I last looked into ISINs for Derivatives in my article on MiFID II – Why ISINs for OTC Derivatives are Bad for Transparency, so as we approach the end of year let’s check on what has been happening on this.

ANNA-DSB

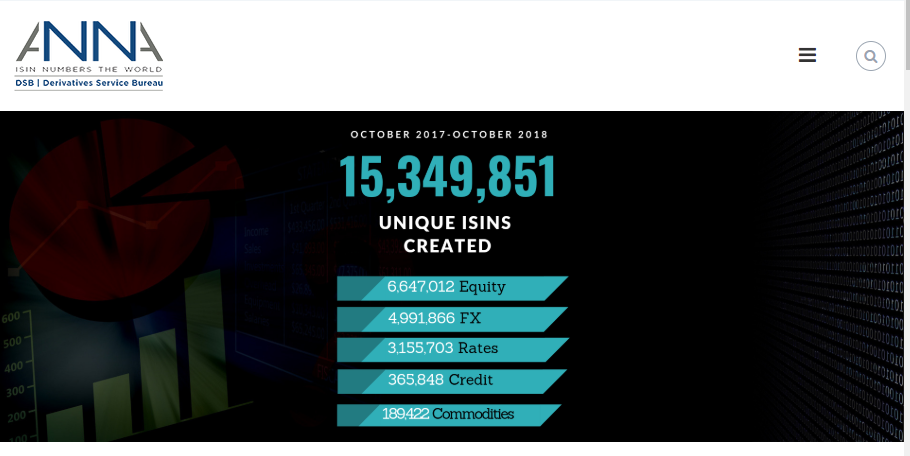

The ANNA Derivatives Service Bureau (DSB) website now provides a lot of interesting information, starting with this banner display.

Showing that there are now more than 15 million ISINs!

Equity with 6.6 million is the largest asset class, followed by FX with 5 million, Rates with 3.2 million and Credit and Commodities also rans with just 365,000 and 190,000 respectively.

That is some growth rate since January, when I noted there were 2 million ISINs.

DSB Blog

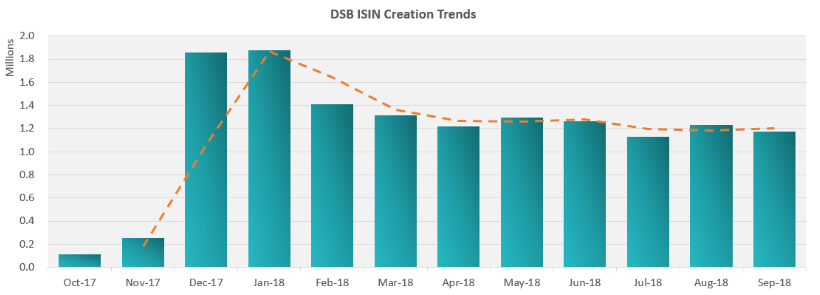

It is good to see that the DSB website provides regular blogs on ISIN metrics, which gives full transparency on the monthly growth rates.

The September article gives this nice growth chart.

Showing that after the ramp up in Dec-17 and Jan-18, the steady state is approximately 1.2 million new ISINs a month!

Further tables show that this monthly growth breaks out into:

- Equity 550,000

- FX 400,000

- Rates 200,000

with Trading venues creating most of the Rates ISINs, Banks and TVs creating equal amounts of FX ISINs, while Equity, Credit and Commodities are created primarily by Banks.

There is also a nice Pivot Table shown of ISINs by product type, which I won’t re-produce in full here (please see here for details), from which the following standout with greater than 1 million ISINs each:

- Equity, Price Return Basic Performance Single Name with 4 million

- FX Swaps with 2.1 million and FX Forwards with 1.3 million

- Rates, Fixed Float with 1.1 million

For FX Swaps, Forward and Rates Fixed Float, we know that these unreasonably large numbers are simply down to the fact that the ESMA requires a fixed maturity date for an ISIN definition, when it should instead require a tenor period e.g. 10Y and not 2028-11-08.

