- Four providers have entered the race to provide term SONIA fixings.

- These terms fixings are intended to ease the uptake of SONIA and made the transition easier for end-user cash markets.

- The providers are LSEG, ICE, Refinitiv and Markit. We look at their proposals.

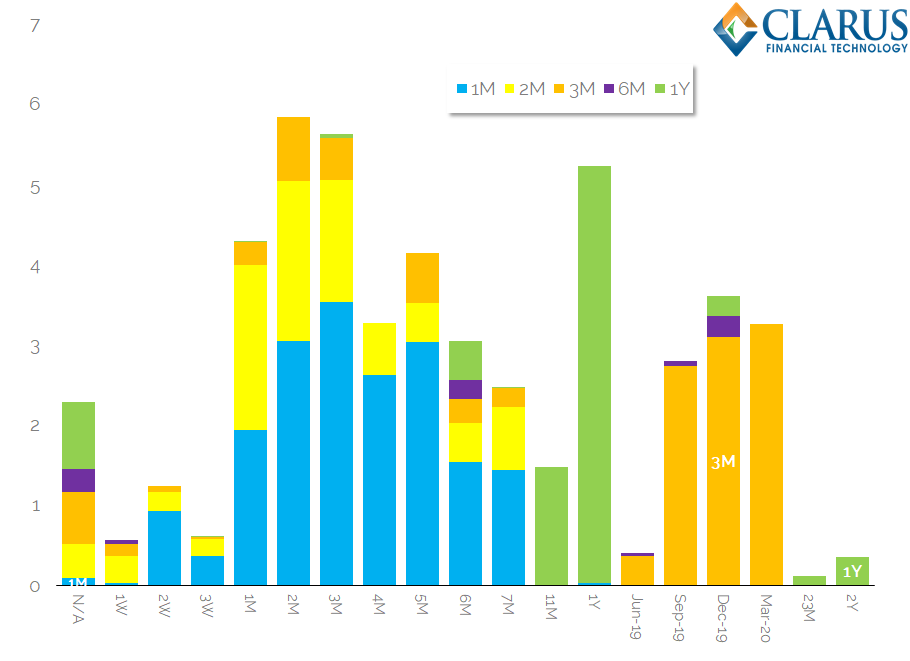

- Looking at the SDR data we find that 80% of SONIA risk currently reported is forward starting.

- Does this suggest that a successful term fixing will need to incorporate the information embedded in these forwards to be truly representative?

Since May 2019, four benchmark administrators have thrown their hat into the ring to produce credible Term SONIA Reference Rates (TSRR). This work is being supported by the Risk Free Rates Working Group, who have developed a new Task Force to help provide market-wide input.

From the Statement, it looks like the use of these term rates will be focused on areas of the market that are unable to transition to compounded overnight in-arrears SONIA. This follows on from the 2018 consultation on term rates, which identified demand for term rates from certain cash markets (responses here, including our own).

Whilst reading the below, bear in mind the following risk profile of SONIA risk reported to SDRs in the past six months:

FTSE Russell (LSEG)

This is an interesting one, with some big names attached:

- FTSE Russell will be the benchmark administrator.

- LCH will provide transaction details.

- Tradition will provide quotes from the electronic trading platform Trad-X.

- TP ICAP will provides quotes from the electronic trading platform i-Swap.

The presentation does not include precise details on the calculation methodology, but states that they are keen to consult with the broader market to develop a methodology. From what I can ascertain from the presentation:

- There is a preference for a point-in-time fixing, instead of a volume weighted average over a whole trading day.

- There are not enough actual transactions in spot-starting OIS to create a fixing from transaction data alone.

- Quotes fed into a Central Limit Order Book can help to improve transparency in spot-starting OIS transactions.

I guess LSEG plan to license quote data from Trads and TP ICAP, and back it up with actual transactions at LCH. The downside being that, under the current market infrastructure, there are not enough actual transactions (or binding, executable quotes) to be able to create a robust term fixing.

Therefore, changes required from the market will be:

- Establish CLOBs at the two IDBs.

- Encourage trading of spot-starting OIS.

Nothing too surprising in this proposal, other than the requirement for the market to start quoting (and trading) spot starting OIS, that don’t really trade yet.

On to the next one…

ICE

ICE are already the administrator of LIBOR – it’s no surprise to see them developing a methodology! They also administer the ICE Swap Rate (previously ISDA Fix) used mainly for Swaptions, so they have form in this space.

In terms of robustness, they appear to be trying to cover all bases. The methodology includes:

- Spot starting 1M, 3M and 6M SONIA OIS swap transactions. I assume they’ll take these from SDRs, APAs, MTF transaction reports? Good luck actually using the MIFID II data…

- These may (or may not) be complemented with quote data as well. I guess they too will need CLOBs for that quote data to be robust enough.

