Back in July of 2016, the CME submitted a proposal to the CFTC for a new class of clearing membership which they call “Direct Funding Participant” (“DFP”). I was drawn to the topic last week when Bloomberg wrote an article about its imminent effective date of Sep 23, 2016. As it happens, it appears that date was just a requested date, as I cannot find any mention of it on the CME website. Perhaps this might require a more formal blessing from the CFTC.

I took the time to educate myself on how the Direct Funding Participant (DFP) model might work, so I thought I would share what I learned in my “Direct Clearing For Dummies” education. Here is the overview:

- Instead of being a client of an FCM, a client can clear directly as a “DFP” with the CME. A “DFP” must, however, be sponsored by an FCM.

- The DFP would pay VM, IM, and option premiums directly to the CME (not through an FCM)

- The DFP could only clear their own trades (they cannot have clients)

- The DFP would have same settlement cycles as any other member (twice daily for futures, once for swaps)

- Initial Margin requirements slightly higher by 4%

- The DFP would NOT contribute to the guarantee fund. Instead, their Guarantor (an FCM) would accept their risk of default including:

- Their Guarantor (FCM) pays their share of GF contributions

- Their Guarantor (FCM) would be responsible for the DFP’s (client’s) waterfall contributions (assessments, loss mitigation, etc)

- If the DFP Guarantor (the FCM) fails, the DFP (the client) would be liquidated unless they have another DFP Guarantor (or FCM) immediately available

The rosy glass-half-full perspective on this is:

- Client avoids Fellow Customer Risk (No pro-rata loss allocation if another FCM customer defaults and causes FCM to go bust)

- Because DFP’s margins bypass the FCM, the FCM (“Guarantor”) would not have cash collateral on their balance sheet, so it would not count towards their leverage ratio

To sum that up, by being a DFP, the client is doing the FCM a favor by not giving them their cash! Is that where banking has gotten to?

Forgetting costs for a second, the only downside for the client would seem to be that the DFP (the client) needs to make margin calls earlier than they might have with their FCM – there is no grace period when dealing with a clearinghouse.

HISTORY LESSON

I wanted to go back to your fathers FCM days. The way the FCM made money was basically twofold:

- FCM charges clearing fees to the client

- FCM gets to play with a bunch of excess client funds

The first one is obvious. Every FCM has a schedule of fees. Trade clearing fees, trade maintenance fees, capital allocation fees, guarantee fund contribution fees, “you’re a risky client” fee, etc. They might be called various things, and might even be dropped if you are a good enough client, but there are fees that can be tied back to trading activity and/or how much risk is introduced to the FCM.

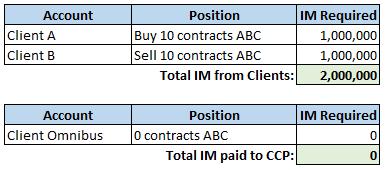

The second one is more intricate. Let us take a simple example of an FCM that has two clients, Client A & Client B. In this example, each client has an equal and opposite position. Under some old-school margin and segregation models, each client has to pay the FCM some amount of initial margin based on their leveraged positions ($1mm each in my case). The FCM collects this $2mm. But, because the account is really just a big pile with all client’s positions in it, the CCP only calls the FCM for enough margin to cover the net risk, which is 0 (10 long and 10 short). This diagram attempts to explain this:

So in our example, FCM collects +$2mm from clients, and pays nothing to the CCP. The trick of course is to take that $2mm and put it to work overnight for a yield. The FCM might have to pay the client some interest, but the game was to beat the rate you were paying a client. It was, basically free money.

On top of this, many clients left excess funds at their FCM. So while they might have only been required to have $1 mm at their FCM, they might keep $100 mm. Even more money to play with!

However, over the past many years, three things have changed:

- Interest rates have gone to 0, thereby reducing the amount of yield the FCM can make on excess customer funds

- More elaborate accounts have been created and prescribed that limit the FCM’s use (and access!) to client funds

- Clients have become more sophisticated, and are leaving litte to no excess funds at their FCM

Let’s next examine these various account types next.