Such a change would make a massive reduction in the ISINs required. In my earlier article I estimated that such a change would mean we would only need about 1,000 ISINs for Vanilla IRS, which is primarily what is included in Rates Fixed Float above; so just 0.1% of the existing counts! The same argument applies to FX and even if we go with 1% instead of 0.1%, for a large margin of error, we end up with just 30,000 ISINs instead of 3 million!

The Equity, Price Return Basic Performance Single Name must be what are commonly known as Total Return Swaps on Equities, but how many equities are there with TRS traded on them? One thousand, two thousand, five thousand, ten thousand? Surely not more than that. Then there is the period of performance, 1Y, 2Y etc. and perhaps some other characteristics, but I would hazard a guess that the explosion from the tens of thousand to 4 million is also down to requiring fixed dates. (Anyone know for sure?)

Trade Counts

Another way to look at why 1.1 million ISINs for Rates Fixed Float is nonsensical is to look at actual transactions.

Using SDRView, I can see that the monthly average number of trades reported in the US for IRSSwap:FixedFloat in all currencies is 70,000 a month. January to October is 10 months, so that would make it 700,000 trades this year and the US market is larger or a similar size to Europe.

Meaning that 1.1 million ISINs is most likely greater than the number of trades in this period! I would guess that many of these ISINs have not been used for a single trade.

For an instrument identifier scheme to be of any use, it should have should have an order of magnitude less values than the number of trades on these instruments, as even for OTC derivatives there can be hundreds of trades a day in the same instrument.

Whichever way you look at it ISINs for OTC Derivatives are bad for transparency.

ESMA Q&A

ESMA does issue frequent Q&A updates and this one on page 26 has an update on Sep 26, 2018 for interest rate swap tenor and expiry date and the ISIN.

I did get my hopes up when reading this, but unfortunately it does not address the topic of replacing expiry date with a maturity tenor period.

It is however helpful in that it explains that forward starting swaps should use a different ISIN to spot starting swaps and the forward period should be in Field 41 (term of contract), so that is helpful as allows us to distinguish forward starts, otherwise it makes a mockery of price comparisons.

However it is still a muddle through with existing constraints as the examples make clear that spot starting swap traded today with expiry date of 2028-11-8 will have the same ISIN as a forward start swap traded 1 year ago, which was a 1Y10Y trade. Not good.

Anyway, some improvement is good and ESMA has given a 6 month implementation period to update how ISINs are populated, so by March 2019(?) we should see this implemented.

Onward.

ISIN Counts in 2020?

In my article on Best Execution RTS 27, I included the following paragraph:

“Now I don’t blame DSB-ANNA, they are simply following an ESMA guideline, but someone at ESMA really needs to do something about this explosion in ISINs by changing the reference data specification! Why not have an industry consultation to invite feedback or do we need to wait for 2020 and who knows what number of ISINs we will get to by then, any takers at 40 million?”

Given the growth rate of 1.2 million above, we can now answer this as 32 million in January 2020 and 44 million in 2 years time (Nov 2020). So given I left the wording lose in not specifying an exact date, I will assume I won that bet.

But seriously 44 million is not a laughing matter; when with a better design of the ESMA MIFID regulations, we would probably need less than 1% of this number.

Is anyone listening and willing to make changes?

Or are other pressing matters such as Brexit taking all the bandwidth?

MiFID II implementation might be done, but the important nitty gritty work of improving compliance with the intention of the regulations, needs to continue.

The End

I had planned to look at more from the DSB site.

Consultations, Governance Committees, the Fee model.

About which there is a lot of interesting detail.

But that is now a task for another day.

Amir,

Great article, as always.

I want to point out that the ESMA Q&A requires inclusion of both Term and Maturity in the ISIN. It does allow for distinguishing forward starting trades which is good, however it also will further increase the number of ISINs. Your 40 Mio estimate might be on the low side

Good point on forwards and thank you for the positive feedback.

Also it occurred to me that I forgot about the new RFRs like SOFR, ESTER, … soon there will be be new ISINs required for all the Swaps, vanilla and basis, further increasing the ISINs required.

40 million will indeed be a different memory with these two and no doubt other enhancements!

Interestingly the DSB saw ISIN creation activity driven by a broader spectrum of users than in the prior few months, with 10 banks and 10 venues contributing towards 91% of all ISIN creation activity.