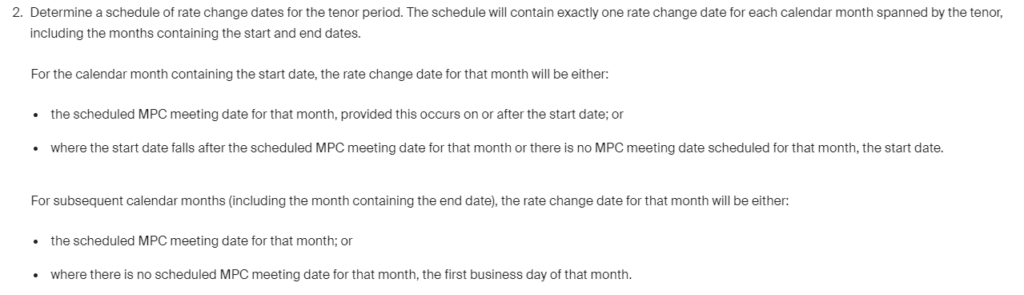

- If there are insufficient transactions and/or quotes, the methodology will fall-back to futures quotes, transactions and prices. The futures prices are combined using a step-up function per MPC date (as detailed under “Show Methodology” on the ICE RFR Portal).

The Step Function is very simple. I can’t stress this enough. The model is basically to pick one day per month when SONIA can actually change. Normally this will be the day after the MPC decision is announced. But if there is no meeting that month, it is the first day of the month.

ICE therefore deserve credit for using multiple sources of transaction data as possible. However, I am a little surprised that they don’t also propose using forward starting OIS in the model. Aren’t forwards an even better input to the Step Function than futures?

The paper is also explicit that they have not yet decided whether to:

- Employ a point-in-time fixing (with say a two minute observation window).

- A fixing window – e.g. 9am til 11am.

- A whole day.

On to the third proposal….

Refinitiv

The proposal;

- Use CLOB quotes for spot-starting term OIS.

They acknowledge that there are not currently enough transactions to create a robust fixing, and also acknowledge that there might not be a CLOB to use either. Therefore as a first level of a waterfall approach indicative quotes could also be used:

- Data taken from both D2D and D2C platforms.

- Random samples could be taken – either over different windows, or averaging or using a median quote.

This approach is consistent with the first stages of both the LSEG and ICE approaches. I cannot see an explicit backing by the platforms (maybe Tradeweb are involved?) or a futures/forwards-based input for other transactions. Therefore, it doesn’t seem to differ too much from the other two approaches.

Will the Refinitiv/LSEG proposed merger change things here?

Nonetheless, it is notable that the first three proposals are quote-based, assuming CLOBs can be created in spot-starting OIS.

The final proposal is different…

IHS Markit

Whilst all of the other three providers presented their solutions in May 2019, Markit didn’t appear until September 2019. No idea what the delay was, but let’s see where this approach differs…

- Purely transaction based. Now that IS different.

- OIS and Futures based.

- Both spot- and forward-starting. Again, different.

- Volume-weighted calculation. I think this is different as well.

- Transactions across a variety of Trading Venues and CCPs.

- Eligible transactions must be cleared with at least one dealer involved.

The paper outlines a “calculation engine” which might set some alarm bells ringing regards complexity/transparency. However, it seems to be pretty simple in that it:

- Allocates OIS trades to each day it references the underlying rate.

- Calculates a volume-weighted average using observed transactions each day.

- By extension, if there is no transaction data covering a future date, then the model must use some type of interpolation.

- Let’s assume a step-rate function similar to the ICE futures model? The paper only describes an “end-of-day base curve” so it’s not 100% clear.

The Term Rate is calculated using this input curve data.

The paper doesn’t state explicitly where the data comes from, however it’s got to be from MarkitSERV data, right? From a SONIA perspective, it is hard to imagine where that might be different to the LCH data that LSEG reference on any given day?

It seems positive that this administrator is willing to look at combining spot- and forward-starting OIS, as it tends to be much easier using existing data rather than convincing a market to change what they quote and/or trade.

Where is the Data?

I do not know whether the publicly available presentations give all of the details that were presented to the SONIA Working Group. But I do wonder why none of the presentations include data on the underlying transactions?

