- We estimate the Initial Margin impact from moving EUR Clearing out of the UK

- This could happen as a result of Brexit

- We can make an estimate as to the maximum margin impact possible using publicly available data

- In terms of Initial Margin, we only see a small impact on the LCH SwapClear portfolio in London

- But the data leads us to estimate a doubling in IM from $83bn to $160 billion for the industry.

- This is driven by a new clearing venue located in the Eurozone.

Bloomberg Reporting

There has been a lot of coverage in the press recently, particularly by Bloomberg, on what could happen if EUR clearing were to be forced out of the UK upon Brexit. There are several stories, including:

Banks Said to Plan for Loss of Euro Clearing After Brexit

LSE’s Rolet Says 100,000 Jobs at Risk If Clearing Leaves London

Bank of America Official Likens Brexit to Nuclear Waste Move

But let’s approach this from a data angle. Can we estimate the effect on the market from bifurcating Interest Rate Derivative portfolios in a way that leaves non-EUR business in London and EUR-denominated business elsewhere?

Using public data we outline a methodology that can be used. It is important to understand the caveats that go hand-in-hand with this methodology:

- We do not have detailed position data

- We do not know the concentration of risks across counterparties

Nonetheless, we present an estimate that we feel is credible given the data available. Feel free to reach out to us or comment below with any thoughts.

Total Margin

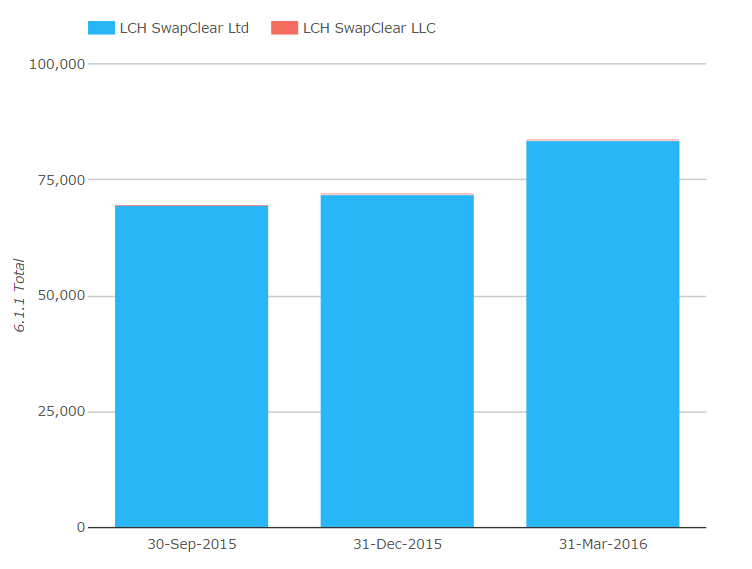

As Amir has noted in his blogs about the disclosures, CCPView now includes details about how much Initial Margin is held by CCPs. For LCH, we can see that this has been steadily increasing since September 2015:

Showing;

- As at 31st March 2016, Initial Margin at LCH SwapClear (which is in the UK) stood at $83.34bn

- Of this, $32.1bn is Client and $50bn is House.

