- A large proportion of JPY swaps activity at JSCC has moved to JPY TIBOR.

- JPY LIBOR swaps have shrunk from 89% to just 66% of the market.

- At the same time, overall JPY IRS volumes have drastically shrunk.

- We look at the data behind cleared JPY IRS markets.

A Bloomberg article last week flagged to me that TIBOR use is increasing in JPY swap markets:

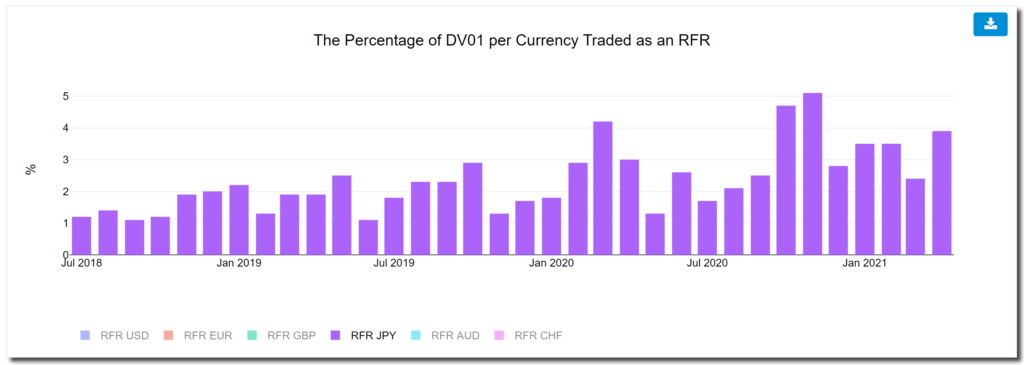

As we have long noted here, it is of particular concern that JPY TONA use just doesn’t seem to be accelerating. When we look at our RFR Adoption Indicator for JPY, it is still stuck below 5%, despite the upcoming cessation of JPY LIBOR at the end of this year:

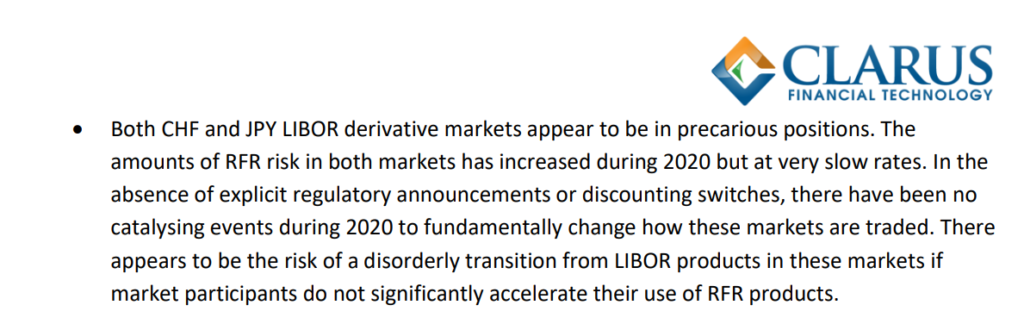

As we noted in our response to the ICE LIBOR consultation earlier this year:

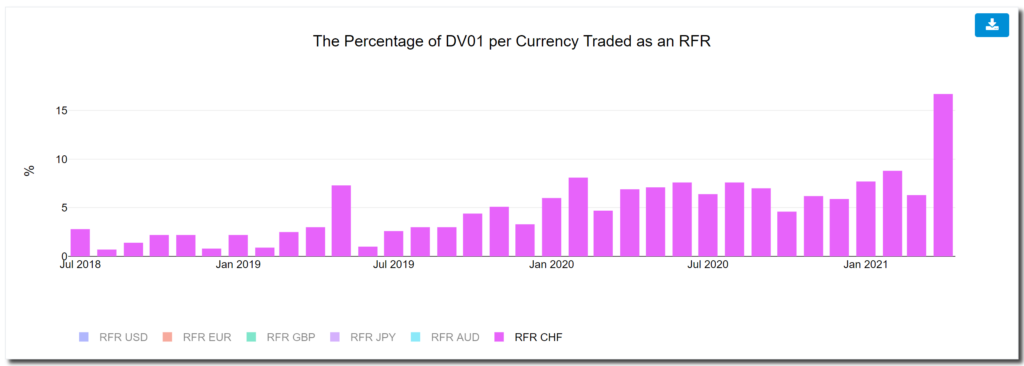

Happily, at least CHF markets appear to have taken note. Last month saw a huge jump in SARON risk traded, reaching new heights in terms of absolute volumes and as a proportion of the overall market:

We will cover the CHF story in more detail in another post. This is about JPY markets. So what gives?

Cleared OTC JPY Swaps

There are two CCPs who enjoy meaningful market share in JPY IRS clearing – LCH SwapClear and JSCC. As we saw last month, their market share is fairly evenly split, but they have particular strengths in different tenors.

The first point to note here is that LCH SwapClear does NOT clear TIBOR swaps. The website lists only JPY LIBOR swaps:

Therefore, whilst LCH and JSCC have a roughly 50/50 split in JPY IRS, this means this blog is focused only on the half of the market cleared at JSCC. A bit more analysis of the overall JPY market is shown below from our blog last month:

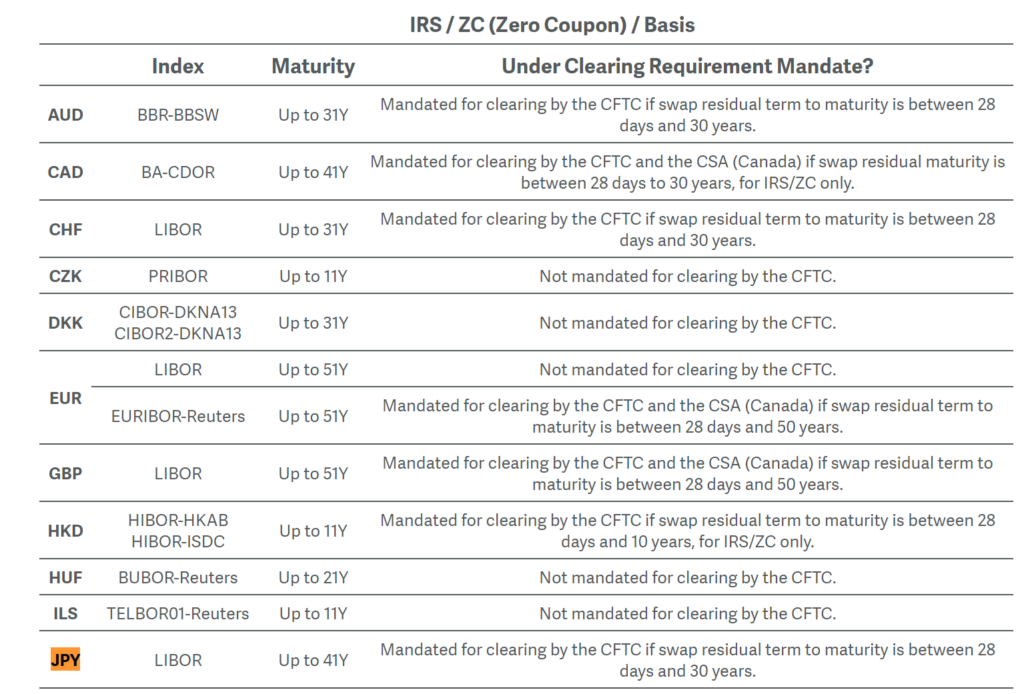

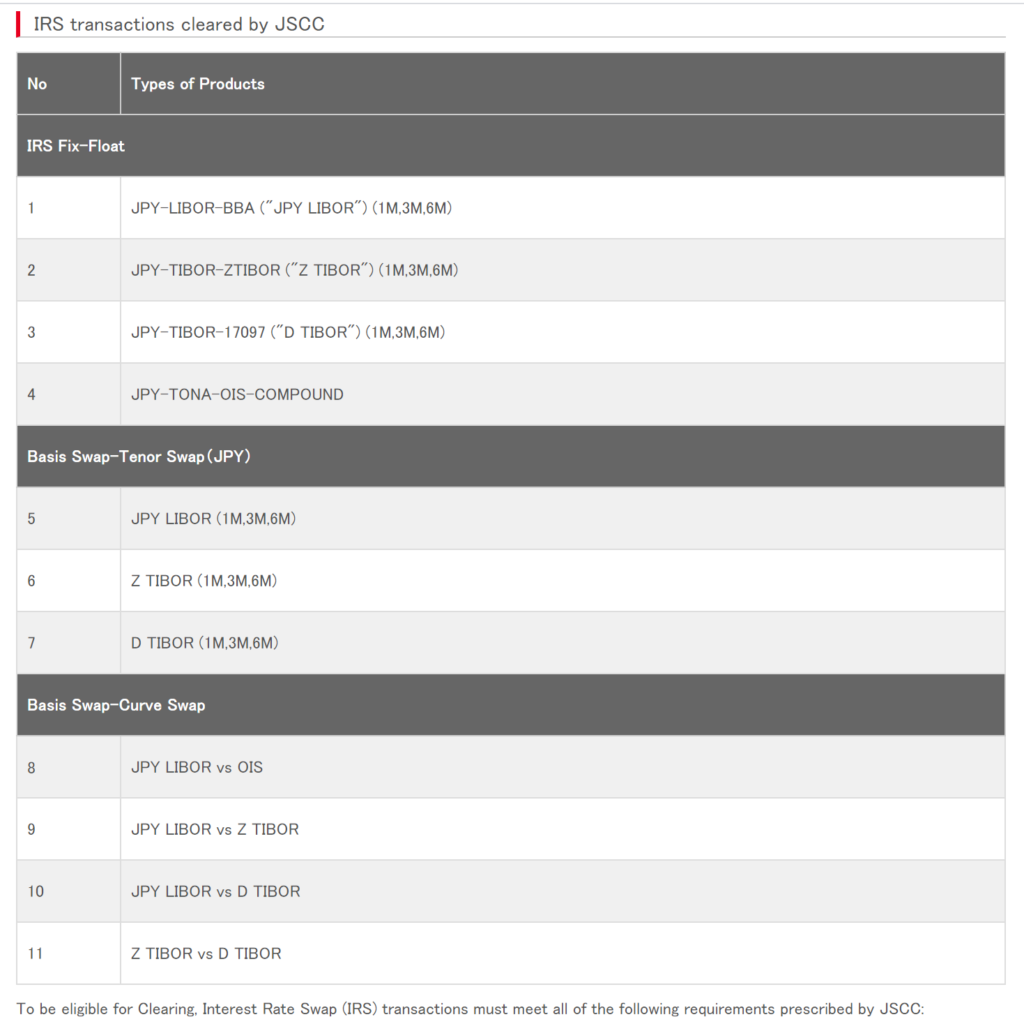

In terms of the JSCC offering in cleared TIBOR swaps, their product support is very broad. These are not just basis LIBOR-TIBOR swaps we are talking about here!

