This blog follows on from the interesting activity we have seen across Options markets so far this year. Take a look if you have missed anything:

I have written previous Swaption reviews after large, directional moves in Rates. Q2 2024 was a little bit different, although it would still be characterised as a “volatile” quarter. Q2 2024 saw the following daily moves in ten year SOFR swaps:

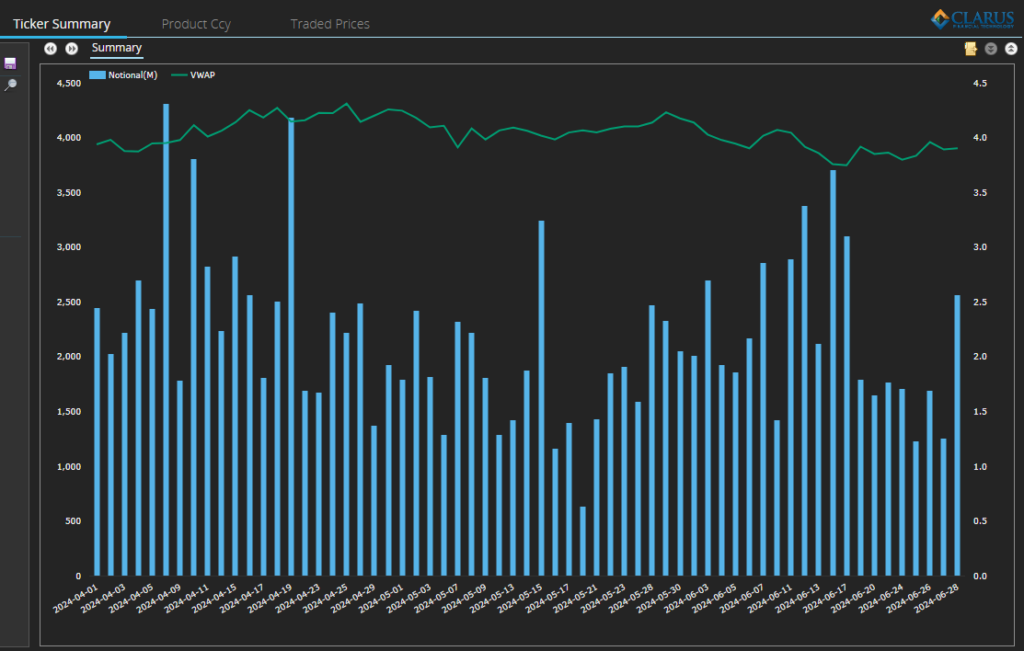

Showing;

- The daily Volume Weighted Average Price (VWAP) for 10Y USD SOFR Swaps (ticker USOSFR10).

- There was a 56 basis point range in VWAP, from 3.75% to 4.31% for 10Y SOFR swaps.

- The volumes are interesting. Starting on the left of the chart, we had a peak in volumes early in April when yields were at their lowest since end of Feb.

- This was almost immediately followed by a sharp sell-off (move higher in Rates) on April 10th, which resulted in the second highest volume day of the quarter.

- We then had to wait until the end of the quarter to see another spike in volumes. The middle of June (12th-14th) saw bonds rally, yields moving lower and swap volumes again spiking beyond $3.5bn in a day.

- This evolution of Rates means that we are not necessarily expecting to see lots of swaption activity at either the highs or the lows of the month. But let’s check the Heatmaps.

Notes on the Data

Straddles are now included in the packages that Clarus identify. They are no longer identified in the source data – see this blog for details about how the data changed. I recently found out that over 80% of D2D trades are Straddles, which is nicely backed up by SDR data:

Which is great. What is not so great is that, in the source data from the DTCC, Payers are no longer called Payers and Receivers are no longer called Receivers. All Options are “standardised” so that the data is streamlined into Puts and Calls for all product types. Great on the surface, but we are not 100% convinced that everyone is now reporting these accurately. There are far more D2D payers transacted with a “2” handle on the strike for 10Y tails and D2D receivers transacted with “5” handles for the data to be consistent.

The convention that we follow is:

- Call = Payer (it is a call on the underlying swap).

- Put = Receiver (it is a put on the underlying swap).

This is consistent with the UPI specs, the ISO 20022 standards and RTS23 in MIFIR – so we are pretty sure it is accurate. Could we ask all SEFs, dealers and other reporting entities to ensure that they are following the same standards please?

Within the scope of MiFIR, RTS 23, the following meanings should be used where a swaption is being detailed, “Put”, in case of receiver swaption, in which the buyer has the right to enter into a swap as a fixed-rate receiver. Call”, in case of payer swaption, in which the buyer has the right to enter into a swap as a fixed-rate payer. Caps and floors shall interpret this field as, “Put”, in case of a Floor, “Call”, in case of a Cap. Field only applies to derivatives that are options or warrants.”

