- RFR trading in Q2 looked a lot like Q1, with some changes in USD and EUR.

- 60-80-30 are the three numbers you need to know for RFR Trading now.

- 60% is the percentage of global trading that takes place against RFRs.

- 80% is the amount of the USD market that trades versus SOFR.

- 30% is the amount of the EUR market that trades versus €STR.

Time for a quarterly check-in on RFR trading. The data provides a high-level overview of trading activity across all Rates products.

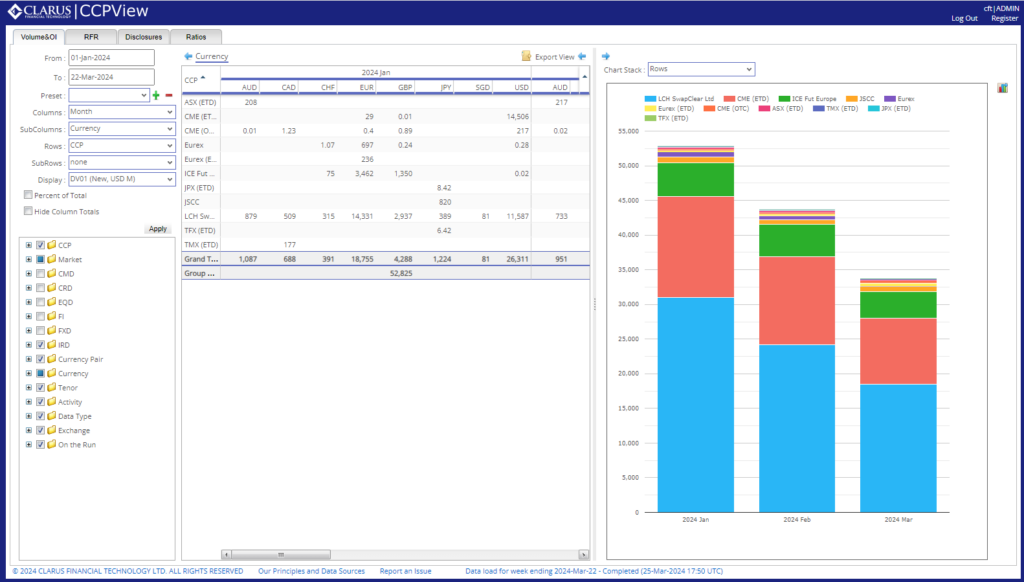

Clarus API – CCPView

As a reminder from the previous blog, Clarus microservices allow me to query numerous volume measures from CCPView. That means I have rebuilt the RFR Adoption Indicator using just two queries to pull in DV01s traded across all products in eight currencies:

