Last week Eurex put out a press release, DekaBank successfully switches swaps book to Eurex Clearing which was interesting enough to make me want to find out what else I could learn about the switch.

The public details are that over 7,000 individual transactions were switched from LCH SwapClear to Eurex Clearing in a single day, Thursday November 7th. That is all the information provided.

The first question that interest’s me is how much notional or risk was switched?

Volumes

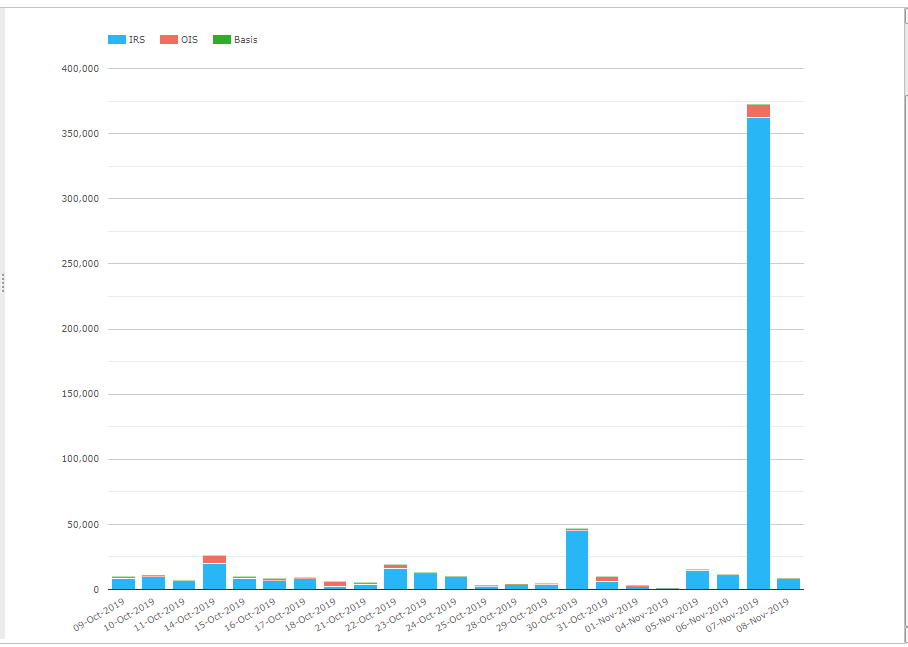

CCPView has daily volumes and open interest from all Clearing Houses that clear OTC derivatives, so lets look at the Eurex daily volumes for the last month, selecting only the currency EUR and Swap product types.

Showing a massive spike on 7-Nov-19 with €362 billion of IRS and €10 billion of OIS and €200 million of Basis Swaps gross notional cleared. This volume is far higher then any day in the past month or year, with previous highs for EUR IRS at Eurex being 30-Oct with €45 billion and 6-Mar with €32 billion.

While we cannot say that all of the €362 billion of IRS is from the 7,000 swaps transferred by Dekabank, the vast majority must be. If we work out the average daily value (ADV) for the period 9-Oct to 6-Nov inclusive, we come up with €9.6 billion, lets call it €10 billion and taking this out of the volume on 7-Nov, leaves us with €352 billion to attribute to the transfer.

Dividing €352 billion by the 7,000 transactions, gives us €50 million per transaction, which is the standard market size for a 10Y IRS trade, so am pretty confident we have an accurate estimate of the gross notional switched.

So we can add to the disclosure of 7,000 transactions with €350 billion gross notional.

Open Interest

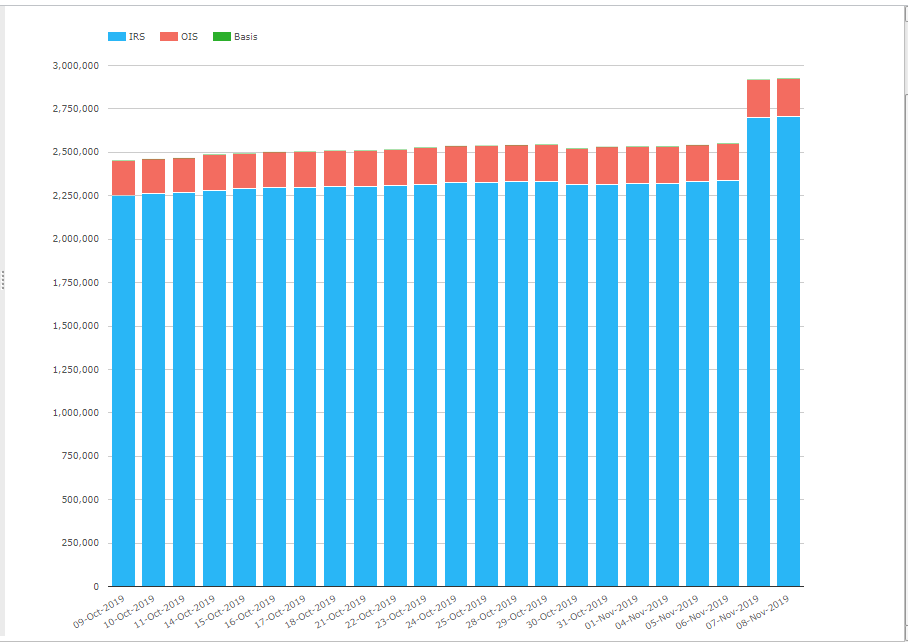

Switching from volume to open interest (outstanding notional).

