- SOFR Swaps are the standard trade for dealer-to-dealer USD Swaps

- Trading as Spreadovers, Outrights, Curves and Butterflys

- Market share is best measured using a package adjusted DV01

- New information allows us to get closer to this metric

- We do this for last weeks volume (23-27 January 2023)

- Showing the following market share

- SOFR Spreadovers, TP-ICAP (IGDL, ISWV, TPSE) is 50%

- Butterflys, Tradition (TSEF) has 55%

- Curves, Tradition (TSEF) 43%

- Outrights, IGDL 62%

- Caveats apply (see below)

- For all SOFR Swaps, it is a tight call between ICAP and TSEF, followed by BGC

- For the data and methodology, continue reading

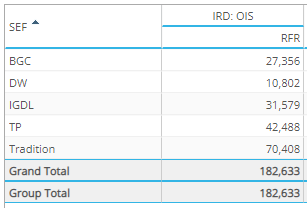

SOFR Swap Volumes at D2D SEFs

Volumes in SEFView reported by D2D SEFs under CFTC Part 16 regulations for last week.

Showing that Tradition is the largest with $70 billion, followed by TP at $42 billion and IGDL(ICAP) at $32 billion. However we know that in terms of market share that represents revenue share, these figures need adjusting for an apples to apples comparison, by at least two factors:

- Notional to DV01, a proper risk-adjusted and comparable measure, as notionals of short dated trades are much higher than long-dated and aggregating these will overstate short-dated volume over long-dated. SEF Fees are charged as a function of DV01.

- Packages, the notionals above are a sum of all legs of a package (a Curve trade has 2 legs, a Butterfly has 3 legs) and so overstate the value of these relative to Outrights (1 leg). SEF Fees are charged on a package adjusted DV01.

In SEFView, as we have tenor information, we are able to do the first, but not the second, as volume is reported by SEFs at an aggregated transaction leg level (so sum of all 5Y volume, irrespective of whether it is from Outrights, Curves, Flys or Spreadovers).

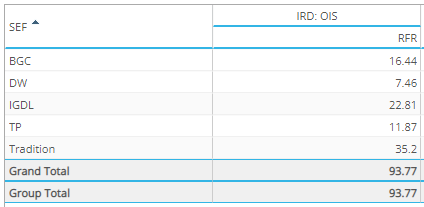

Lets’s change our earlier table to DV01.

A quick inspection of these numbers, shows that in relative terms to the notional table, TP is down and IGDL(ICAP) is up. This makes sense, as we know a higher portion of TP volume is shorter tenors and a higher portion of IGDLs is longer tenors.

Quantifying this as percantage share for:

- Notional – Tradition 38.6%, TP 23.3%, IGDL 17.3%, BGC 15%, Dealerweb 5.9%

- DV01 – Tradition 37.5%, IGDL 24.3%, BGC 17.5%, TP 12.7%, DW 8%

However this is still not the correct share, as packages reported as outright legs (point 2 above) overstates and under-states certain shares. For example, we know that Tradition has a high portion of Butterflys in its volumes, so this volume is counted 3 times (one for each leg) as opposed to a single leg (the middle, by convention).

How can we adjust for this?

