The latest ISDA-Clarus RFR Adoption Indicator shows that RFR trading is really picking up across the board. I know we’ve all been waiting a while for this to happen, but finally the industry seems to be accelerating efforts to transition away from IBORs.

September 2021

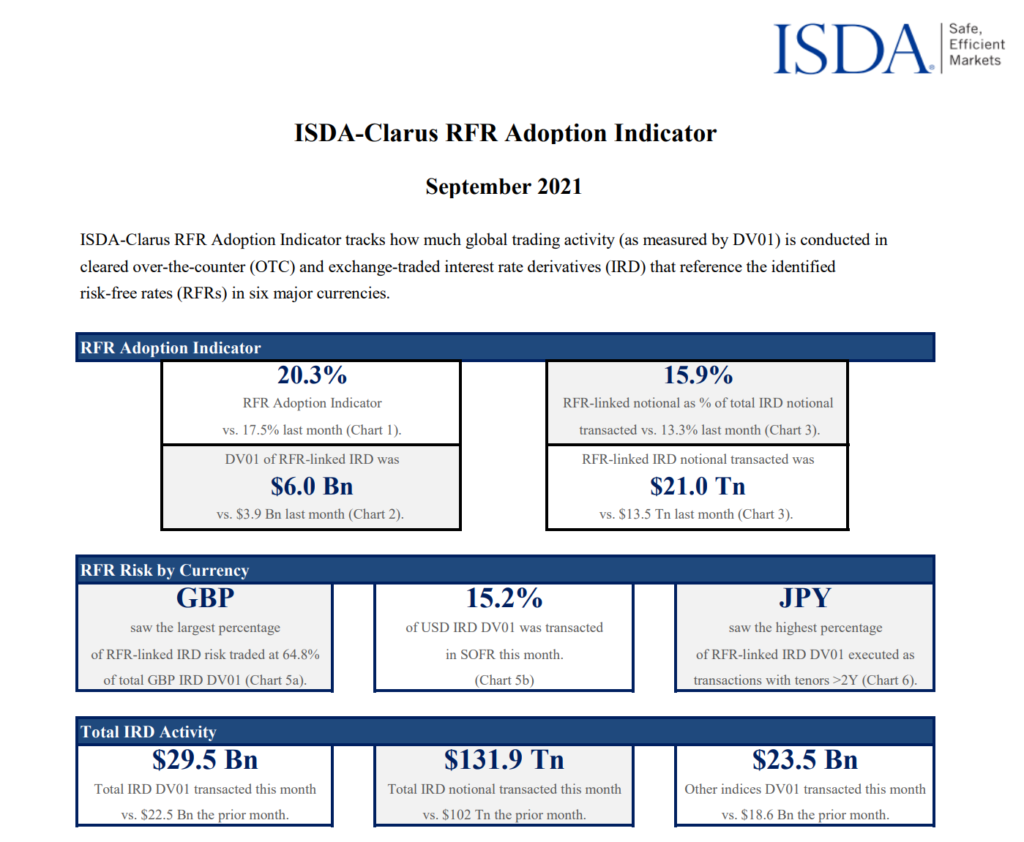

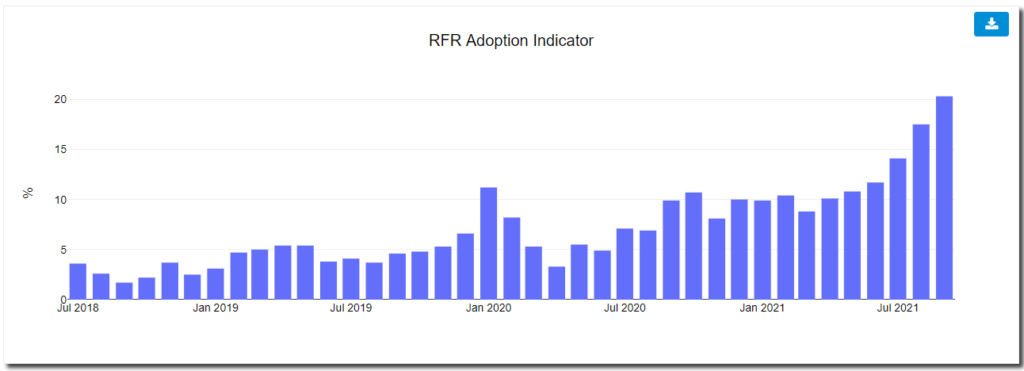

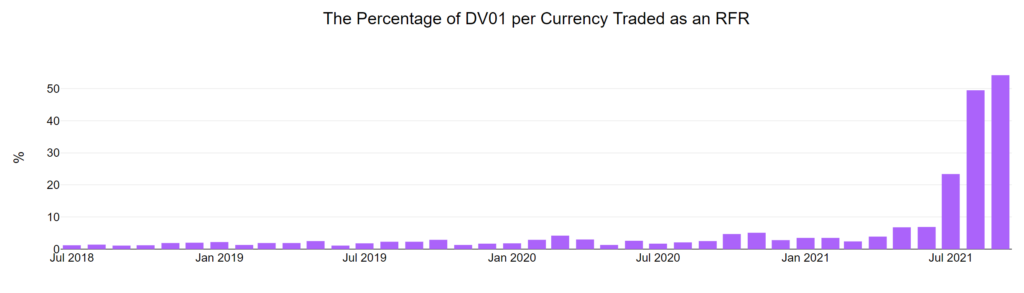

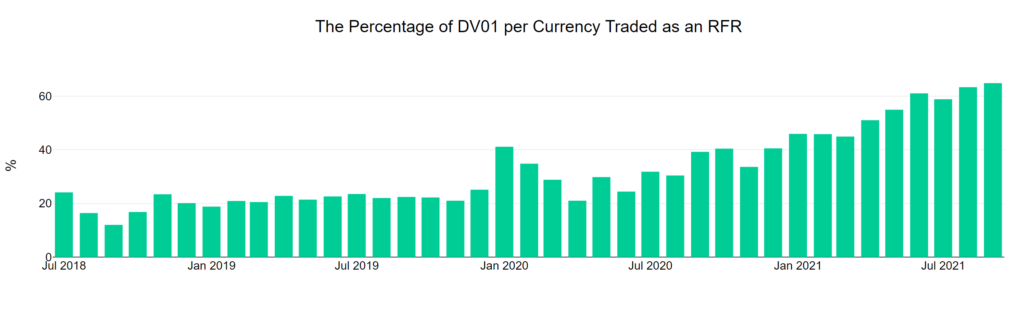

Overall, we hit a new all time high of 20.3%. Over a fifth of all traded risk was in an RFR product last month. That is a huge step forwards and double where we were as recently as March this year – just six months ago.

Highlights include:

- A new all-time high of 20.3% for the overall RFR Adoption Indicator.

- SOFR adoption increased to 15.2% suggesting there is still room for growth under the “SOFR First” initiative. (Read on to see how this relates to our blog headline!).

- 64.8% of GBP risk was versus SONIA (a new high)

- 54.2% of JPY risk was versus TONA (wow!)

- 43.4% of CHF risk was versus SARON.

- $6.0bn of RFR DV01 was traded, 52% higher than last month and a record by over $2bn DV01!

An All Time Record Month

With plenty of records to talk about, let’s see what the really big movers were last month.

First up is the USD market. What happened in SOFR trading last month? Some notables:

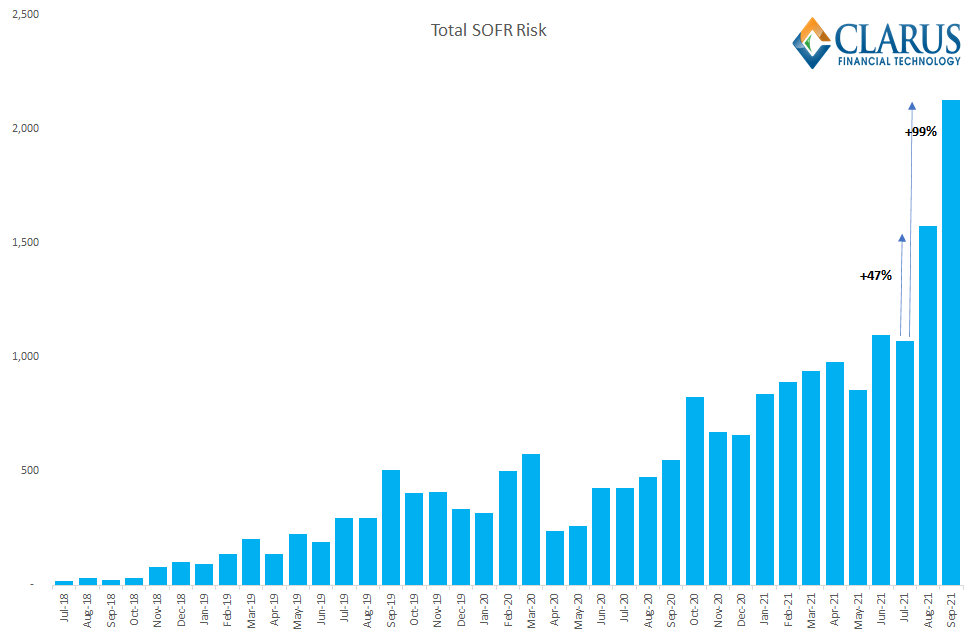

- $2.13bn of USD SOFR DV01 traded across ETD and OTC products in September. This is the first time over $2bn of DV01 has traded in a given month.

- This is DOUBLE the amount of SOFR that traded during July!

- $500m + of additional SOFR risk has been traded each month since July. That is incredible growth:

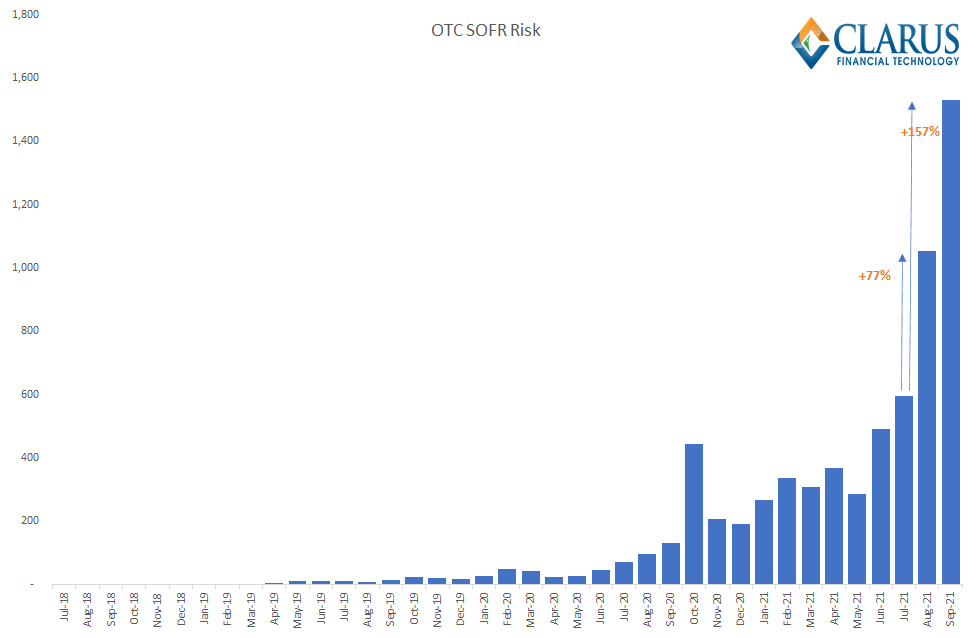

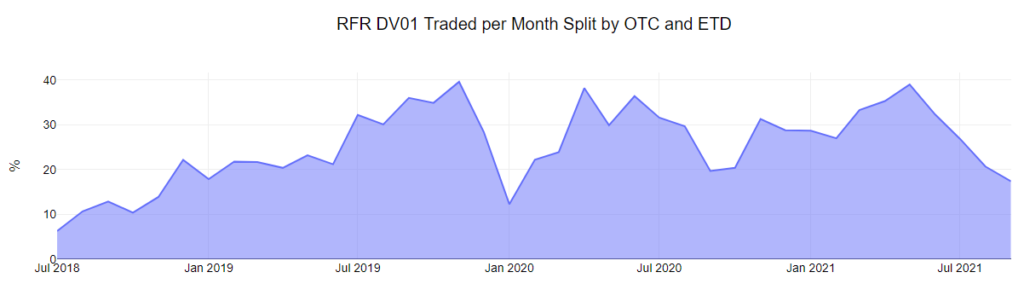

This is across both ETD and OTC. The growth in SOFR risk in OTC markets is even more impressive:

- $1.5bn DV01 of SOFR risk traded in OTC markets last month. This is as much SOFR risk as traded in total just last month.

