Following on from my article SEF MAT Week6, USD IRS, Massive Volume in Forwards, this week I will look at:

- USD IRS for Week 7 (Mar 31- Apr 4) and Week8 (Apr 7-11)

- Market share in USD IRS by SEF

- EUR IRS Volumes

- Market share in EUR IRS

WEEK 7 and Week 8

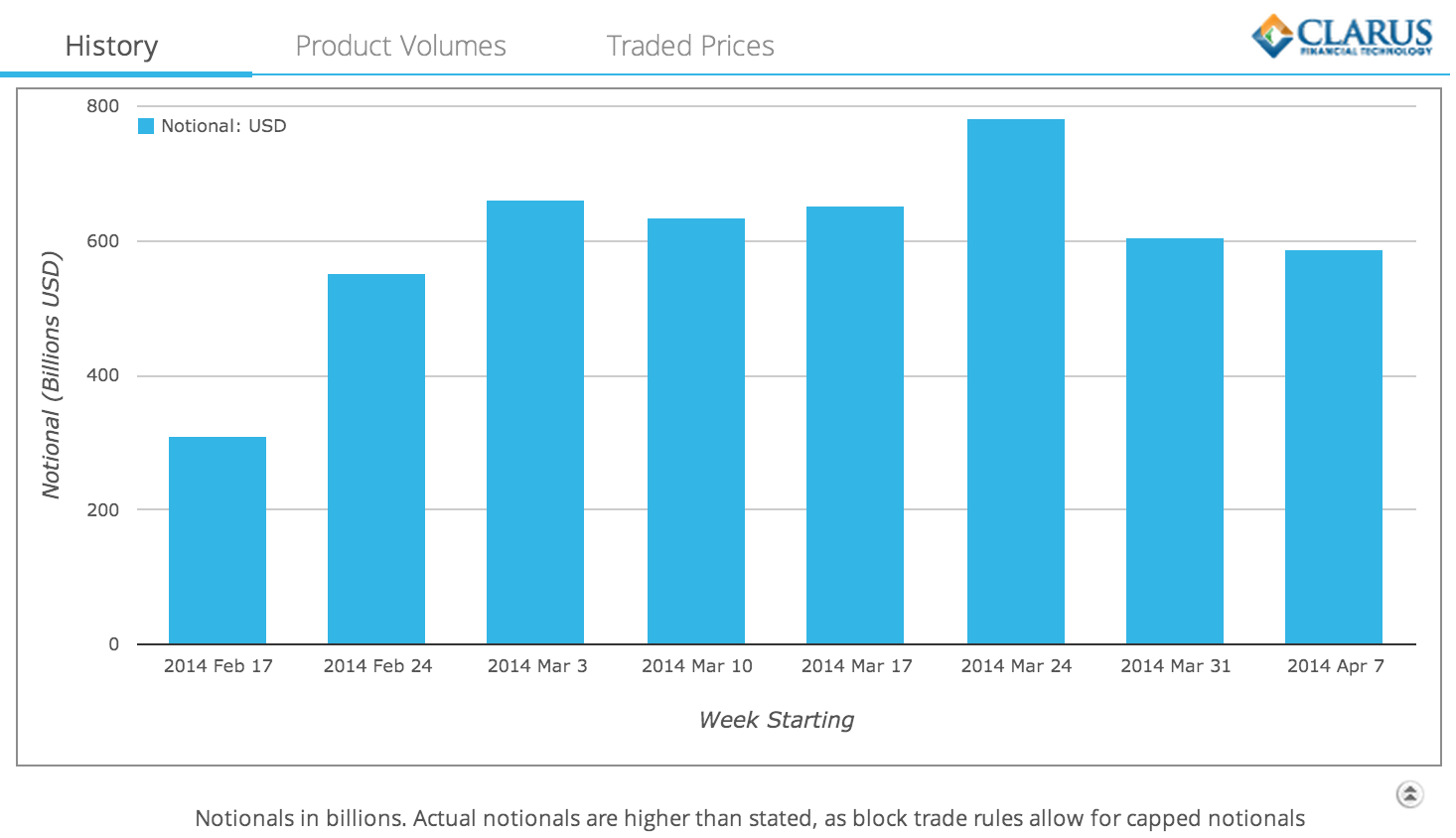

Lets start with a chart from SDRView Researcher of weekly volumes for all USD Interest Rate Swaps in the eight week period starting from MAT week of February 17, 2014.