RFR Adoption Q2 2024

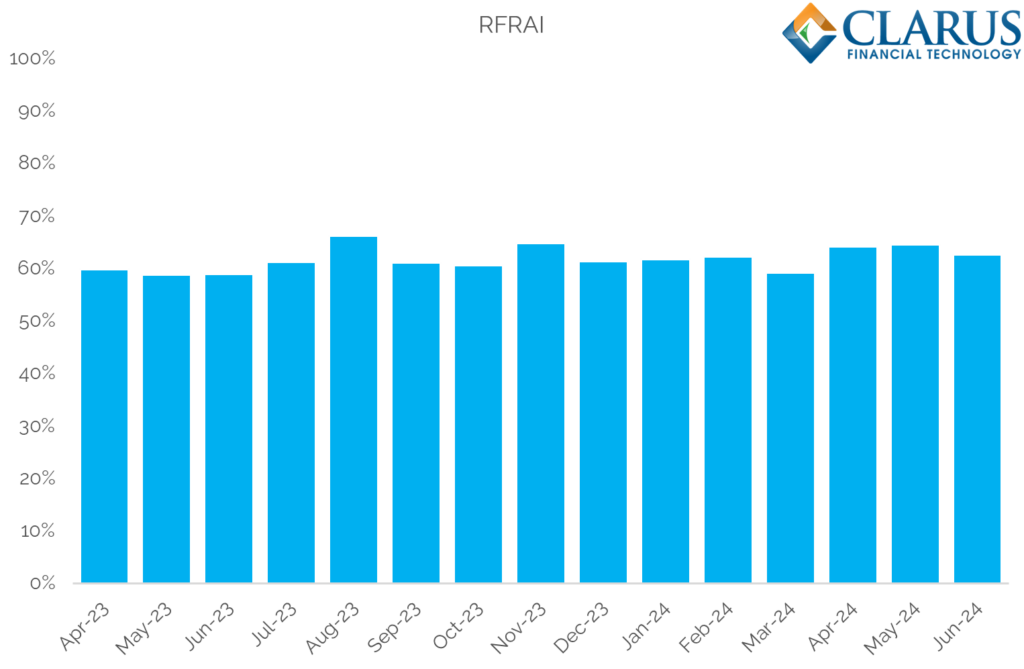

Stability. That is the key word for the past year when you look at the evolution of RFR trading as a percentage of all risk traded:

Showing;

- As of June 2024, the RFR Adoption Indicator stands at 63% vs 59% in June 2023.

- It has been between 59% and 66% since Q2 2023.

- There is no particular pattern to the monthly variations.

- It has been particularly static during Q2 2024, at 63-64%.

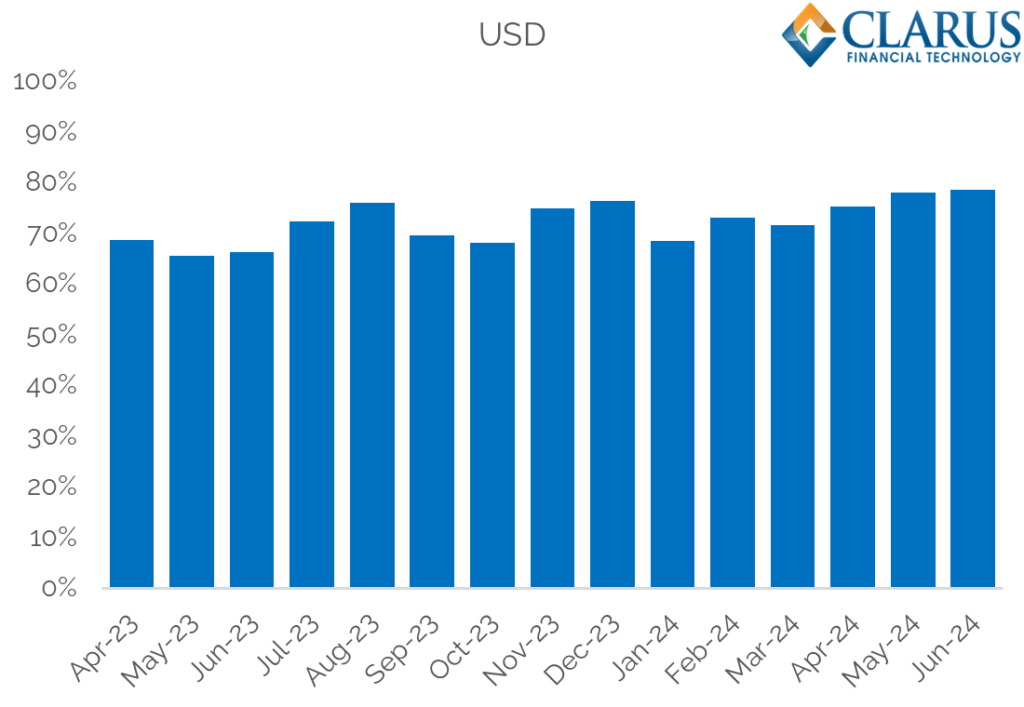

RFR Trading in USD

Starting with USD:

- June 2024 saw 79% of all USD risk traded versus SOFR versus 59% in June 2023.

- This is a new all time high.

- Q2 2024 ranged from 75% – 79%, compared to 66-69% in Q2 2023.

- More SOFR trading in USD means that there has been less Fed Funds traded.

