Clearing Houses have published their latest CPMI-IOSCO Quantitative Disclosures:

- Initial margin for ETD at $528 billion is down 7% QoQ and up 19% YoY

- Initial margin for IRS at $280 billion is up 4% QoQ and 8% YoY, to hit a record high

- Initial margin for CDS at $76 billion is up 15% QoQ and 31% YoY

- LME Disclosures that increase in the latest quarter are highlighted

- A number of CCP disclosures show record highs since reporting began in Sep 2015

- Including at B3, CDCC, ECC, Eurex, ICE Clear Credit, LCH SwapClear …

- Continue reading for charts and details

Background

Under the CPMI-IOSCO Public Quantitative Disclosures, CCPs publish over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk, back-testing and more.

CCPView has over 6 years of these quarterly disclosures for 44 Clearing Houses, each with multiple Clearing Services, covering the period from 30 Sep 2015 to 30 Jun 2022. This disclosure data provides insights into trends over time at one CCP and comparisons between CCPs.

Let’s take a look at the latest disclosures.

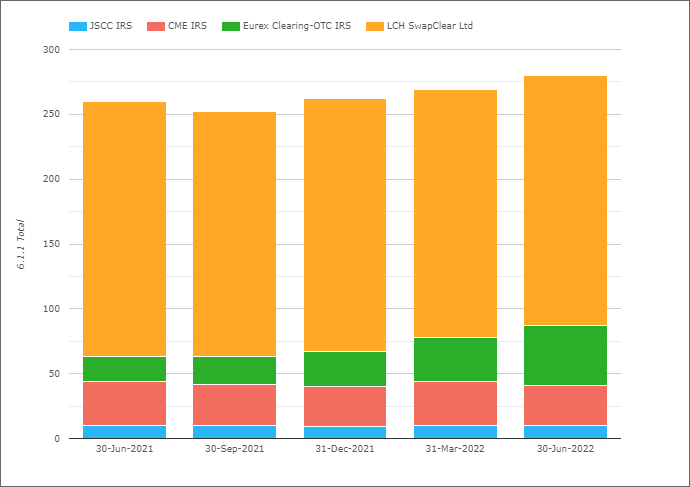

Initial Margin for IRS

- Total IM for these four CCPs was $280 billion on 30-Jun-2022

- $11 billion or 4% higher QoQ and $20 billion or 8% higher YoY

- LCH SwapClear with $193 billion or £159 billion on 30-Jun-2022

- Up 9% QoQ and 12% YoY in GBP terms ( and up 1% and down 2% in USD terms)

- Eurex OTC IRS with $46 billion or €44 billion, is again higher than CME

- Up €13 billion or 42% QoQ and €28 billion or 177% YoY (in EUR terms)

- CME IRS with $31.5 billion, down 6% QoQ and down 7% YoY

- JSCC IRS with $10 billion or Y1,366 billion, up 14% QoQ and up 24% YoY (in JPY terms).

Total IM for IRS at $280 billion, is above the record high of $271 billion on 31-Mar-20.

Eurex OTC IRS increasing significantly QoQ and even more so YoY.

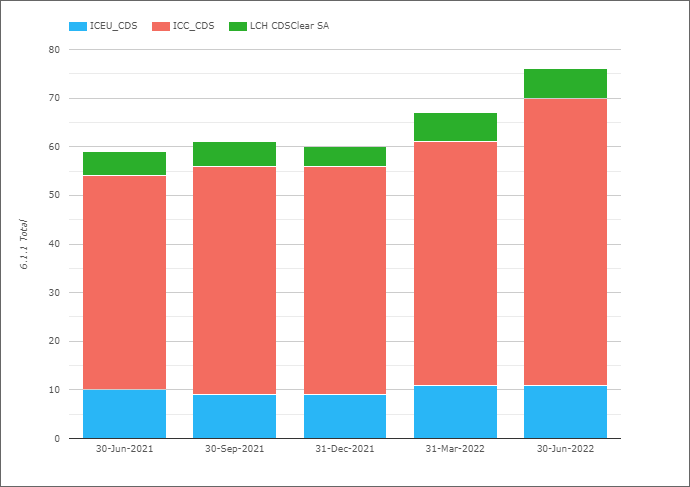

Initial Margin for CDS

- Total IM for these three CCPs was $76 billion on 30-Jun-2022

- Up $10 billion or 15% QoQ and up $18 billion or 31% YoY

- ICE Credit Clear with $58.8 billion, up 18% QoQ and 35% YoY

- ICE Europe Credit with €10.65 billion, up 11% QoQ and 32% YoY

- LCH CDSClear with €5.9 billion, up 15% QoQ and up 47% YoY

IM increasing at each CCP by double digit QoQ percentages and >30% YoY.

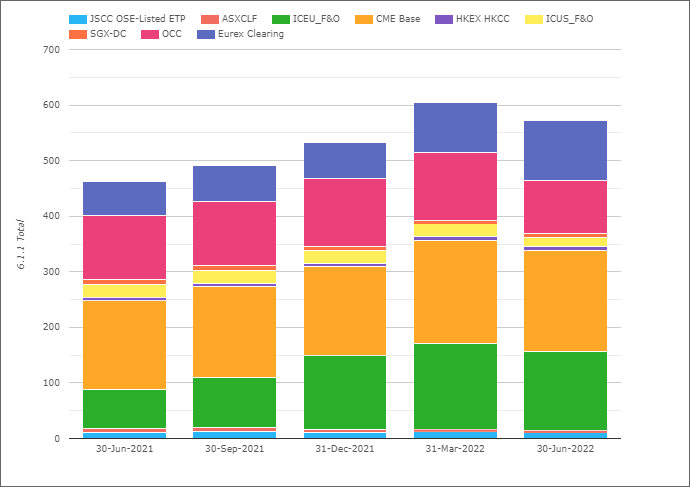

Initial Margin for ETD

- Total IM for these CCPs was $528 billion on 30-Jun-2022

- Down $43b or 7.5% QoQ and up $84b or 19% YoY

- (Note the chart shows higher totals as the Eurex figure includes OTC IRS IM, which I exclude)

- CME Base with $182 billion, down 2% QoQ and up 14% YoY.