- It was 2.6 times more risk than traded in SOFR ETDs (futures).

- As recently as May twice as much SOFR risk traded in Futures than Swaps.

- SOFR First has really moved the needle for the amount of risk trading in OTC markets.

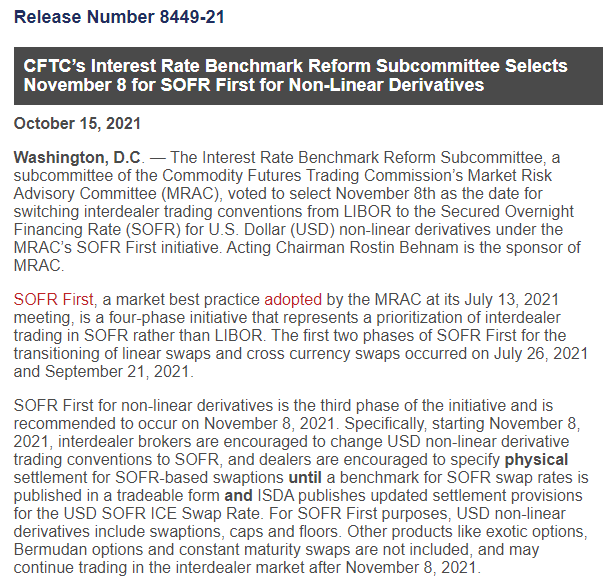

There is probably more to come in OTC space in the coming six weeks as well. November 8th 2021 has now been announced as the “SOFR First” date for non-linear derivatives from the MRAC, a subcommittee of the CFTC:

Sadly, this means we are unlikely to see the impact of this initiative in the data until early December – which is very close to the final date most US banks (and UK etc) are meant to be trading USD LIBOR in the interbank market at all.

Note that there is also planned a SOFR First date for “exchange traded derivatives”:

The fourth and last phase of SOFR First will involve exchange-traded derivatives with timing to be determined.

https://www.cftc.gov/PressRoom/PressReleases/8449-21

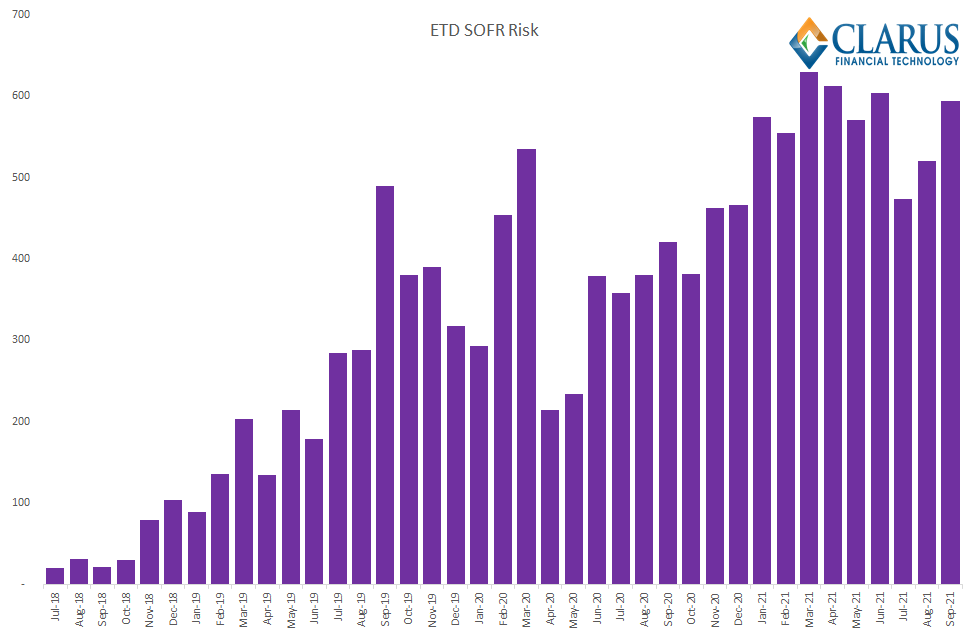

As the chart below shows, SOFR adoption has not significantly changed in ETDs during 2021 at all, so it is high time we saw this market moving:

This lack of activity in ETDs for SOFR shows up across the overall RFR Adoption Indicator where a recent low of just 17% of total RFR risk was actually conducted in ETDs:

Futures markets need to step up their efforts.