Outstanding Notional

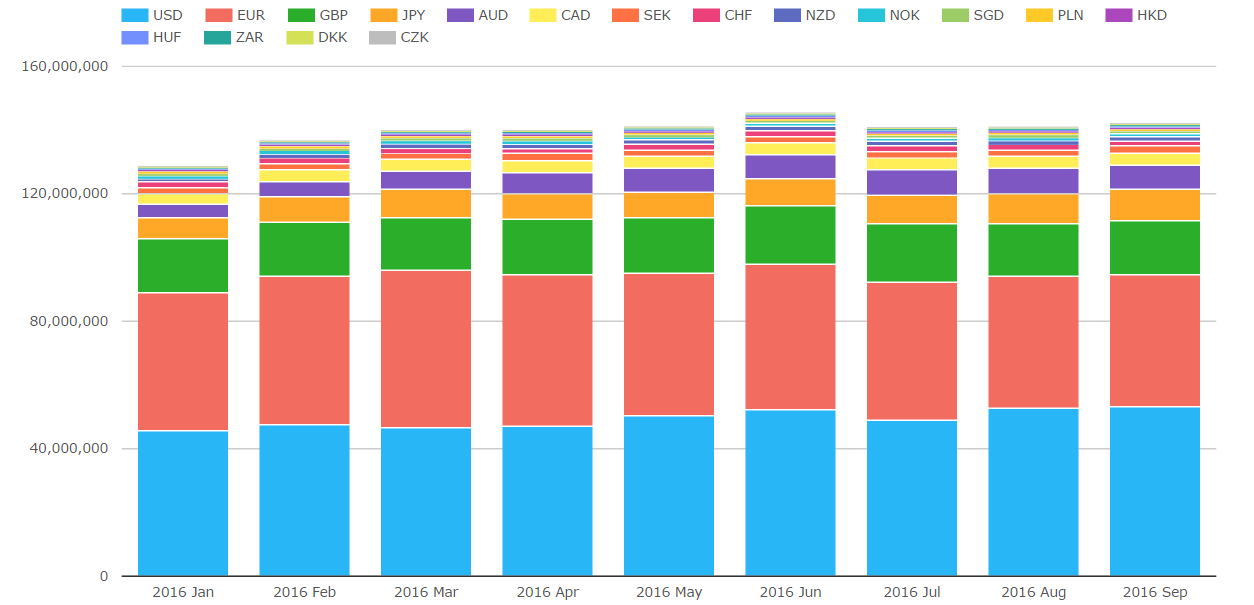

To work out the impact on Initial Margin from moving the EUR business out of the current London location, we need to have an estimate of how much of the outstanding notional at LCH is currently denominated in EUR. This is super simple using CCPView:

Showing;

- Notional outstanding, aside from a jump in February this year, has been pretty much constant all year – that’s all the hard work from compression paying off!

- USD is currently the largest currency by notional outstanding

- EUR is second

- EUR and USD have been fighting for number one spot all year

- In percentage terms, in March 2016:

- USD made up 33.3% of outstanding notional

- EUR was 35.4%

- GBP was third at 11.7% and JPY fourth at 6.27%

- In absolute terms, as at March 2016:

- USD had $46.6 trillion outstanding

- EUR had $49.5 trillion outstanding

- GBP $16.4tn and JPY $8.8tn

Volume Weighted Average Maturity

To estimate the impact on the industry, as well as knowing the size of positions, we also need an idea of the average maturity that the outstanding notional applies to. Let’s also assume that it is mainly Outright risk that is the driver of IM, therefore this is the trade type we are most interested in.

From SDRView Res, we can therefore use our Tenor view to estimate the Volume Weighted Average Maturity for the LCH SwapClear portfolio. Across USD, EUR, GBP and JPY , which make up 86% + of notional outstanding, we see the following tenors traded:

Showing;

- Most activity (as measured by DV01) is in the benchmark tenors of 2y, 5y, 10y and 30y.

- Let us assume that the amount of notional outstanding mirrors the volume activity.

- Therefore, we calculate the Volume Weighted Average Maturity as:

- USD 11.9 years

- EUR 13.0 years

- GBP 12.9 years

- JPY 10.3 years

- We can be pretty confident that because these average maturities are very similar, that there isn’t too much difference between currencies.

- Therefore, let’s take the overall average maturity across the LCH SwapClear portfolio as 11.9 years, which is the average across all four currencies. For ease, I’ll be rounding that up to 12 years to make deal input quicker.

Estimating the Impact on IM

Given these two facts, can we simply model the LCH portfolio as $46.6tn of 12 year USD IRS vs $49.5tn of 12 year EUR IRS? Sadly not. The notional outstanding does not give us an idea of what positions are driving IM for example, and notional outstanding is not the equivalent of Open Interest in Futures.