We see the sharp uptick with EUR IRS outstanding notional increasing from €2.34 trillion to €2.7 trillion, an increase of €360 billion or 15%, a significant amount indeed.

LCH SwapClear and Eurex

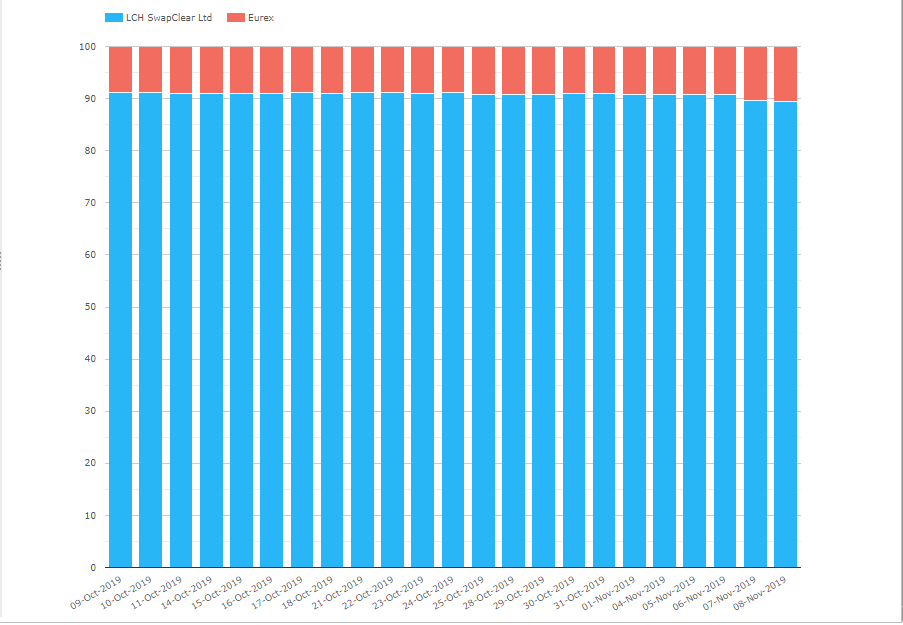

Next we can look at what difference this transfer makes to the market of Eurex in EUR IRS versus LCH SwapClear, in terms of outstanding notional.

Showing an increase in Eurex share from 9.23% to 10.45% on 7-Nov and then to 10.63% on 8-Nov. While in outstanding notional terms, Eurex is up from €2.3 trillion to €2.7 trillion and LCH SwapClear is down from €23.1 trillion to €22.8 trillion.

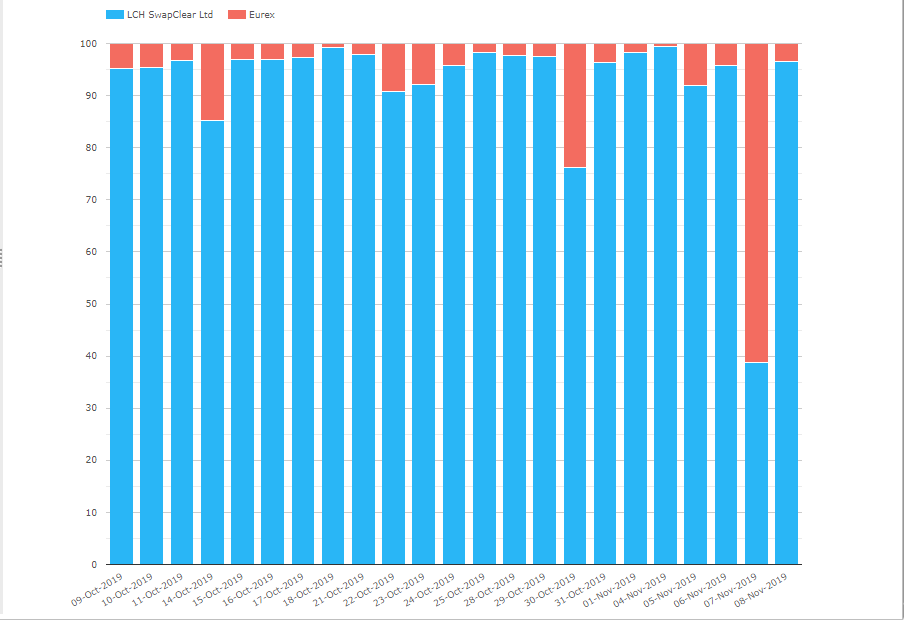

While switching to volume and percent share by day.