Both Week 7 and 8 show similar volumes to Week 5, so nothing of interest to report here.

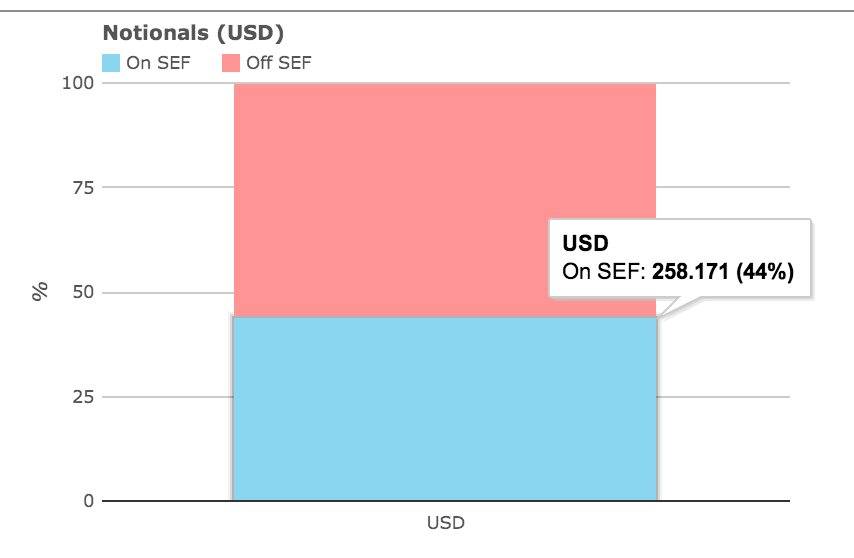

Lets look at USD IRS in Week 8, split by On SEF and Off SEF

Which shows:

- On SEF is > $258 billion or 44% in gross notional terms

- Off SEF is > $329 billion or 66%

- Total USD IRS is > $587 billion

- In Trade Count terms, 51% is On SEF and 49% Off SEF

- Both these compare favourably with the 33% in Week 3 (see Week 3 On SEF percentages)

SEF MARKET SHARE

Now onto volumes reported by SEFs using SEFView.

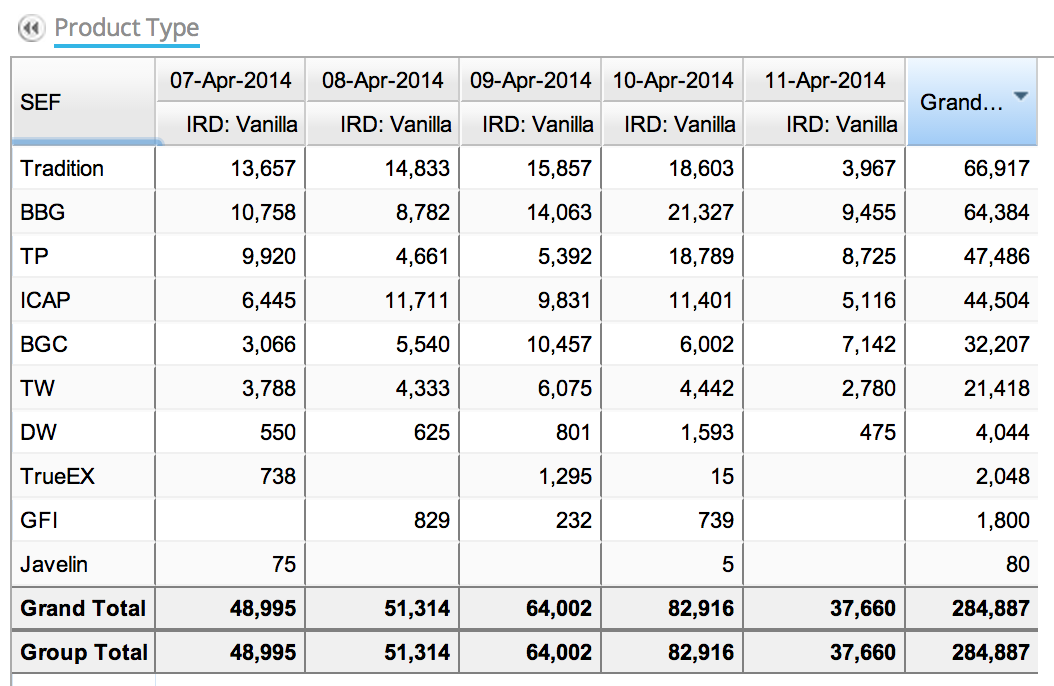

Lets start with a table just for Week 8 (amounts in $ millions)

