A few months ago I examined swap futures at Eris and CME, and postulated that the swap market has most certainly not moved to swaps.

While there has not been a shift to futures products, the infrastructure and behavior of the market most certainly has been “futurized”. You need to look no further than the transparency of SDR trade reporting, SEF trading requirements, and of course mandatory clearing. We’ve been futurized, we’re just not trading futures. All that’s left is standard products (OK and we need more of the trading to take place on SEFs).

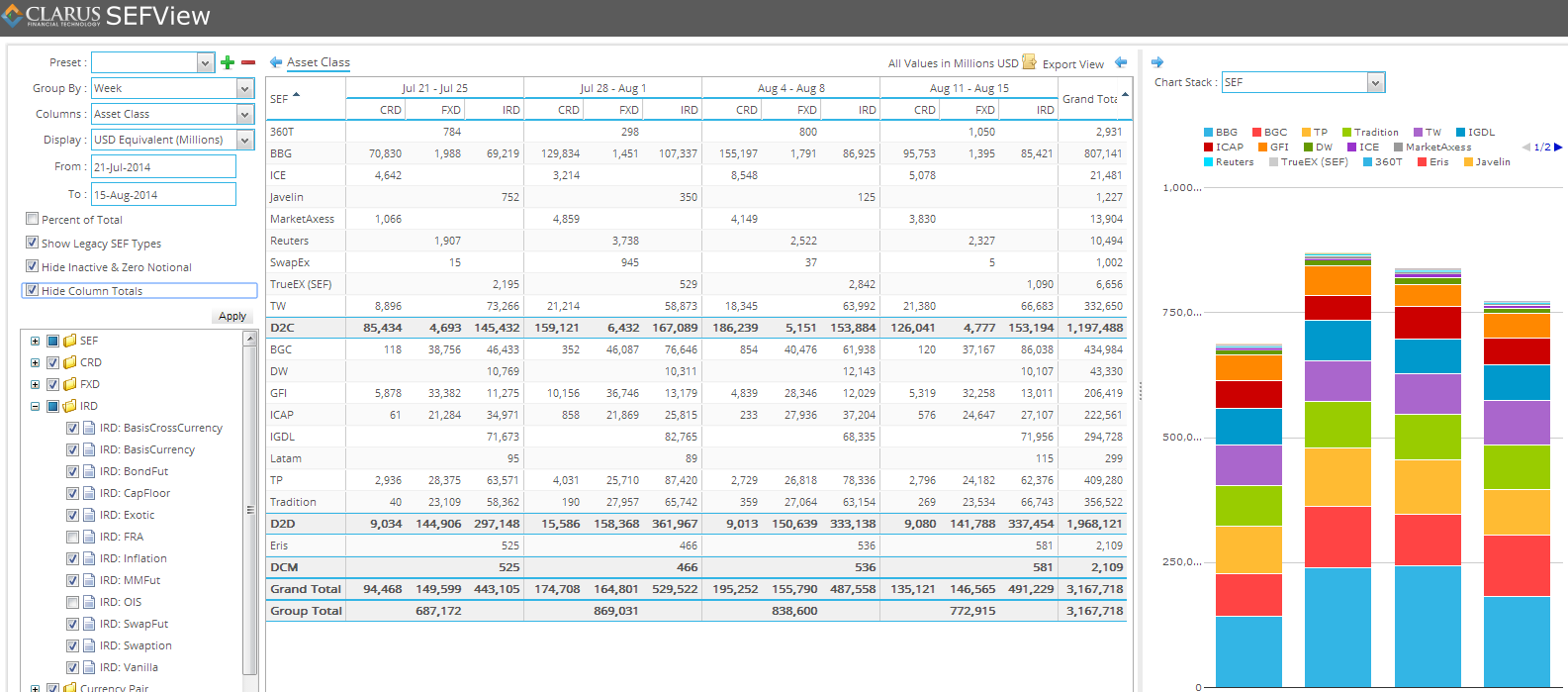

Having just completed our implementation of CME futures into our CHARM product, it got me doing some homework on the most liquid CME futures products, namely the Eurodollar and Treasury futures. I had always known this market was terribly liquid, but just how big was it really, in comparison to the swap market? So I began pulling futures data and introduced that into SEFView. We can now see just how large that market is, in comparison to OTC derivatives on SEF.

DATA

First, I need to apologize to the friendly folks at TrueEx. We at Clarus had been collecting their SEF packaged trades and DCM reports but had missed collection of their SEF RFQ volume for a couple months (they publish 3 separate reports). We’ve rectified that at the end of July but have some alterations to make to the data when that is made available to us.