- ICE Europe F&O with $141 billion, down 8% QoQ and up 100% YoY!

- OCC with $95 billion, down 22% QoQ and 18% YoY.

- Eurex with $63 billion, up 12% QoQ and 50% YoY.

- ICE US F&O $17 billion, down 20% QoQ and 27% YoY.

- JSCC OSE Listed ETP with $10.5 billion, down 14% QoQ and 4% YoY

- HKEX HKCC with $7.2 billion, down 12% QoQ and up 34% YoY

- SGX-DC $7 billion, up 1% QoQ and down 18% YoY

- ASX CLF $5.1 billion, down 2% QoQ and 22% YoY

ETD IM showing the first decrease since the 30-Sep-2020 quarter end.

- OCC with the largest decrease in amount terms, dropping to $95 billion from $121 billion in the prior quarter, persumbly as equity prices and positions decreased.

- ICE Europe and ICE US down 8% and 20% respectively, persumably as commodity prices decreased a touch and volatility down.

- Eurex the only CCP to buck the QoQ trend, up 12% in USD terms.

LME Disclosures

Last quarter we covered the London Metal Exchange (LME) disclosures in some detail, given the suspension of Nickel trading. Consquently it is worth looking for disccloures that have changed materially between 31-Mar-2022 and 30-Jun-2022:

- 4.1.4 Prefunded – Aggregate participant contributions doubled from $1.1 billion to $2.08 billion

- 4.1.8 Committed – Aggregate participant contributions to address a default also up from $1.1 billion to $2.08 billion

- Neither is surprising given the price volatility in commodity markets and events of early March 2022.

- 5.3.4 Number of days during the look-back period on which the fall in value during the assumed liquidation period exceeded the haircut on an asset increased to 64 from 44, a record high

- 6.1.1. Client Net IM dropped from $8.6 billion to $5.9 billion

- 6.1.1 House Net IM dropped from $6.2 billion to $4.5 billion

- 6.1.1. Total IM at $10.35 billion is down from $14.75 billion and the same as it was on 31-Dec-21

- 16.2.17 Estimate of the risk on the invetsment portfolio (99% 1-day VaR) increased to $275k from $88k, a record high

Reports and lawsuits are still pending on the suspension of nickel trading on 8 March 2022, so we will have to wait a while longer to learn more detail on the outcomes.

Other Disclosures of Interest

Next let’s do a quick scan of 30-Jun-22 disclosures, highlighting a few historically significant ones, with a number of new record highs:

- B3 – 6.7.1 Maximum total variation margin paid to the CCP on any given day, was $4.2 billion, up from $3 billion and the highest on record

- B3 – 16.2.1 Percentage of total particpant cash held as cash deposit (including reverse repo) was 41.6%, up from 35% and a record high ( with commensurate drops in domestic government bond holdings)

- CDCC – 6.1.1 Client Gross IM required was $2.1 billion, up from $1.7 billion and a new record high

- ECC (European Commodity Clearing), which we recently added, has 4.1.4 Prefunded – Aggregate participant contribution of €3.1 billion

- ECC 6.1.1 Client Gross IM required of €44.7 billion, up from €39.8 billion in the prior quarter

- Eurex – 6.1.1 Total IM required of €105 billion is a record high up from €82 billion in the prior quarter and €39 billion on 30-Jun-2016

- Eurex – 6.7.1 Maximum total variation margin paid to the CCP on any given day was €12.1 billion, a new record high and up from €7.5 billion, €4.4 billion and €3.3 billion in prior quarters

- Eurex – 7.3.1 Estimated largest multiday payment obligation in total that would be caused by the default of a single particpant in extreme but plausible market conditions was €18.7 billion, a record high and up from €7.8 billion, €5.8 billion and €6.3 billion in prior quarters

- ICE Clear Credit – 4.4.3 Estimated largest stress loss (in excess of IM) from the default of any single participant PeakDayAv, was $1.8 billion, a record high and up from $1.2 billion

- ICE Clear Credit 6.1.1 Client Gross IM required was $41.5 billion, a record high and up from $34.8 billion

- LCH SwapClear 6.5.1.1 Number of times over the past 12 months that margin cover held against any acocunt fell below the actual mtm exposure of that member account was 8,117, a record high and up from 4,365, 1,664 and 172 in prior quarters

- LCH SwapClear 6.6.1 Average total VM paid to the CCP by participabts was $10.2 billion, a record high and up from $8.7 billion, $7 billion and $4.9 billion in prior quarters

- …..

There are a lot more Clearing Services and Disclosures but I will stop there and leave it to those of you with your own CCPView access to analyze further changes.

As well as a Web UI, we also offer an API to programatically access this data.

IOSCO Quantitative Disclosures

CCPView has disclosures from 44 Clearing Houses, each with many Clearing Services, covering Equities, Bonds, Futures, Options and OTC Derivatives with over 200 quantitative data fields each quarter and quarterly figures from September 2015 to June 2022.

Please contact us if you are interested in subscribing to CCPView.