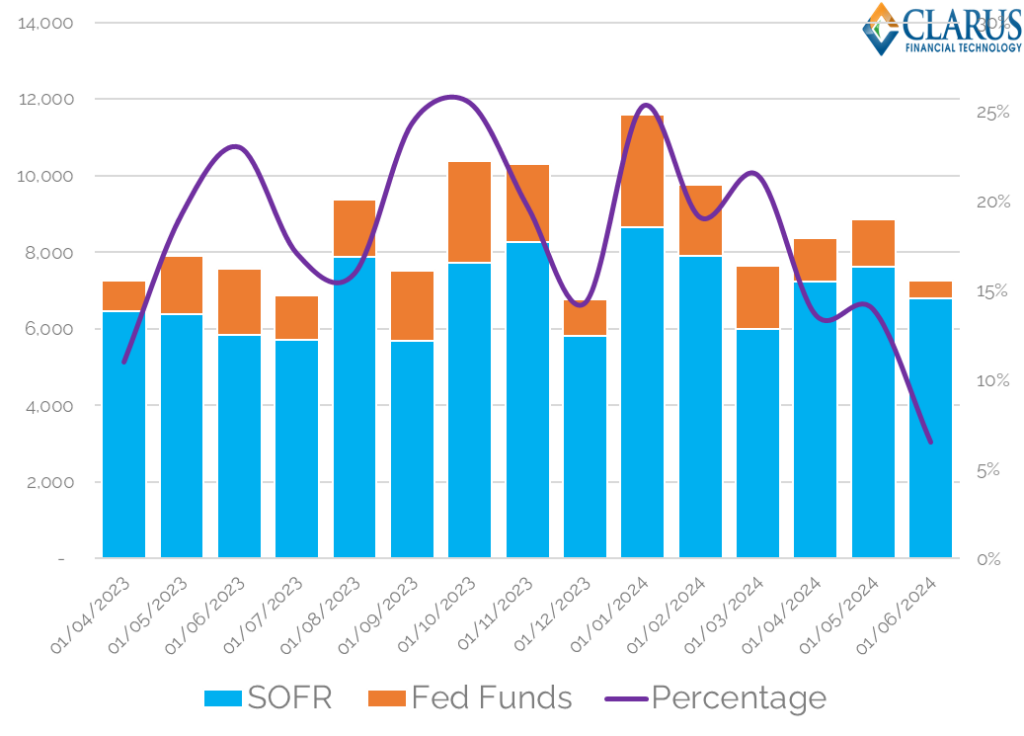

- These numbers include both Swaps and Futures. If we look at only Swaps, just 7% of risk was traded versus Fed Funds in June 2024, compared to 23% in June 2023:

RFR Trading in EUR

To state the blindingly obvious, EUR markets continue to trade across multiple rates/indices. There is a fight for market share in EUR €STR futures, and in CCP market share as a result of “active accounts“, whilst the overall split of EURIBOR and €STR is volatile:

- June 2024 saw 27% of all EUR risk traded versus €STR. It was 29% in June 2023.

- Q2 2024 ranged from 27% – 35%, compared to 27-29% in Q2 2023.

I get confused as to which is the larger market – EUR or USD. It is therefore useful to state that:

- There is a larger total DV01 traded across all USD risk (Swaps and Futures) than in EUR.

- Swaps markets in EUR are now consistently larger than in USD, as a result of USD LIBOR cessation.

- Futures markets in USD rates are much larger than in EUR – like 4 times as big:

- USD is therefore still the largest component of the overall RFR Adoption Indicator (because it looks at total risk).

- Our data subscribers can cut this data any which way they choose using simple API queries.

RFR Trading in CAD

Showing;

- CAD CDOR publication ended on 28th June 2024.

- CORRA adoption reached 97% in June 2024, a new all time high.

- It was 60% in June 2023 and should now move up to 100% the next time I take a look at the data.

RFR Trading in AUD

- AUD is the other currency pursuing a multiple rate/index future. Check out the blogs here and here plus the podcast on AUD swaps for my thoughts on that!

- AONIA trading accounted for 37% of total AUD rates risk traded in June 2024, compared to 45% a year earlier.

- Q2 2024 ranged from 37% – 40%, compared to 42-45% in Q2 2023.

In Summary

- 60% of global rates trading occurs versus Risk Free Rates.

- This has been pretty consistent during 2024.

- In Q2 2024, it was most volatile in EUR, ranging from 27-35%.

- SOFR trading has been ticking higher in USD markets, now reaching nearly 80% – a new all time high.

- CAD should now move to 100% of trading versus CORRA following CDOR cessation.