CUSTOMER FUND PROTECTION

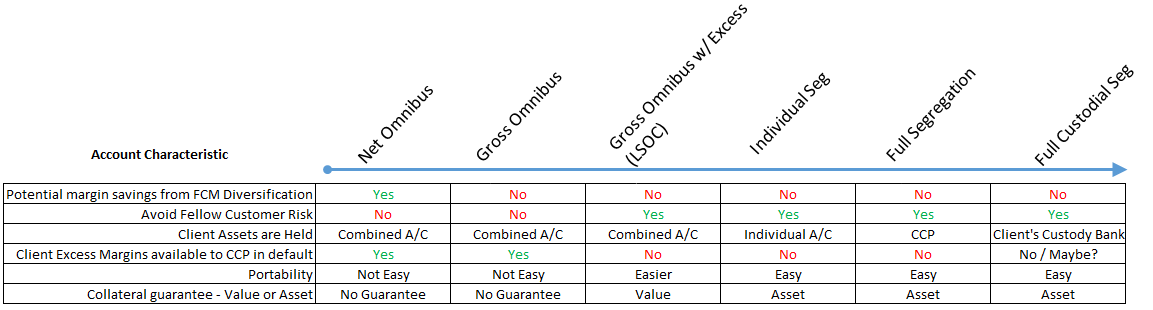

With the advent of Dodd-Frank and EMIR derivatives rules, there now seems to be many account types for cleared derivatives. I have attempted to construct a spectrum of these account types below:

My example account where the FCM had 2 clients and enjoyed a free $2mm to play with was the Net Omnibus structure. Margins were diversified, client funds were commingled, and clients stood the risk of another client blowing everything up.

I should note that even this “Net Omnibus” model is no longer in play in the USA. Generally speaking, the US currently has 2 flavors: Gross Omnibus for futures, and LSOC for swaps. The only possible funds the FCM can “play” with would be excess funds pledged by the client that is above and beyond their margin requirements. And even here, there are limitations on what the FCM can do with those funds, as defined by CFTC rule 1.25 which limits their activity to very secure securities.

On the far side of the spectrum, there is actually a class of account type now – I’ve called Full Custodial Seg – where the client’s funds don’t touch the FCM, and in fact they don’t even touch the custodial bank of the Clearing House! This appears to only be planned by LCH in Europe.

But as you move from left to right in this spectrum:

- Clients margin requirements need to be fully pledged

- The FCM loses access to the client funds, and even the excess client funds

- Porting of a client account becomes easier (because all of the cash/collateral is more readily identifiable)

- The value of, and actual pieces of client funds become more secure

Of course, the client should expect to pay more for their clearing services as they go further right along this spectrum.

It would seem the CME’s model of DFP lies somewhere around the “Full Seg” portion of the spectrum, in that the client (the DFP) deals directly with the CCP for settlement and has no exposure to the FCM. In fact, DFP seems awfully similar to Eurex’s ISA Direct Program, which would seem to fall under my Full Seg category.

ECONOMICS

So the pressing question is – what’s in it for the FCM?

I’m guessing here, but it would seem that in a direct clearing relationship, both revenue models are gone:

- There are no trades to produce fees on (though the FCM / “DFP Guarantor” is told about the trades)

- There is no excess cash to play with

So basically, the only service the FCM (the DFP Guarantor) is providing, is an insurance policy.

The pricing model of this service would theoretically have to change so that it encompasses only:

- FCM cost to finance the proportional Guarantee Fund contribution

- FCM insurance policy to cover:

- The losses arising from the possible default of the DFP

- The losses arising from any possible members default (assessments, loss sharing)

- Some cost to cover the possibility that the DFP operations team are out golfing, miss a payment, and the FCM has to scramble for a few hundred million in a moments notice

It boils down to a pure-play extension of credit by the FCM (The Guarantor) to the client. They wouldn’t even have to touch a trade!

It’s not clear to me which clients and which FCMs would want this kind of structure, and how much it would cost.

SUMMARY

- CME has filed a request for a new “DFP” account type

- DFP caters for direct clearing by a client to CCP

- An FCM “DFP Guarantor” has to guarantee the performance of this client

- The model seems to accomplish “Full Seg” that is available in Europe

In the grand scheme of things, it’s a logical proposition. It’s really no different to what has happened to many things in the retail space. Consider something as benign as the mobile phone market. Do the mobile phone carriers make money on your wireless service? Maybe. But their easy money came from financing your phone for 3 years. People are getting smarter and bringing their own phone and asking the mobile carriers to provide a single service – data. In some form, that is what’s being proposed here in the clearing space – some clients may just ask for a single service – insurance.

It will be interesting to see if there is any appetite for this in America, and how this unfolds.

Very informative and helpful Tod