Data – JPY TIBOR Clearing

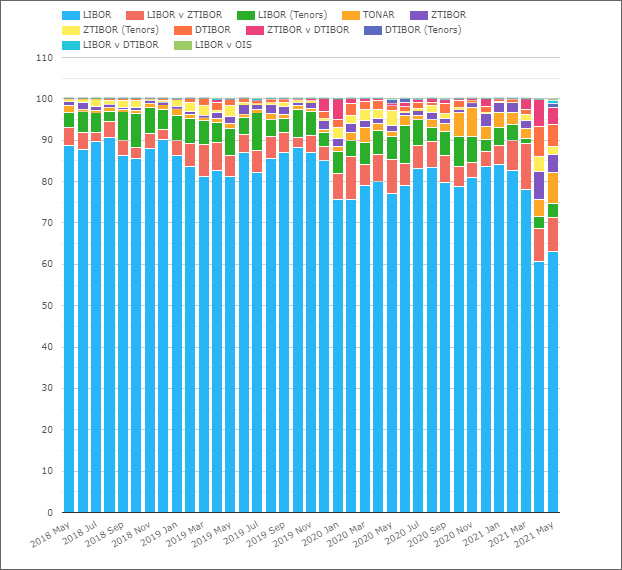

On to the data. The Bloomberg article focuses mainly on the price action in the LIBOR/TIBOR basis, only briefly mentioning volumes in the final paragraph. I thought I should flesh that out and show what TIBOR volumes have been doing recently. From CCPView, looking at only JSCC volumes in JPY IRS:

Showing;

- The percentage of DV01 volume traded by product type in JPY at JSCC.

- The blue bars show pure LIBOR-referencing swaps.

- TONA is in orange.

- Everything else is TIBOR-related.

- Prior to March 2021, LIBOR swaps accounted for 89% of volumes.

- In May 2021, LIBOR swaps accounted for just 66% of volumes.

- A 23% swing in favour of non-LIBOR swaps is clearly significant here.

Are we therefore in the midst of witnessing a shift of onshore JPY clearing into TIBOR-denominated swaps?

In terms of TONA market share;

- 2% of JSCC volumes were related to TONA products prior to March 2021.

- This has increased recently, to reach 7.46% in May 2021.

So TONA is winning some volume from LIBOR. But the biggest beneficiary at JSCC has been TIBOR swaps.

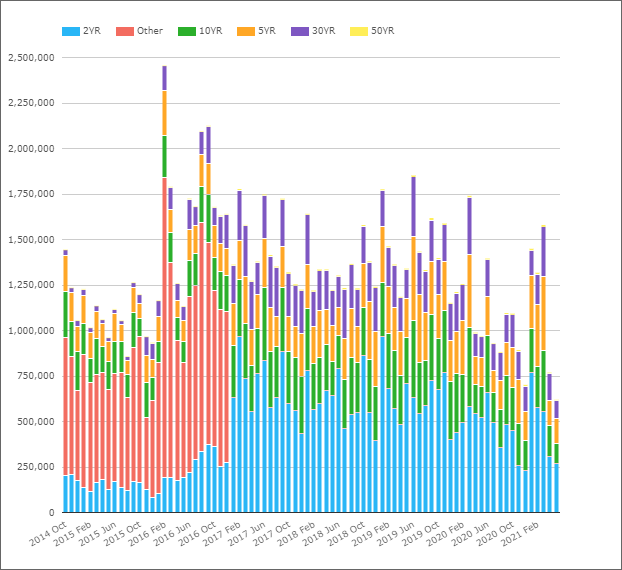

JPY Cleared Volumes

Let’s look at more JPY data for the cleared IRS markets.

First up, we have to note that May 2021 was an extraordinarily low volume month for JPY swaps. Across all CCPs and all IRS products it was the lowest volume month in notional since at least 2014! Gulp. That’s not a great transition story….

Showing;

- A complete plunge in JPY IRS volumes across LIBOR and TIBOR products in May 2021.

- December 2020 was also a very low volume month which quickly recovered in January 2021.

- However, both April and May 2021 have seen really low volumes. We hope this isn’t related to the cessation of LIBOR (although I guess it cannot be helping things!).