With that said, lets now recap the last 4 weeks of SEF data since my last SEF activity update:

Fairly stable activity week on week, and month-on-month over the summer. In fact, its interesting that the summer doldrums just really havent happened. I suspect that the summer lull has just always been a rumor, and now that we have transparency into the OTC market, we can clearly see things keep ticking away during the summer months.

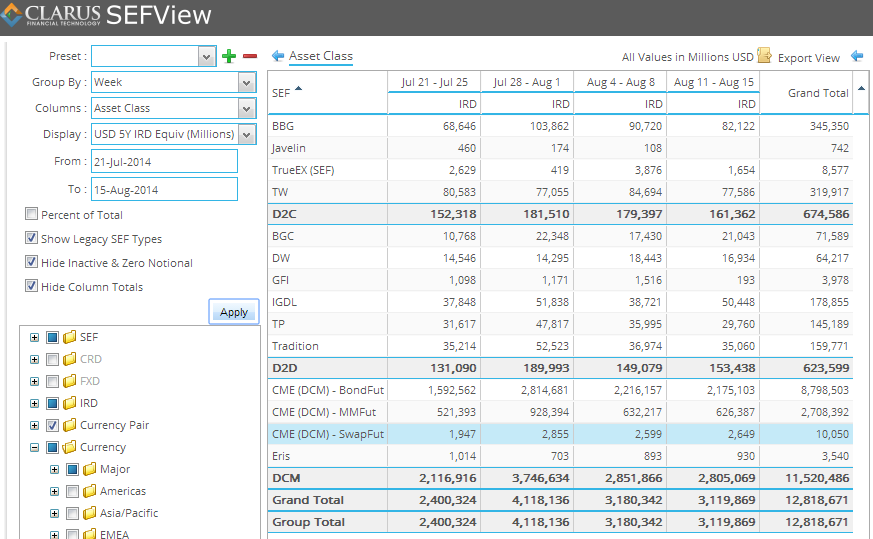

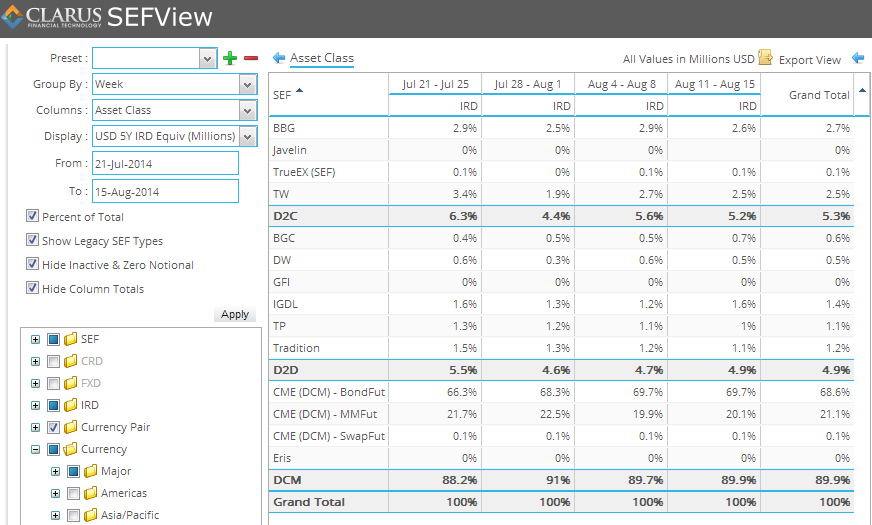

QUICK LOOK AT CME FUTURES

We can now report the notional activity of Bond, Swap, and MMK futures traded at CME. So if we pare down the activity report to show only USD vanilla swaps on the SEFs, we can benchmark that to the CME futures activity. Because the MMK futures are all short dated, its best to translate everything (both the OTC swaps and futures) into 5YR equivalents. The screenshots below show the 5YR equivalents, and then the 5YR equivalents in percentages of the totals:

This seemed to validate my suspicions of the futures markets:

- Bond and Eurodollar futures combined are 9x (nine times!) larger in risk terms than all USD swaps traded on SEF.

- If you assume roughly 50% of all USD OTC rates are being recorded On-SEF, thats still roughly 4x the total USD swap market.

- Over 2 TRILLION USD of 5YR equivalent swap risk goes through every week in bond futures alone.

With all these big numbers, its a good thing futures were futurized long ago.