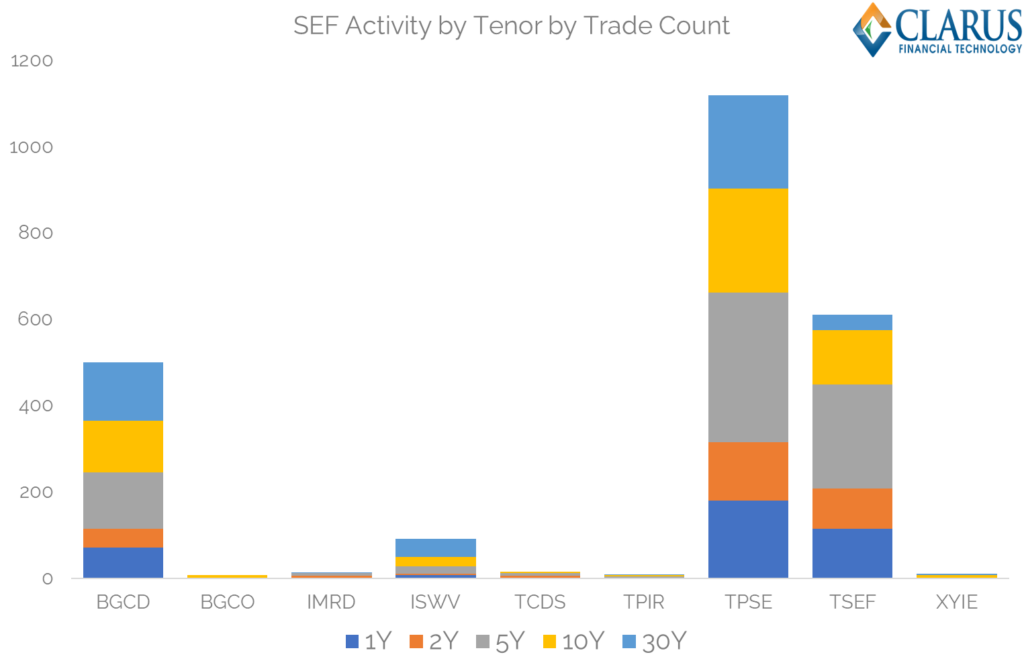

Since December 5th, we can see which platforms Cross Currency Swaps have traded across:

Showing;

- Notional volumes for XCCY Basis reported as “ON SEF” per platform since December 5th.

- The platforms are identified by so-called “MIC” codes. In plain English, we have:

- TPSE, IMRD, TPIR = Tulletts SEF, TP ICAP UK MTF and TP ICAP Europe MTF.

- TSEF and TCDS = Trads SEF and Trads OTF.

- ISWV = ICAP Voice

- BGCD and BGCO = BGC

- XYIE = Yieldbroker (an Australian broker)

This allows us to monitor trades in real-time as they come in on each SEF via SDRView Professional, a significant change to how we have been able to use the data previously. It also allows us to monitor market share by:

- Trade count

- Notional

- DV01

- Block trades

- Tenor

For example:

Pretty interesting data for anyone involved in the markets and nice to see improvements to transparency data in the US.

In Summary

- Cross Currency swap volumes increased by 15% in 2022.

- EURUSD volumes in particular increased by 30%.

- Average trade sizes range from $25K to $40K DV01, depending on the currency pair.

- About one-quarter of XCCY trades are reported Off-SEF in the US data.

- We now have trade-level transparency for the 75% of trades on-SEF thanks to improvements in the public data.

- We will also see changes to the block thresholds in Q1 2023.