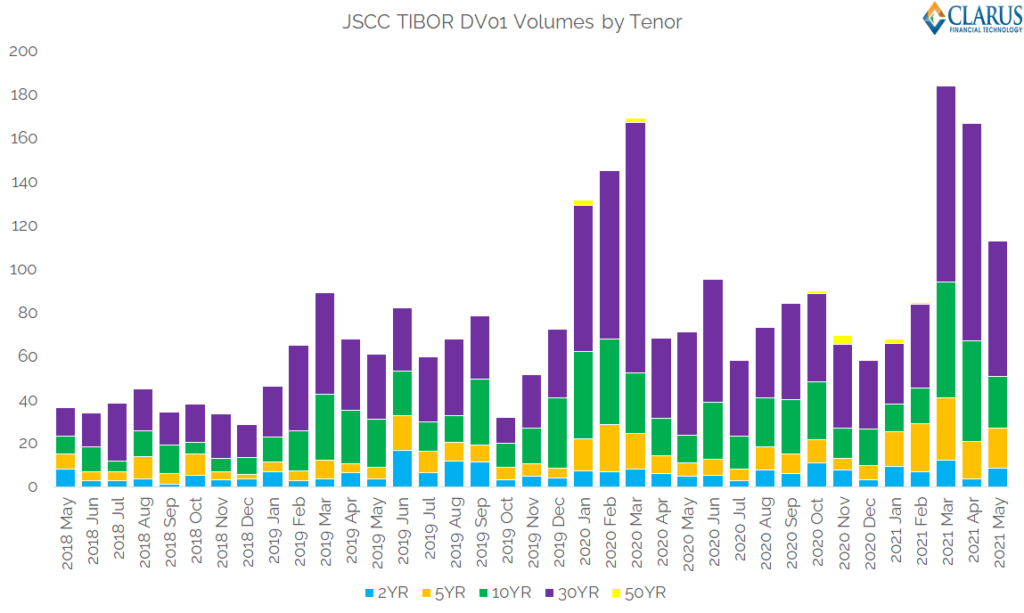

JPY TIBOR Volumes by Tenor

The relative plunge in JPY IRS volumes across the whole market puts some perspective on the next chart, showing DV01 traded each month in TIBOR-related products:

Showing;

- May 2021 was not a record month for the absolute amount of TIBOR risk traded. However, it was well above the 3 year average.

- May 2021 saw $113m equivalent of DV01 traded in TIBOR related products.

- This is someway off the highs of $165m+ reached in both April 2021 and March 2020. (Is there something about this time of year that sees a lot of TIBOR risk traded?).

- The chart shows that 30Y TIBOR products are the most traded tenor. These long-dated products account for over 50% of TIBOR volumes per month.

- 50Y TIBOR is a tiny market. That has not changed recently.

- In TIBOR space, it is fair to say that 30Y volumes are twice as large as 10Y volumes. Likewise, 10Y is about twice as big as 5Y and again 5Y is about twice as big as 2Y. TIBOR is a long-dated market, which makes the lack of 50Y activity a little surprising.

- Overall TIBOR volumes as measured by DV01 have more than doubled since March 2021.

- DV01 volumes across the whole of the curve have increased to $154m from $68m per month in the previous 3 years.

Q1 2020 saw a big spike in TIBOR volumes. But all IRD products saw record volumes in Q1 2020 as a result of the market volatility, so it is pretty tempting to discount those observations.

The more interesting point will be whether overall JPY IRS volumes recover in June 2021, and whether TIBOR will continue to grab more market share, at the expense of LIBOR products.

All the while remembering that this is a move limited to JSCC cleared swaps (which I think means mainly the onshore JPY market) for now. It could only be replicated for the broader market if another CCP also began offering TIBOR clearing in JPY swaps.

In Summary

- JPY LIBOR swaps have shrunk to just 66% of volumes at JSCC.

- JPY TIBOR swaps have been the biggest beneficiary

- There were record TIBOR volumes in March and April 2021.

- A record proportion of JSCC swaps were traded versus TIBOR in May 2021.

- However, JPY swap market volumes have reduced drastically in the last couple of months across all CCPs.

- What will the end state of the JPY IRS market look like? The data will be interesting!

Thanks for the analysis. It would be great to see if there’s evidence on whether the JPY the cross currency swap market adopts TIBOR instead of TONA as reference index for floating leg.

No, no evidence yet of TIBOR vs USD LIBOR trading in USDJPY. That kind of makes sense seeing as usage of USD LIBOR will be limited from the end of this year by regulatory definition. The SDRs are reporting TONA vs SOFR, but no TIBOR vs USD LIBOR.