Last week CME Group announced that it will begin clearing Swaptions on April 11, 2016 and this triggered my interest in revisiting trading volumes and taking a deeper dive into margin requirements for Swaptions.

Volumes in SDRs

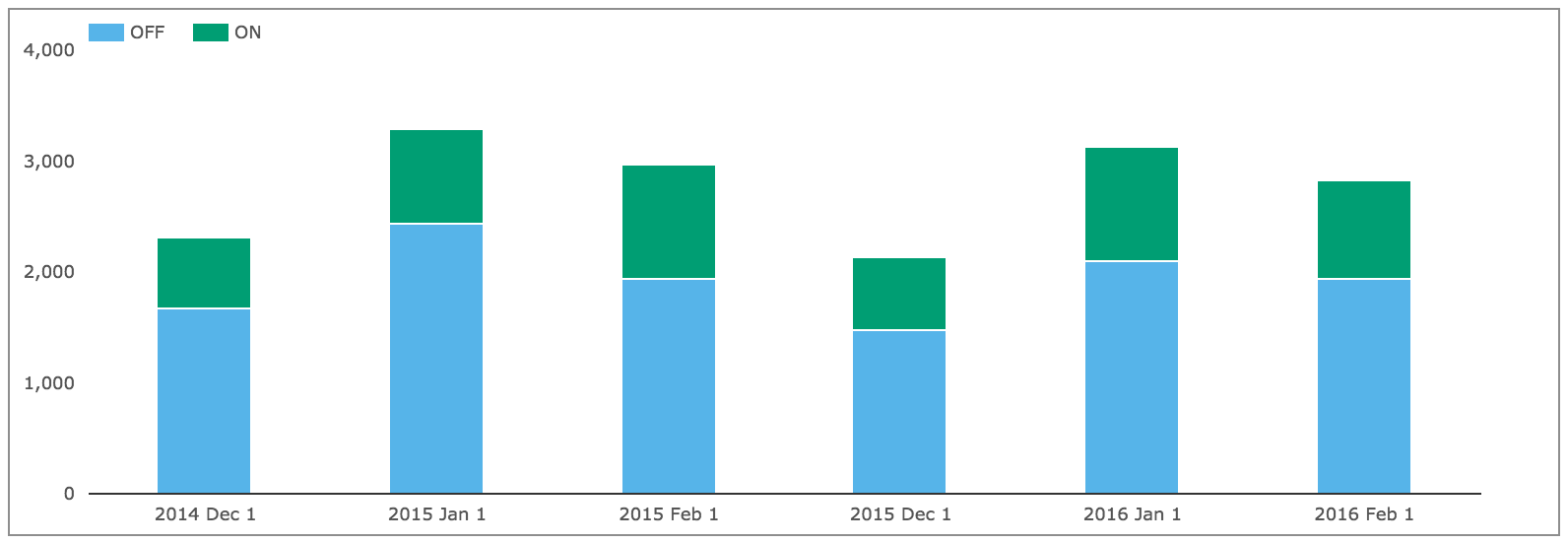

I last covered Swaption volumes in Jan 2015, so lets use SDRView to look at volumes for US persons:

Showing:

- USD Swaptions in the most recent 3 months compared to a year earlier

- Monthly trade counts split by Off SEF and On SEF

- Approximately 3,000 trades a month are reported

- Of which 2,000 are Off SEF and 1,000 On SEF

- Volumes are broadly similar year-on-year

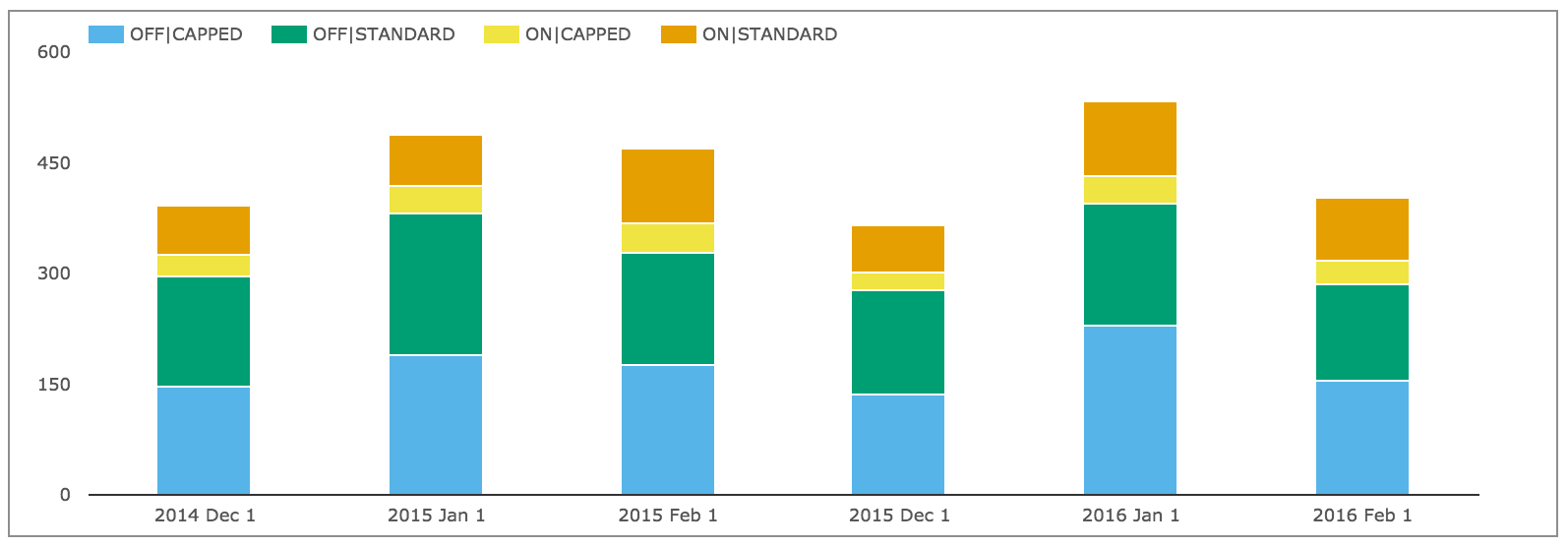

Switching to Gross notional in billions.

Showing:

- Volume split further by Capped (above block/large size) and Standard (below block/size)

- At least $400b to $500b trades each month

- Capped volume for Off SEF is generally higher than Standard volume for Off SEF

- While the opposite is true for On SEF

- Suggesting more large trades take place Off SEF than On SEF

Big numbers indeed.

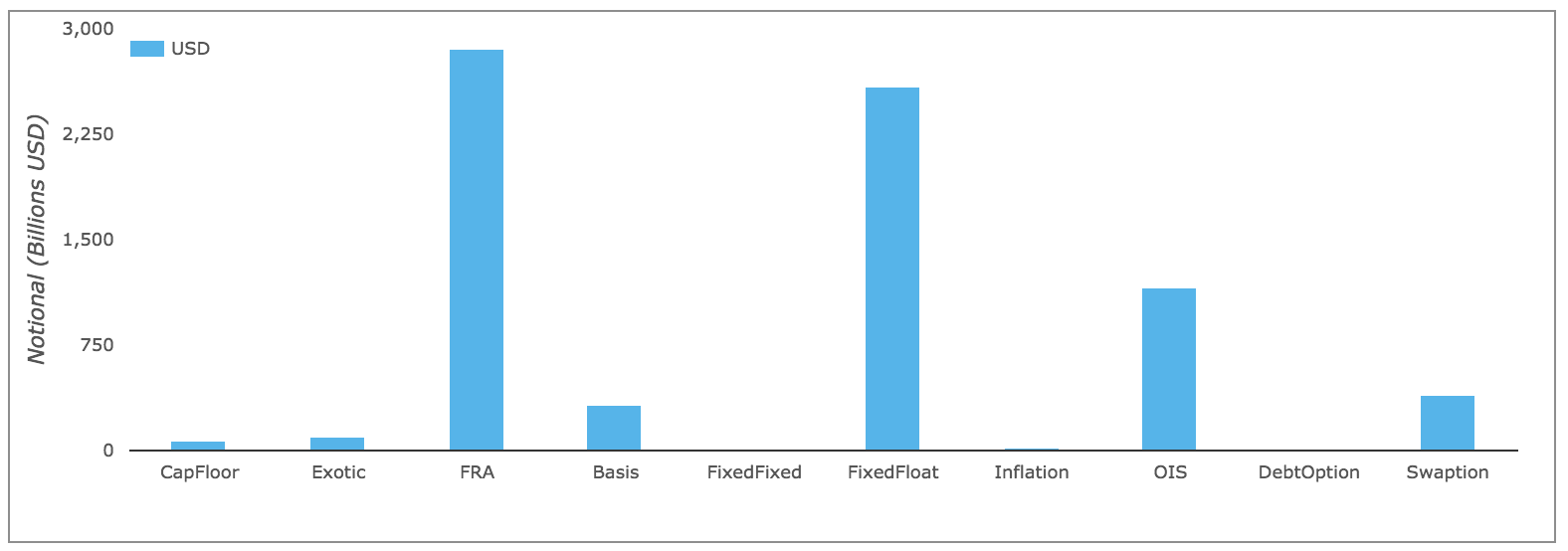

And comparing February 2016 gross notional for all IRD products.