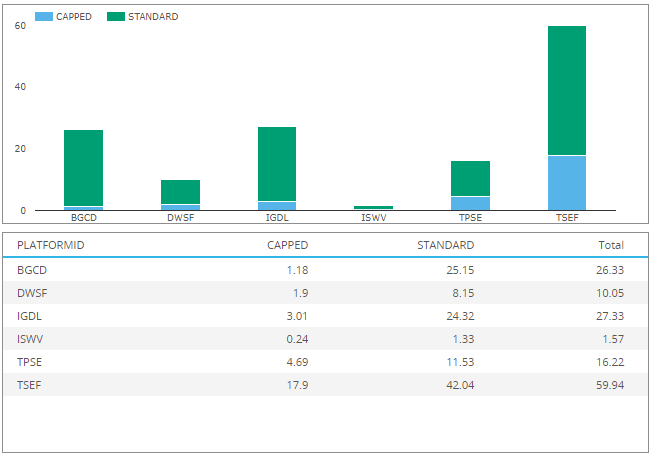

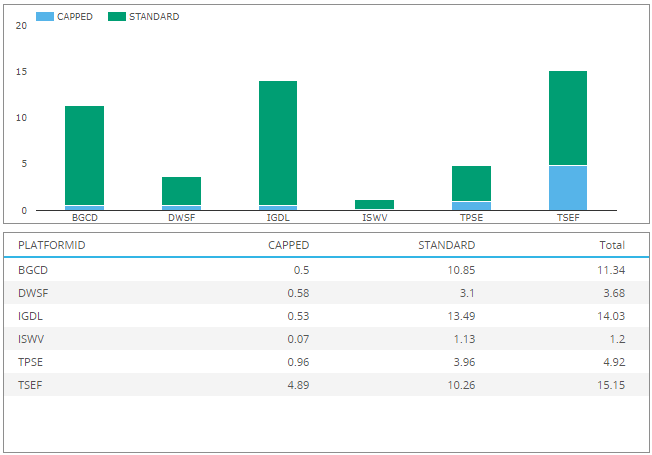

Swap Data Repository Volumes

Luckily, or actually by design, CFTC Part 43 regulations have recently changed to include both package and execution venue (platform_id) information for each transaction reported. So we can create the same notional table from SDRView using trade level data.

The first point to note is that the Total column shows a lower figure for each SEF, compared to what we had in the first table from SEFView. For instance TSEF, which is Tradition, shows $59.96 billion above, lets call it $60 billion, while in the SEFView table we had $70.4 billion, a difference of $10 billion.

This difference is due to capped notional rules, which result in an understatement of the notional shown in the Capped column above. The $17.9 billion reported for TSEF, would have been higher by $10 billion without the capping of notional amounts of large trades.

(Also, as a side note for TPSE, we have excluded $4.5 billion of capped notional volume on 26-Jan-2023, on the assumption that this is non-pricing forming and from Matchbook their portfolio rate reset management service).

Let’s now apply a package adjustment to the above figures, so use a single notional amount for each package (from one of the legs of the Curve or Fly and not the sum of all).

Note the decrease for each SEF, with a greater proportional decrease for TSEF (Tradition), IGDL (ICAP) and DWSF (Dealerweb).

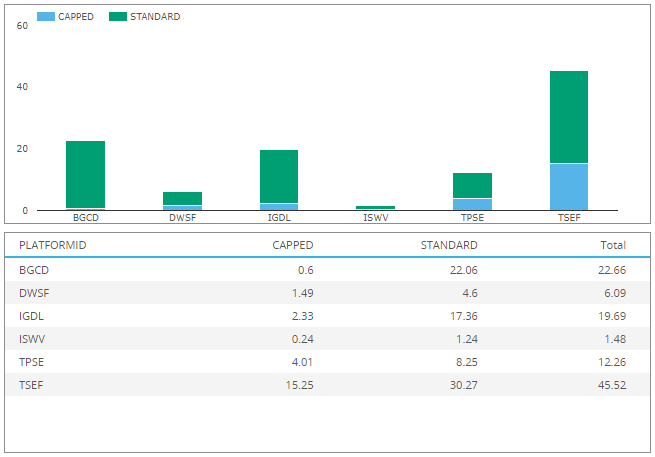

Now let’s do the above but for DV01.

Showing a more equalisation of volume between TSEF, IGDL and BGCD.

Quantifying this as a market share percentage, we now have:

- Tradition 30.1%, IGDL (ICAP) 27.9%, BGC 22.5%, TP 9.8%, DW 7.3%, ISWV (ICAP) 1.2%

Compare that to what SEFView gave us (without package adjustment):

- Tradition 37.5%, IGDL 24.3%, BGC 17.5%, TP 12.7%, DW 8%

We plan to refine our methdology to get to a better number.

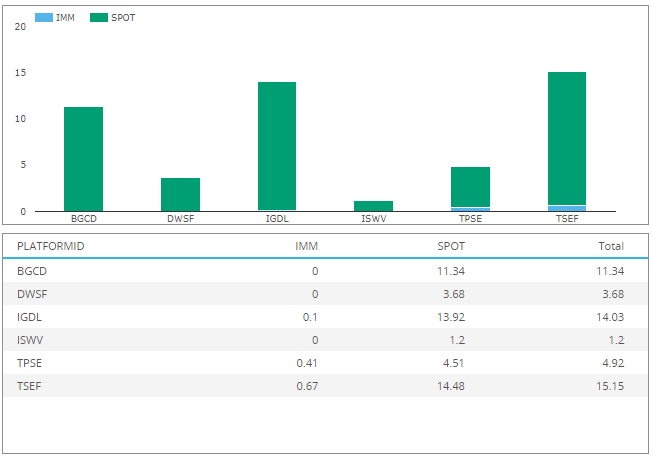

IMM Swaps

We can also look at the above DV01, by separating out IMM Swap volume from standard Spot starting Swaps.