Instead, we need to guesstimate a representative portfolio of Interest Rate risks that will generate an IM of $83bn. To do this, we will split the risk according to the ratio of notionals outstanding in each currency. We therefore turn to CHARM and some IM modelling.

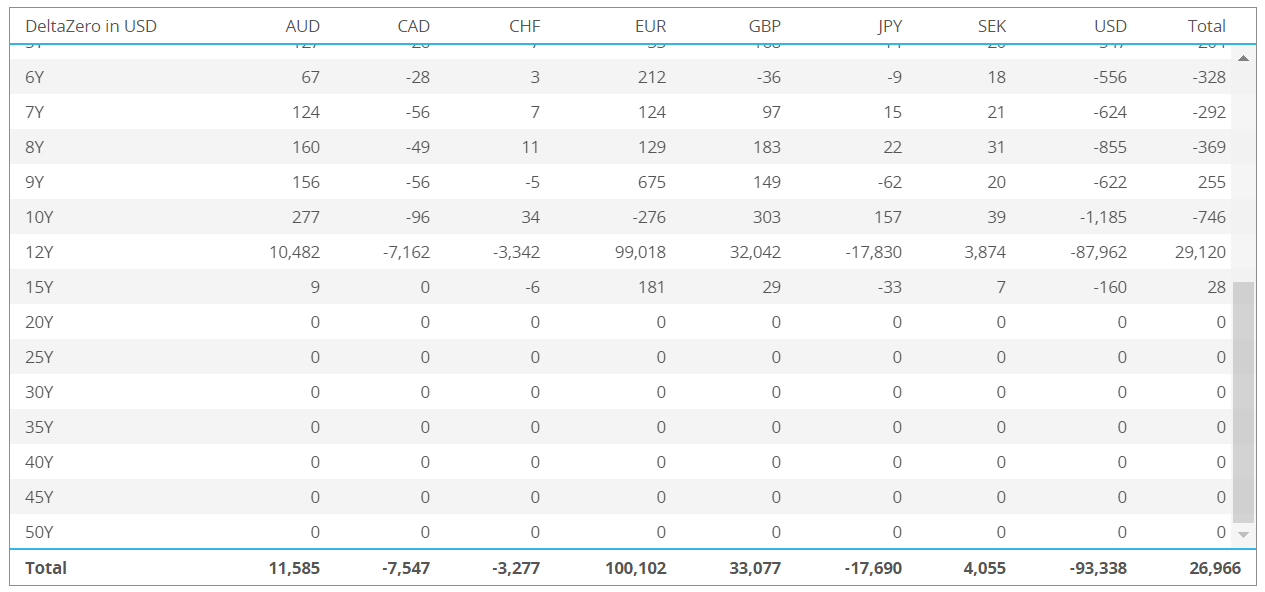

First, let’s see what a portfolio of 12 year swaps looks like with the currency split according to that of the notional outstanding:

Showing;

- DV01, in USD equivalents for each currency in our model portfolio.

- This model portfolio shows risk per $100k of DV01 in 12 year EUR swaps.

- We simply apportion the risk in non-EUR currencies according to the ratio of notional outstanding in EUR swaps.

- We have no way to know whether the portfolio should be “paid” or “received” in any currency, so we will simply alternate between currencies.

- We only model the top 8 currencies. This represents over 96% of the total notional outstanding.

- The overall portfolio is not delta neutral – there is an overall position of $27k in DV01.

- The goal is to see how much Initial Margin this model portfolio consumes. We will then scale up to estimate a risk profile for the whole market that creates $83bn in IM.

Before we show the IM figure for this portfolio, it is worth running over the following thought experiment:

- A CCP is always risk neutral – there is a buyer for every seller and vice versa.

- CCP margin for Interest Rate Swaps is not symmetrical – payers see a different IM amount to receivers.

- Therefore, for this model portfolio we need to model both sides. We will therefore have sixteen 12 year swaps, two in each currency with offsetting risk. This keeps the CCP risk-neutral.