Which shows:

- Gross Notional for Vanilla IRS as $285 billion

- Higher than the SDR figure of $258 billion

- Higher by $27 billion

- Which is explained by the Capped amounts in SDR

- As $49 billion of trades in SDR are capped below their actual notional

- Thursday 10 April was the busiest day

- Friday 11 April the quietest

- Market Share is as prior weeks

- The four IDBs split by Bloomberg

- TradeWeb, DealerWeb, TrueEx, GFI, Javelin

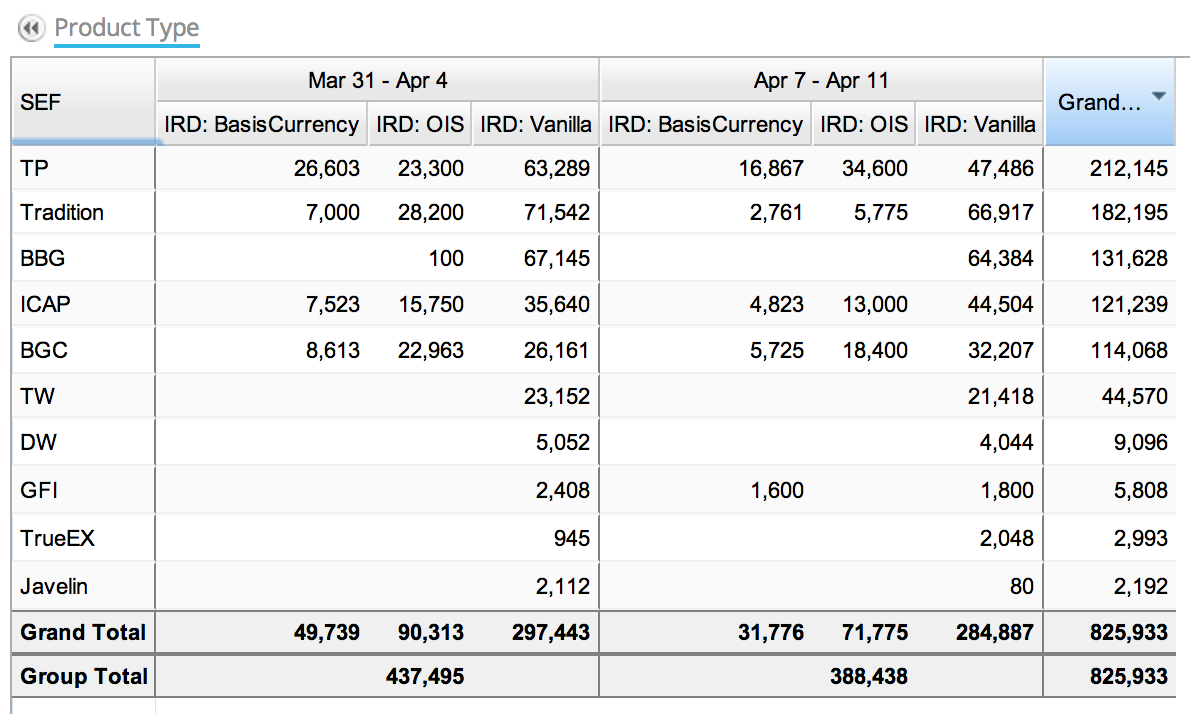

Lets now look at Week 7 and 8, this time also including OIS and Basis Swaps

From which we can see:

- Basis Swap volumes are $50billion and $32 billion

- TP has by far the largest share of 50% in Basis Swaps (Libor 1M v 3M, Libor vs FedFunds, …)

- Only the four IDBs plus GFI in Week 8 have volume in Basis Swaps

- OIS volumes are roughy double Basis Swaps volumes

- TP also has the largest share in OIS

- Only the four IDBs have volume in Basis Swaps

- Vanilla IRS volumes are $297 billion and $285 billion

- The four IDBs split by BBG is as before

- (See Week 6 comments on Curve Trade and Butterflys)

- Javelin shows $2 billion in Week7

- Which if we drill-down comes from $1.4 billion in 4Y CME vs LCH Swaps

- TrueEx shows $2 billion in Week8

- Which is we drill-down comes from $1.3 billion 10Y termination and $687 million 5Y termination

- Good to see innovation in action from both of these new SEF players.