Shows that USD Swaptions are the 4th largest USD IRD product and by far the largest product that is not cleared. Surely Swaptions Clearing is long overdue and even more pressing when Uncleared Swap Margin Rules come into force from Sep 2016.

CME Swaptions Clearing Scope

CME’s initial scope is USD Payers, Receivers and Straddles with Expiry less than 2 Years, underlying Swaps (vanilla and spot starting) up to 30 Years with Libor 3M index and with European exercise and Physical settlement. EUR Swaptions will follow at a later date.

Lets look at what proportion of USD Swaptions this initial scope represents.

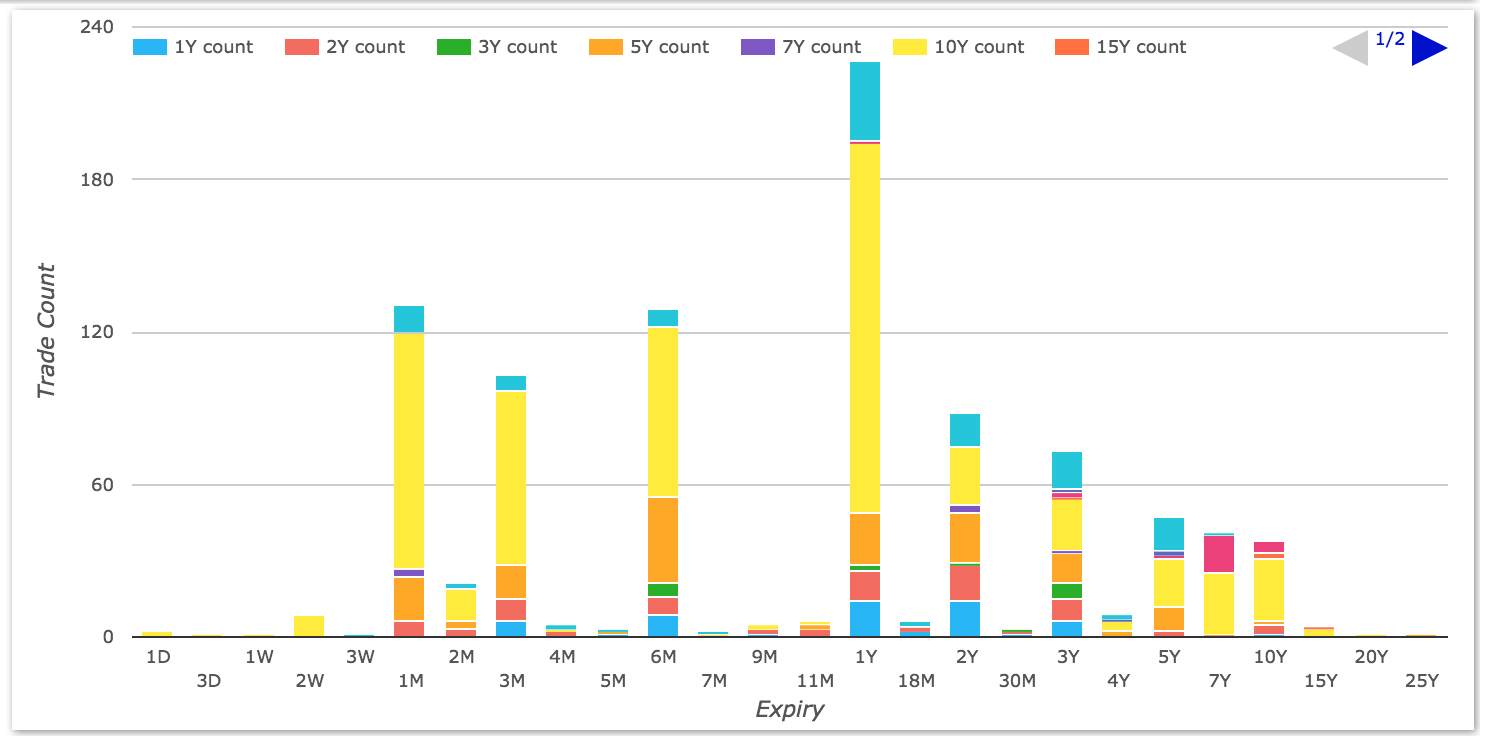

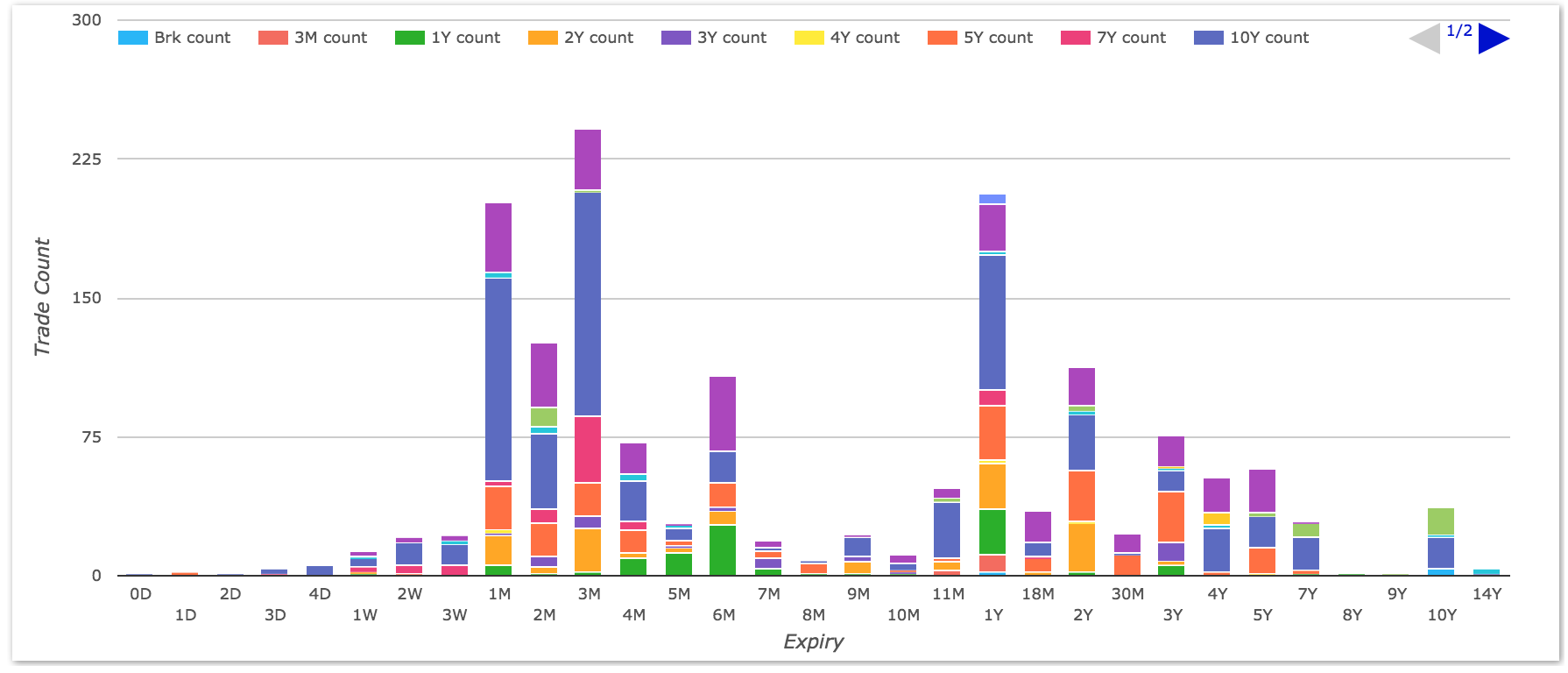

Using SDRView we can select USD Straddles with European exercise on spot start swaps in February 2016.

Which shows:

- 1Y into 10Y are by far the most common with 145 trades

- 1M into 10Y are next with 93 trades

- 3M into 10Y and 6M into 10Y each with 67

- 740 trades are up to 2Y expiry and 30Y Swap

- Out of a total of 957 Straddles

- So 77% of the Straddles volume is in scope

Now lets look at Payers and Receivers in February 2016.

Which shows:

- 3M into 10Y are the most common with 121 trades

- 1M into 10Y are the next most common with 110 trades

- A total of 1,590 trades of which 890 are Payers and 700 Receivers

- 1,303 trades are up to 2Y expiry and 30Y Swap

- So 82% of the Payers & Receivers volume is in scope

In grand total terms, 1,303 + 740 = 2,043 trades are covered by the CME product scope. This represents around 75% of the total volume, with Forward Start representing the largest product characteristic not in scope.