Interdealer Data – now for the 78% SOFR data point!

This paragraph in a recent IFR article sparked my interest – it is not the first time I have heard this mentioned:

Brokers estimate 90% of interdealer volumes are now SOFR-linked, while Sokol said a decent cohort of his clients (mainly hedge funds) have also embraced the risk-free rate. Improved liquidity in SOFR swaps has been a pivotal factor.

Clock ticks down on Libor transition

It’s interesting to compare this anecdote from brokers with what our SEFView data shows. Looking at just interdealer SEFs:

Showing;

- DV01 traded at the 5 large interdealer SEF venues in vanilla USD IRS and OIS split by RFR or IBOR indices.

- 78% of risk was traded versus SOFR in October 2021.

- A bit short of the ~90% anecdotal evidence, but yes we do see some days when upwards of 90% of risk is traded versus SOFR.

- Impressive stuff from the interdealer market in reaction to SOFR first.

- Note that over 98% of risk was still being traded versus LIBOR as recently as June!

That puts a bit of perspective on how quickly this shift has happened. We can only assume the same will happen in futures markets (I guess ahead of the December IMM roll date?).

There Are Other Currencies Too!

Enough about SOFR (although it does seem to get the lion’s share of media attention!). JPY markets saw over half of IRD risk traded vs TONA for the first time ever:

This has been a result of a very short-notice “TONA First” initiative by the Bank of Japan. Announced on 26th July and effective 30th July (!) we completely missed this announcement at Clarus – clearly indicative that I should never go on vacation again until RFRs rule the world.

Elsewhere, CHF SARON risk dropped back from the heady 50% heights to 43% of markets – still very impressive. This was also in response to Working Group guidance:

(viii) In order to promote a smooth transition to SARON in CHF derivative markets, the NWG recommended start dates for using only SARON as single price reference and benchmark in derivative markets:

a. The NWG recommended that all market participants (investors and issuers) switch to the SARON swap curve as the only pricing reference starting 1 September 2021, at the latest.

b. The NWG recommended using only SARON-based derivatives for new transactions starting from 1 July 2021, excluding transactions that reduce or hedge LIBOR exposures.

c. The NWG supported both dates, which are currently being discussed internationally – 7 and 21 September 2021 – as start dates to switch quoting conventions of cross-currency swaps in all five LIBOR currencies to RFR (i.e.SOFR, SONIA, TONA, €STER and SARON).

Executive summary of the 1 July 2021 meeting of the National Working Group on Swiss Franc Reference Rates

This was also announced in the final week of July when I was out of the office. Typical!

And of course we should always mention the “poster child” of RFR markets – GBP. SONIA accounted for nearly 65% of all trading, a new all time high in September:

That just leaves us to note that last month saw just 2.3% of EUR risk traded versus €STR. This is before the CCP conversion of EONIA into €STR that took place this last weekend. Strangely, I’ve heard nothing about this potentially major event so I assume everything went smoothly?

In Summary

- RFR transition is plainly evident in the data.

- 20.3% of all global IRD risk was transacted versus an RFR in September 2021, a new all time high.

- Over $2bn of DV01 was transacted in USD SOFR for the first time.

- 78% of USD risk is transacted versus SOFR in interdealer OTC markets according to SEFView data.

- Both GBP and JPY saw over 50% of risk transacted versus an RFR last month.

Hi Chris, crisp and clear as always. One question. The second phase of SOFR first was to deal with cross currency swaps. I’ve seen some things on basis swaps between developed currencies, but nothing on where the buy side convention is supposed to be for trades such as fixed TRY against floating USD, which we see as still against USD Libor. Similar remarks for non deliverable swaps such as fixed IDR against floating USD. Do you see any movement there?

I believe that the market expectation is that everything will transition to include a USD SOFR leg on new trades before the end of the year – at least for interdealer markets. Clients/end-users of course have a degree more flexibility!