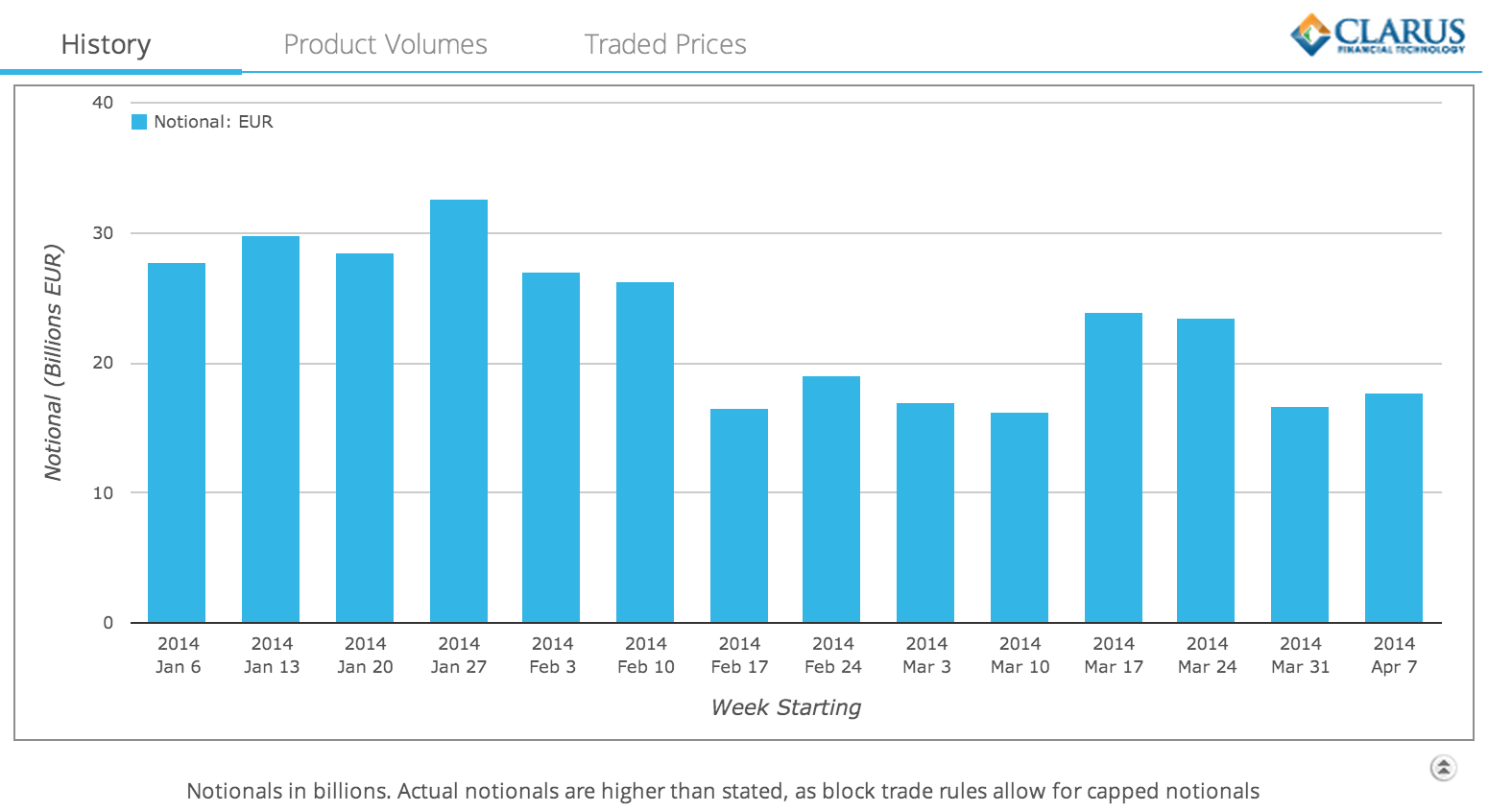

EUR IRS Volumes

A recent ISDA Research Note highlighted that On SEF EUR MAT Swap daily volume declined by 30% after that MAT rule came into effect. Lets look at chart from SDRView Researcher.