However these is no flag on the SDR public dissemination record that tells us whether the trade is physically settled (into the swap) or cash settled (using ISDAFix or a Curve); which would serve to reduce the proportion in scope. For USD, certainly in the IDB market, cash-settled Swaptions are common, even though given the investigations into ISDAFix moving to physical settlement into the Swap would be attractive.

So our best guess is that up to 75% of USD Swaptions volume is within the initial CME Clearing Scope.

Which is very significant when you consider that this is the first OTC Derivative product with optionality that is going to be cleared by any global CCP.

CME VM methodology for Swaptions

Lets now change focus and look at the specifics of CME’s margin methodology for Swaptions starting with variation margin, which requires a daily settlement price valuation to be performed.

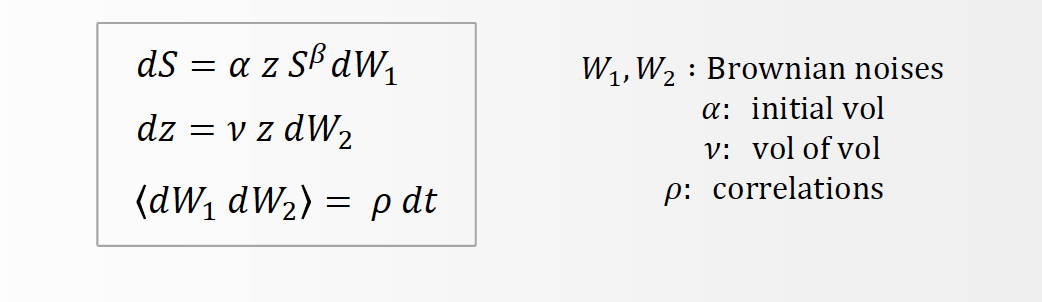

CME have chosen to use a modified SABR model to price Swaptions and such shifted SABR models are the market standard for pricing Swaptions, as they interpolate market quotes and are able to reproduce the observed volatility smile and skew dynamics.

Clearing members submit volatility cubes each day from which CME calibrates its SABR model parameters and then values the portfolio of cleared Swaptions. CME will also publish some daily options pricing data, which should help improve transparency and price discovery for Swaptions.

Portfolio margining of Swaptions and Swaps is supported, so a Swaption that is delta-hedged with a Swap would have much lower daily variation margin moves than a naked Swaption.

CME IM methodology for Swaptions

The initial margin methodology is more of a challenge.

Firstly the Filtered Historical Simulation methodology that CME uses for Swaps has been extended by adding normal atm implied volatilities as risk factors into the scenario set.

Secondly a new Skew AddOn charge is introduced to capture the risk from out-of-the-money or in-the-money positions in a portfolio as well as a higher level of price dispersion in price submission for non-ATM options.

Together these constitute a base initial margin for Swaptions and one that is consistent with the existing Swaps methodology, which will provide capital efficiencies when margining Swaps and Swaptions.

CME Liquidity Margin for Swaptions

A key challenge for Swaptions is default management and specifically how to increase the margin requirement to compensate for a possible increase in time and cost to hedge and auction a defaulted portfolio.

To address this, CME has revised its existing Liquidity Addon methodology, which relied on an IM threshold multiplier, to a methodology based on the liquidity cost for each of the risk sensitivitys (greeks) in a portfolio.

For Swaps only portfolios this is Delta risk and means that firms with large directional portfolios may also see a change to their Initial Margin requirement after April 11; even if they do not have Swaptions in their account.

For portfolios with Swaptions and Swaps, in addition to Delta risk, Gamma, Vega and Skew risks are also considered.

CME uses a Dealer Poll to collect data from which Liquidity Cost functions and Liquidity AddOn tables for Delta, Gamma, Vega and Skew are derived. These then serve to increase the margin requirement to compensate for the time and cost to hedge the additional market risks in a defaulting portfolio that includes Swaptions.

That is it for our quick detailed dive into margin methodologies.

Summary

CME has announced clearing for Swaptions.

Swaptions are a large and important Interest Rate product with significant volume.

A margin methodology that accounts for portfolio margin offsets with Swaps is highly desirable.

It means that Swaptions delta hedged with Swaps will attract far less margin (80% to 90% less).

Removing one of the hurdles to clearing Swaptions.

Upcoming Uncleared Swap Margin rules will create a further impetus to use Clearing.

Given that this will be more expensive (e.g. MPOR of 10d and not 5d).

It will be interesting to see how quickly firms adopt Swaptions Clearing.

Only time and data will tell.