I don’t know if the IMM volume above is Invoice Spreads (IMM Swaps vs CME SOFR Futures), one to investigate on another day.

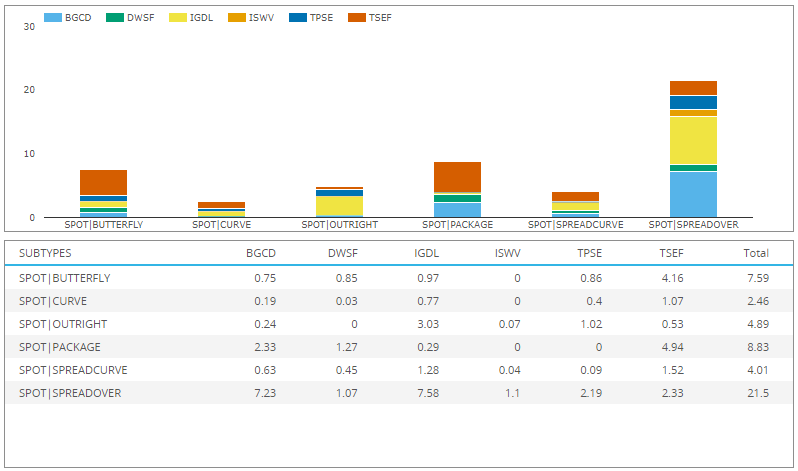

Market Share by Package

Let’s now look at market share by package type; Outright, Spreadover, Curve, Butterfly.

First in DV01 amounts.

Showing that Spreadover is by far the largest package type with $21.5 million DV01 and SpreadoverCurves are a further $4 million.

Butterfly is the next largest with $7.6 million DV01.

(Recall both of these are somewhat under-stated due to capped notional rules, not by a huge amount, at an estimate somewhere in the 10-25% range).

There is also a Package row, which is a bucket for transactions reported as part of a package, that we have not been able to classify into one of the other types or requires a new granular type. At $8.8 million DV01 this is much larger than expected, particularily for TSEF, BGC and DWSF. So that is a pending task. What is it with data, always something more to analyse, classify and make sense of!

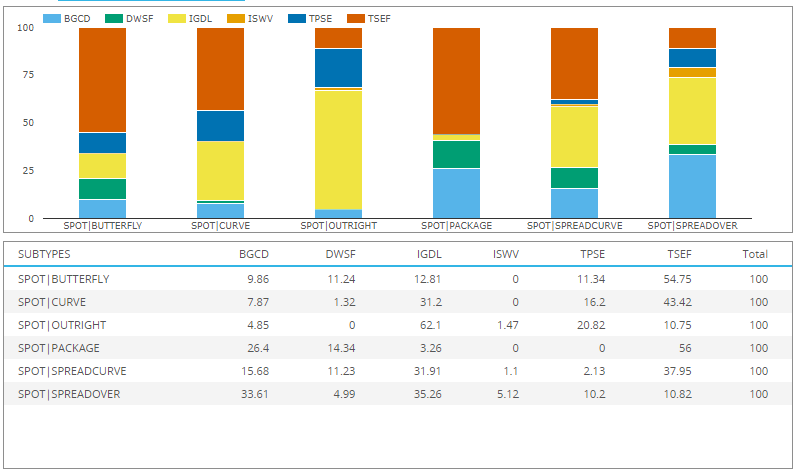

Next the same data as a percentage share of DV01.

Showing that in:

- Spreadovers, IGDL has 35% share, followed by BGC with 34%

- Adding in ISWV to IGDL (as both ICAP), increases ICAP to 40%

- While adding in TPSE to ICAP, we get TP-ICAP at 50%

- Spreadover Curve share is shown separtely above

- Butterfly, Tradition has 55% share

- Curves, Tradition has 43% share

- Outrights, IGDL has 62% share

- Package, we need to re-classify TSEF, BGC, DWSF

Aggregating all these to get a share for all spot starting SOFR Swaps, we get:

- TSEF 29.5%, IGDL 29.3%, BGC 23%, TPSE 9.25%, DWSF 7.5%, ISWV 2.5%

Again caveats apply due to capped notional rules and the package bucket, both of which will result in some change to these.

While these figures are only for last week, they represent our best estimate of market share.

One we plan to improve in the weeks ahead.

That’s all for today.