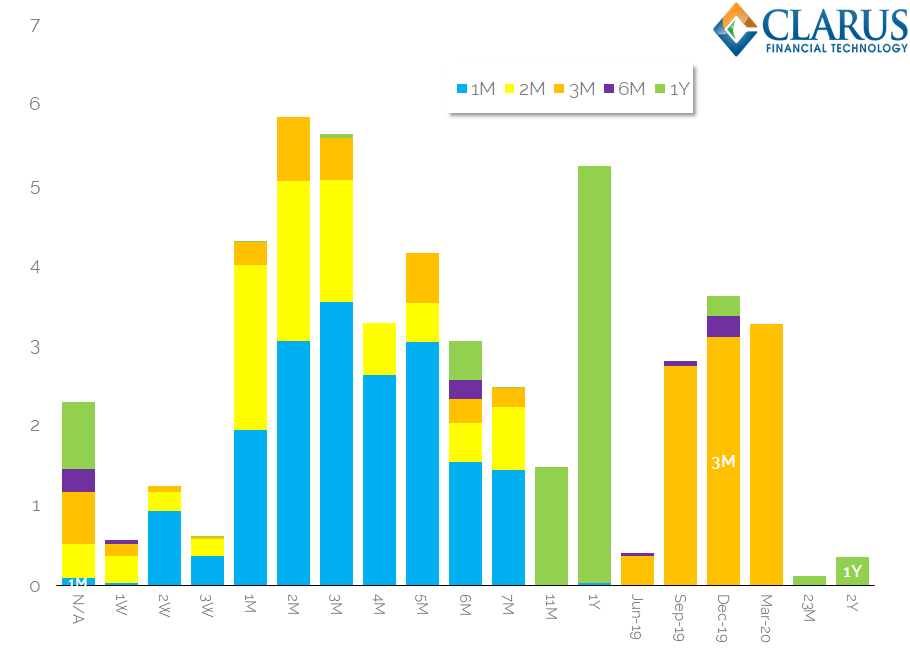

To fill that gap, here is what I can find from the past six months of trading reported to SDRs:

- A DV01 of £123m was reported to US SDRs in the past six months in SONIA OIS.

- Of this, £25m in DV01 was spot-starting.

- 80% of the risk is forward-starting.

80%! That is huge. So what is trading forward-starting?

Showing;

- Most risk is traded out of either a 1 month, 2 month or 3 month forward start.

- 1y1y trades are also very popular.

- For 3 month tenor trades, they mostly trade out of the nearest IMM date.

- For 1 month and 2 month tenors (which include MPC dated single period swaps), they mainly trade out of the next 3-4 MPC dates.

There is the possibility that this distribution of risk is skewed by the types of counterparties reporting GBP OIS risk to SDRs (maybe hedge fund heavy?). This is why I was looking forward to seeing some data out of LSEG or Markit that would show similar statistics.

Presented with this risk profile, it looks to me like we need a model that incorporates forward risk traded in OIS markets into a term fixing. Or we start using forward fixings on MPC dates, and it is up to end users or their banks to volume weight their hedges?

The downside of that is that it can be interpreted as complicated. I do not think it has to be complicated if well communicated.

It is notable that three of the four providers have preferred to incorporate spot-starting quotes into the fixing process. Maybe this is because incorporating actual spot-starting instruments aids transparency in the fixing process?

It is an interesting conundrum to solve. Will the market really start creating CLOBs in the derivatives market to solve it or do we need a Markit-like approach?

Answers in the comments below.

And of course I cannot help but note that it is a real shame that a free solution couldn’t be created from MIFID II data…

Hi Chris – a useful summary to save end users going through the presentations, which as you state lack detail in certain instances.

The official sector in the UK are pushing for a CLOB model since it is deemed easier for end-users to understand and compare to what is seen as quoted on MTFs/SEFs. Whereas I am sure ex-swap traders and market participants would consider a step function to be simple, it is not altogether trivial to implement a bootstrapper which deals with different o/n rate step dates and instrument maturity dates. I can also see why high level talk of a “calculation engine” puts people off. There are also considerations around taking too wide a fixing window, or even the entire trading session – good luck in hedging anywhere close to the fixing rate in those cases (which has been an issue with the ICE Swap Rate).

I think simplicity and transparency is really what end users of these rates will first and foremost demand. I think avoiding modeling is best for the market if at all possible but introducing some modeling as part of the waterfall shouldn’t be an issue (falling back to using a futures strip, for example). If LIBOR transition happens then volumes in spot starting trades will likely increase, whether that is from hedging of term fixing reset risk or other flows. This will keep the CLOBs “honest”. Whilst liquidity picks up and assuming market would support it (indications are there is commitment to support), using CLOB data as the top level of a waterfall would appear a good compromise. This is in fact in line with the current ICE Swap Rate methodology to pending the outcome of the ICE Swap Rate consultation, extending a similar model to shorter tenors seems achievable.