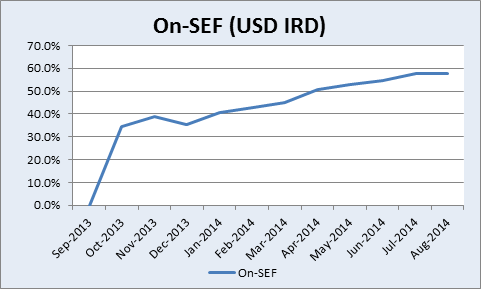

Scrutinizing the most recent OTC data tells a fairly consistent picture over the previous months. The percentage of trades registered On-SEF in recent times is, at best, inching up. In fact the preliminary August data shows no change from July, hovering right around 58% of all trades (and 67% of all cleared trades).

Let’s not forget that the late spring and early summer had the benefit of No-action relief runoffs for most of the packaged trades (curve trades, butterflies, spreadovers, etc). The only carrot, or should I say stick, left in the bag is the November “non-swap” package trades. Will that lead to any uptick? I am not even aware that anyone has gotten their head around how such a product, notably an invoice spread (futures + swap) is going to be traded pursuant to the rules. But let’s face it, even if a mysterious SEF figured it out, we might see a small uptick in adoption.

IS IT EVEN REALLY 58%

Lets first acknowledge what On-SEF actually means. If you equate On-SEF to exchange trading, you might be fooled into thinking 58% of the market is trading on an electronic order book. But we know that is certainly not the case.

This 58% of trades dealt “On-SEF” includes:

- Block Trades. 5 – 7 % of all “On-SEF” trades are blocks, as reported to the SDR. I assume many of these are traded away from, and then reported via a SEF. These aren’t really On-SEF. (note that Bloomberg has told us that much of their block trades are indeed done on the SEF. RFQ to 1, or RFQ to more).

- Trades reported by IDB SEFs have, as recently as 6 months ago, been 100% voice. While no reliable public data exists on this, we’re hearing this ranging anywhere from absolutely 0% electronic to up to 50% electronic, with some growing acceptance of an order book at a couple venues.

- Trades reported by the client SEFs are, with very few exceptions, 100% RFQ.

Hence this 58% contains a majority of RFQ and voice trading. As well as blocks that presumably are not touching the SEF until post-execution. While RFQ and voice are means of “interstate commerce” and hence allowed, this is certainly not the electronic order book envisioned in an exchange.

BUT WAIT, WHO CARES ?

So let’s take a step back. Who cares if swaps are not traded on an “exchange”, ie a SEF?

Well, the G20 told us to, and Dodd-Frank made it law. The spirit of the G20 mandates were to reduce systemic risk, increase transparency, and create an equal playing field.

The clearing mandate addresses systemic risk. And SDR reporting largely addresses transparency. So what do SEF’s address?

How about the equal playing field? The optimist says you’ll get a better deal from good competition.

But wait, you might say, this could apply to anything. I’m happy to go to Costco to buy my 84-pack of kitchen towels. They extend me credit, often have things I need at a good price, and can even rotate my tires while I’m in there. Please don’t make me go to an exchange to buy kitchen towels. I’d have to register, remember a password, read their terms & conditions (or just hit “I agree”), give them my personal details, credit card number, wait around for their delivery truck, and so on.

So if it doesn’t work for paper towels (and perhaps health care?), why would it work for swaps?

WHATS DEFINITELY NOT ON SEF

We’ve done various research, presentations and blogs on the topic of whats still off SEF. But a quick assessment; if you assume that all interbank deals are done via IDBs and hence all of their trades (ex-blocks) are making their way onto SEF, that massive gap of Off-SEF trading is due to clients trading away from SEFs.

Further, if you can stomach the detail of my research in July, you’ll see that the market is trading a significant amount of forward (non-MAT) start. A slightly smaller, but still signifcant amount, of odd (non-MAT) tenor swaps are also being done. Often a single swap shares multiple of these characteristics.

But if you read the research, the kicker is: This has always been true. The OTC market started as a bespoke market, and that bespoke element still exists. These trades will not be on SEF until those trades are MAT’d.

WHERE WE ARE

We seem to be in this middle ground:

- At one end of the spectrum, the end users / consumers are exempt or trading the usual tailored bespoke products with a dealer. They might clear these, but there exists little reason to do them on SEF.

- At the other end of the spectrum, banks are trading “on” the IDB’s SEFs. Much of this is voice, but a couple in particular are making great strides in electronic. Bulk of this is standardized products, and makes up the majority of what we see on SEF.

- The vast middle ground includes small banks and buyside. Some of them say they will not trade on SEFs, while some say they will only trade on SEFs. All have their reasons. But whats true here, is there are a lot of non-MAT-able trades among this bunch. And if they are not MAT, they very likely won’t be going on SEF any time soon.

WHAT SHOULD WE DO

So what I’ve been pondering is:

- Should we MAT the entire curve?

- If we do, and even if 100% of swaps trade on-SEF, how will we be any better off?

- You can’t put non-standard, bespoke products onto an order book. That simply wouldn’t work. But how is that any different from all the standard, MAT-able trades that are trading as RFQ on-SEF?

- Who stands to gain (and lose) from putting more onto SEFs?

I’m going to have to save thoughts on that until next week. Of course I welcome comments (public or private) until then.