We see the transfer on 7-Nov stand-out as well as a large days at Eurex on 30-Oct.

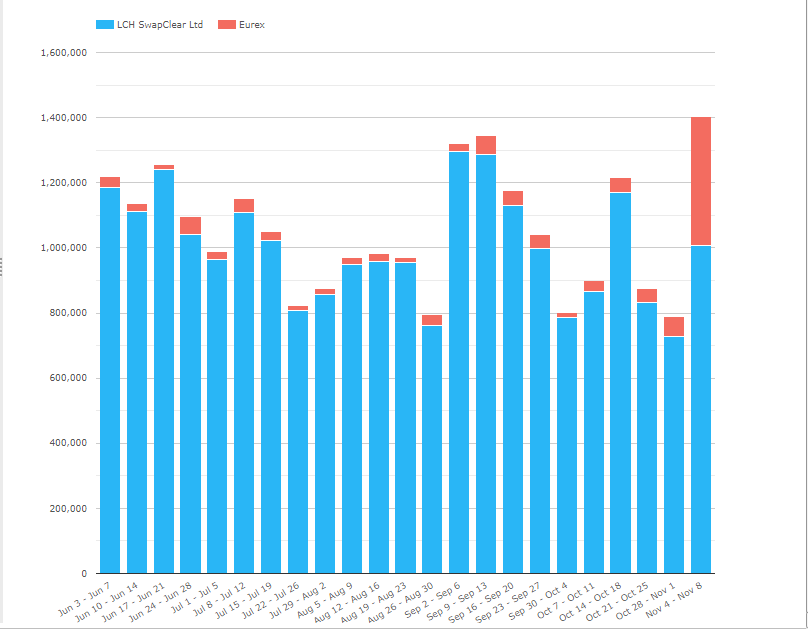

Switching to weekly volumes since June 2019.

The week of 4-8 Nov, which includes the DekaBank transfer stands out, however even in this this week, LCH SwapClear had more volume in EUR IRS. Excluding last week, the average share of volume from May 2019 onwards for EUR IRS is 3% for Eurex.

Volume vs DV01

It would be interesting to know how much DV01 risk was transferred by DekaBank, as that is a better measure of the significance of the transfer. All we would need to estimate the DV01 would be volumes by tenor bucket, which we have for many CCPs that clear Swaps, such as CME, JSCC and LCH. Unfortunately, we do not have this breakdown from Eurex.

Transfer Mechanism

The other detail that interests me is on the how the transfer happened operationally? It is not a simple task to transfer 7,000 swaps and 350 billion gross notional.

DekaBank as a clearing member at both Eurex Clearing and LCH SwapClear, would not be in the position of a client that needed a member to agree to the transfer. However it would have needed counterparts to take-off the risk at LCH and put it on at Eurex as well as understand the costs economics of the transfer, in terms of:

- variation margin as EUR LCH/EUX basis is -0.15 bps

- initial margin change at each CCP

- default fund contribution change at each CCP

- clearing fees at each CCP

- any netting or compression used to reduce the number of transactions

- use of any services to assist with the switch process

As we don’t know the direction and risk transferred by DekaBank, we cannot know if the transfer resulted in a cost or a benefit in economic terms. We can say that Dekabank clearly decided it was better to move its Swap book to Eurex and now was the right time to do so.

Other Currencies

I expect the vast majority of Dekabank’s swap book is in EUR and most likely the whole book was transferred, but if Dekabank also had swaps in other currencies at LCH, there is no evidence that these were switched on 7-Nov as only $15 million of USD IRS and $16 million of GBP IRS was reported by Eurex on that day.

It may well be that DekaBank does not have any non-EUR Swaps at LCH SwapClear or if it does, they are held in a client account and not it’s house account.

Summary

A transfer of €350 billion and 7,000 trades is significant indeed.

It increases the EUR IRS outstanding notional at Eurex by 15%.

Taking it’s share in EUR IRS to 10.6% vs 89.4% at LCH Swapclear.

It will be interesting to see when/if other large transfers happen.

CCPView will show the spike in volumes on those days.

It will be interesting to see how Eurex daily volume share develops.

Will it increase from 3% to something like the 12% that CME has in USD?

And if so, how long will it take to get there.

Good article. Good open questions.

Regarding the Transfer Mechanism: If DekaBank had been the dealer/other side of each of the swaps originally, would it be able to move them intact without searching for counterparties? The payout and collection of margin for all of the swaps might have required quite a bit of orchestration and probably some financing, n?

Thank you for your comment and good points.

The other observation pointed out to me by a reader is that as the LCH/EUX basis did not move on this day or over the period, it is likely that the transfer though large in gross notional terms will have been flat or low in risk exposure/dv01 terms.