Which shows:

- A sharp drop in the MAT Week of Feb 17

- The weekly average has indeed dropped by 32%

- Using the 6 weeks prior to Feb 17 and 6 weeks after

- Unlike USD there has not been a marked recovery in volumes in subsequent weeks

- Mar 17 and Mar 24 are probably anomalies due to IMM date and Year end

- We wait to see whether volume will recover

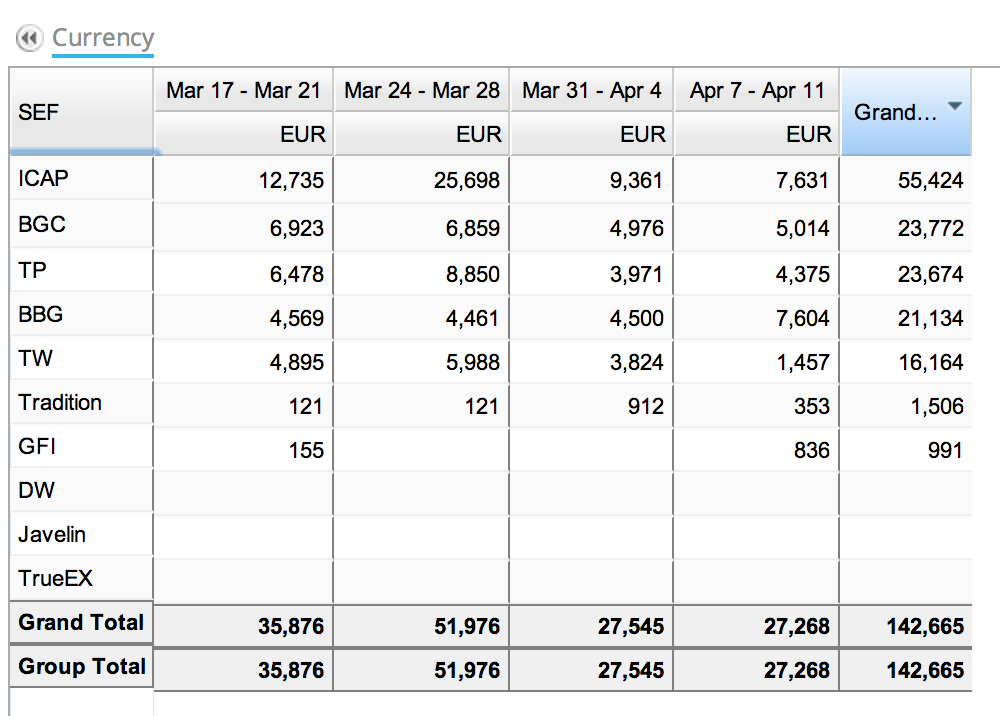

EUR IRS SEF Market Share

Now lets look at the EUR IRS volumes reported by SEFs in the pst 4 weeks using SEFView (amounts in $ millions)

From which we can see that:

- ICAP has by far the largest share of $55b

- BGC, TP & BBG follow, each with $20b

- TW has significant volume of $16b (much larger than its USD share)

- Tradition and GFI have low volumes

- Nothing from DW, Javelin, TrueEx

Summary

USD IRS Volumes in Week 7 & 8 show similar volumes to prior weeks.

On SEF share at 44% in Week 8 is higher than Week 3 (33%).

SEF Share in USD IRS is as before

Tullets (TP) has the largest share in USD Basis and USD OIS Swaps.

Javelin and TrueEx are innovating to differentiate their offerings.

EUR IRS On SEF Volumes are down 30% since Feb 17 MAT date.

ICAP has the largest share of EUR IRS.

TW share of EUR IRS is comparable to other IDBs and BBG.

Thats it for this week.