ISO 20022, Derivative Instrument5

Swaptions Activity

The Year-on-Year comparison highlights the variability we see in Swaption volumes:

Showing;

- 20,150 swaptions executed in Q2-2024, 3% lower than Q2-2023.

- April saw 30% more swaptions executed than the previous year.

- May saw 5% less swaptions…

- …and June saw 25% fewer swaptions executed than last year.

Swaptions Activity by Strike

SDR data for all USD Swaptions reported in Q2 2024 (including packages) can be used to create the following heatmap of Swaption activity:

The summary of Q2 2024 USD swaptions activity shows;

- The notional volume (in $ millions) of USD swaptions traded in major tenors in 25 basis point strike increments.

- This covers all expiries. A 3m10y is grouped together with a 1y10y if they were traded at the same strike.

- This covers Payers & Receivers , Straddles and all other Packages.

- It looks at new volumes traded in the quarter. This is not the same as Open Interest (such as the CME Heat Maps) but it nevertheless gives an idea of activity.

- Red areas show the “hottest” strikes and tenors, those with the most notional volume traded.

- We saw strikes all the way up to 6.75% trade in the quarter (for 10Y underlyings), with activity not really dropping off until ~5.75% strikes for most of the underlyings.

- The highest strike with more than $1bn traded in a particular tenor saw $1.86bn of activity at a 6.5% strike versus 1Y (the underlyings are also referred to as “tails” FYI).

- The red areas largely reflect where the at-the-money rates were as vol trading is naturally concentrated around these areas. The red areas nicely highlight the inversion of the curve as they occur at lower strikes in longer tenors.

- The most active tenor was 1Y, with a huge $539bn traded across all strikes in Q2 2024.

- There is then quite a gap to activity in 10Y underlyings, with $334bn traded. This is consistent with our previous analyses where 1Y and 10Y tenors tend to see the largest notional amounts trading.

- There was an exceptional amount of activity in 10Y tails at strikes of 4% and 4.25%, with over $213bn trading.

Receivers Activity

Now looking at activity only in Receivers:

- Total activity in Receivers accounted for 37% of overall Swaption activity (measured by notional) – higher than the 33% we saw in 2022.

- The most active underlying was 1Y, which again saw a range of strikes traded. $10bn or more traded in strikes from 3.75% all the way up to 5.25%.

- Activity in 20Y underlyings continues to be skewed toward Receivers – why? Of all activity versus a 20Y tail, 49% was in Receivers (versus just 21.4% in Payers). This has been the case in every Swaptions blog I have written. There must be a structural imbalance in the market. Anyone care to comment? Activity was concentrated in the at-the-money strikes from 4-4.25%.

Payers

And for Payers only;

- Payers accounted for 36% of total Swaptions activity as measured by notional.

- The most active underlying and strike was 1Y 5.25%, with over $40bn traded – the most active of any 25 basis point increment across Payers and Receivers.

- 3Y underlyings were relatively more active in Payers this quarter, with 51% of all activity in Payers. The most active strike was 4.75% with nearly $6.5bn traded.

Straddles

And, for the first time since 2022, I can reintroduce the Straddles Heatmap:

- Due to the product, the range of strikes is naturally more compressed for Straddles. A Straddle is a combination of a Receiver Swaption and Payer Swaption with the same expiry, same underlying and same strike. Therefore, if Rates do not really move, both Payer and Receiver positions will expire worthless, and the premium paid (or received) will constitute a loss (or gain).

- Straddles accounted for 28% of total swaption notional traded, somewhat higher than previous analyses in 2021 and 2022. Activity in Straddles is heavily skewed toward the D2D market.

- The most traded Straddles were 10Y underlyings at 4% and 4.25% strikes. These were the most active of any instrument that we saw traded, accounting for over $40bn of activity each (these are “package adjusted” notionals, so only one leg of the Straddle notional is counted).

- Unusually, there was more activity in Straddles versus 5Y tails, than there was in outright 5Y Payers.

In Summary

- Analysis of swaptions activity is a regular feature on the blog across Payers, Receivers and Straddles, allowing us to monitor quarterly trends.

- Heatmaps of option activity show the most active underlyings (tails) and strikes.

- There has been a demand imbalance for Receivers versus 20Y tails for at least 2 years, suggesting this is a structural facet of the market.

- Payers saw relatively more activity in 3Y tails, whilst Straddles saw more activity in 5Y tails than outright Payers.

- There was a huge amount of activity in Straddles versus 10Y underlyings at 4% and 4.25% strikes.