Initial Margin Numbers

- Excluding any add-ons for liquidity risk, this portfolio, assuming it is all house business, has an IM requirement of $3.15m

- “Doubling up” the portfolio to represent both sides of each trade, we see:

- Side 1 IM of $3.15m as above

- Side 2 IM of $3.76m

- Total IM at LCH of $6.90m

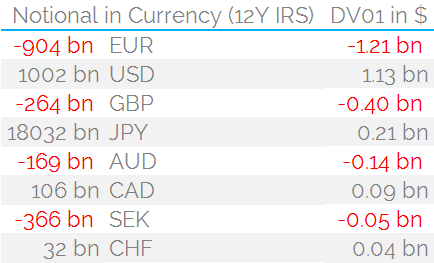

To model the whole market, we therefore have to scale this portfolio up by 83.34 bn divided by 6.9 m – i.e. we need to look at a position over 12 thousand times bigger. This results in positions of almost one trillion dollars in 12 year EUR and USD swaps! The exact positions are shown in the table.

To model the whole market, we therefore have to scale this portfolio up by 83.34 bn divided by 6.9 m – i.e. we need to look at a position over 12 thousand times bigger. This results in positions of almost one trillion dollars in 12 year EUR and USD swaps! The exact positions are shown in the table.

The Initial Margin results are linear – because we are calculating without add-ons. Therefore, we see:

- Side 1 IM of $37.97bn

- Side 2 IM of $45.37bn

Which as expected adds up to a total of $83.34bn.

Is this believable/possible? It’s important to understand the caveats!

The above analysis suggests that if Euro clearing were to leave LCH in London, then the net effect would be to move over €1 trillion of 12 year swaps to a new clearing location (in the Eurozone). In risk terms, that is moving over $1.2 billion in DV01.

Recall that as at the end of March 2016, when the IM numbers were calculated, the total Open Interest for EUR swaps was nearly $50 trillion. We are therefore saying that the overall outright position is around 2% of the outstanding notional. This doesn’t actually sound too far-fetched.

However, we should note that this number assumes there are only two accounts at LCH – Side 1 and Side 2. In reality, LCH obviously have a multilateral network of counterparties, which grosses up IM – as we have discussed numerous times in blogs such as this, this and this.

When calculating IM, we have also ignored add-ons (as we like to work with linear problems) and assumes everything is house business, therefore ignoring Client add-on factors.

Due to these caveats, using the public data available to us will likely end up with a figure closer to the maximum possible impact rather than the actual impact.

This is due to grossing up over hundreds of accounts. We are modelling only two accounts to arrive at an IM figure of $83bn. In reality, there will be far more accounts (probably hundreds), meaning that the amount of risk required to create $83bn of IM is much smaller.

The IM Impact to the London Clearing House

With these caveats clearly stated, let’s go ahead and run the numbers.

Moving EUR clearing out of LCH SwapClear, using our methodology, will involve removing €1trn of 12 year EUR swaps from our model portfolios. This results in the following IM changes:

- Side 1 goes from IM of $37.97bn to $36.28bn

- Side 2 goes from IM of $45.37bn to $47.52bn

- Overall, an increase in IM of $462m

Half a billion dollars? Across the whole industry? As a maximum? That doesn’t sound much….we bet you were expecting a much higher number, right?

Take a quick look at the scenarios below (click to enlarge):

This scenario analysis shows that when we remove the EUR risk from the portfolio, the driving scenarios of IM change. This is because the IM of the portfolio is now driven by a large outright USD position in 12 year swaps, instead of a EUR vs USD 12 year spread when the EUR risk was present.

IM Impact at a Eurozone Clearing House

The impact at the London Clearing House looks fairly manageable. However, the EUR trades still have to go somewhere!

Both sides of every EUR position will now have to post IM at a clearing house outside of the UK. Clearing this EUR position on a standalone basis will result in an additional IM requirement. Because we are moving €1 trillion of 12 years in a directional position, this is a very risky thing to do and hence results in a very large IM requirement:

- Side 1 IM of $39.45bn

- Side 2 IM of $37.58bn

As we see in the following scenarios, this IM is driven entirely by the EUR 12 year positions, as expected:

Overall, bifurcating the existing LCH portfolio into EUR risk and non-EUR risk leads to an increase in IM requirements of $77.5bn.

To reiterate, this is to clear exactly the same risk. The bifurcation would nearly double the amount of IM that is currently being posted.

Hopefully, this would not be the day one impact – this is the result of moving the entire portfolio, which would take a considerable amount of time. For something so unprecedented, we do not know how that would work – whether only new EUR trades would have to be cleared in the Eurozone, or whether regional CCP transfer trades would have to be enacted.

There may also be impacts on Variation Margin and Compression (from separating old and new trades), plus overall increases in Default Fund contributions (mainly at the new CCP).

In Summary

- We combine public sources of data to estimate an IM impact from moving the clearing of EUR denominated OTC Interest Rate Derivatives out of the UK and into the Eurozone.

- As with any exercise such as this, it is just as important to understand the caveats and methodology involved as it is to look at the headline number.

- When we model the LCH SwapClear portfolio as only two counterparties, we estimate that IM would nearly double – from $83bn to $161bn. This is an increase of $77.5bn.

- This arises from moving a €1trn 12 year position from the UK into a new Eurozone Clearing House.

- This increase in IM is almost entirely driven by the directional position of the EUR trades at the new Eurozone Clearing House. This highlights the inter-connected nature of both the risks and the clearing business.

Brilliant – worth every penny.

Not sure I follow the estimation or basis fully. As usual with scenarios like this market behavior is impossible to model and we can only model crude scenarios based on outcomes of EU regulation.

Firstly, I assume EU cannot ban cross-currency clearing outside eurozone/EU. Would mean EUR-USD trades could only clear inside eurozone which is truly nonsense.

Secondly, I assume EU would try to ban all EUR single currency CCP clearing outside eurozeon and european free trade area (includes Switzerland and a couple of scandi-countries I think?). This would mean not just UK but US, Japan and others were affected.

Thirdly, since Brexit is the pressing issue it may be that EU tackles UK first (leaving US and others to a later date – potentially given them an interim advantage over UK?

If true this makes CME US and LCH US and ICH US temporary homes for Brexit CCP fugitive clearing.

I seem to remember massive currency offsets between EUR and USD and JPY are central to the LCH strategic advantage (more balanced between EUR and USD and JPY) where CME is dominated by USD and Japan clearing is almost all JPY. Is that still the case?

If so then pulling out EUR from the portfolio and clearing it in the eurozone either in a new CCP or Eurex or a new LCH eurozone entity) is a massive risk and margin gross up which rationalizes your figures. However, if the third assumption is true then the natural thing for the banks is to migrate both EUR and USD IRS to US CCPs (LCH US which is almost empty last time I looked, CME US) and for the US and UK clients at least to migrate with them.

Since spread trades exist these could easily enough be used to flatten out LCH London portfolios per currency vs one of those CCPs to move say the USD, EUR, GBP, JPY delta across Not sure where CCP compression has got to in sophistication but compression trades could do the rest of the work to tear up the flat risk USD and EUR portfolios.

Since this is not the intended outcome of EU regulators, they may try to implement the global non-eurozone EUR clearing ban all at once which would take much longer to land i.e. landing regulatory agreement with UK , US and Japan regulators more or less at the same time.

This would take much longer and is more fraught as US regulators for sure and Japan maybe would look for reciprocity. e.g. this would mean pulling USD and JPY clearing from EU CCPs. Now we’d have a huge global gross up and IM cal to no-ones real benefit.

At this point EU regs might realize that the idea of banning EUR clearing outside EU was not well founded. (After all currencies are really borderless. USD certainly is. EUR ought to want to be if it is to compete with USD as a global benchmark currency).