We keep on hearing how difficult it is to be a clearing broker these days.

Case in point – this Risk.net article discusses how FCMs had to find billions of dollars in the middle of the day after the Brexit vote. This is because, when the market moves, Clearing Houses can choose to make margin calls intraday as added protection against default. However, some clearing houses are more conservative than others.

The LCH model caters for 3 of these intraday margin call cycles, along with the official end-of-day margin call. On the surface, this all seems fair. Heck if I managed credit risk at a firm, I’d always choose to be paid now rather than later. But this seems to have generated concerns about intraday liquidity. Let’s explore the problem and some of the solutions.

SAMPLE TRADES

Let’s use some of the same sample trades as we have used before. So, we have 3 separate client accounts.

(OVERLY) SIMPLE EXAMPLE

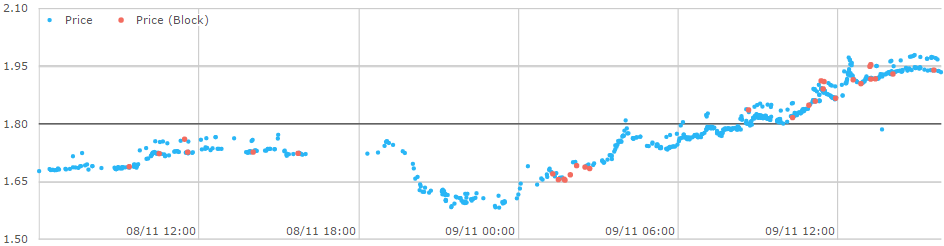

In a very simple example, let’s assume we had just the first account. The account has a couple of LIBOR paying swaps and a total DV01 of about $200,000. Going back to the post-election day of November 9th, this account would have enjoyed a wild ride, with rates down -15bp early in the morning (an interim loss), but rates closing up +25bp toward the end of the day (a significant gain of ~5,000,000).

The price action from SDRView shows this best:

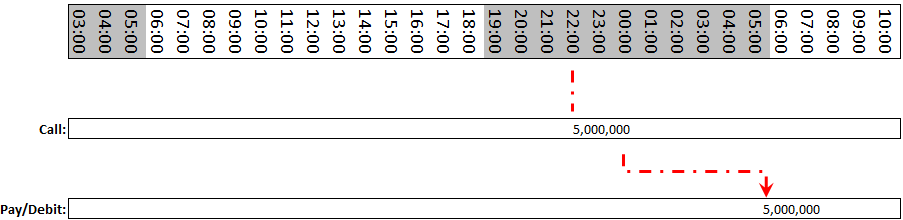

On a time scale, our variation margin, when collected once at end of day, would look something like this:

Showing:

- Around 10pm ET, a clearing house informs you that the total VM for the day is +$5 million

- By 5am ET, the clearing house credits your bank account

Except it’s not quite that easy.

MORE COMPLEX EXAMPLE

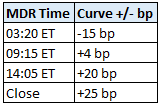

LCH has the concept of collecting intraday payments as additional protection. These are called Market Data Runs (MDR’s), which happen 3 times per day. The math behind it is “variation-margin”-esque because it’s a simple mark-to-market from last nights close, but it is not treated as variation margin. Rather, it is treated really as additional/topup Initial Margin.

These runs have typically happened at 3:20 AM, 9:15 AM, and 14:05 AM East coast time. For simplicity, as well as dramatic effect, I will assume the market action on the day across the curve corresponded to:

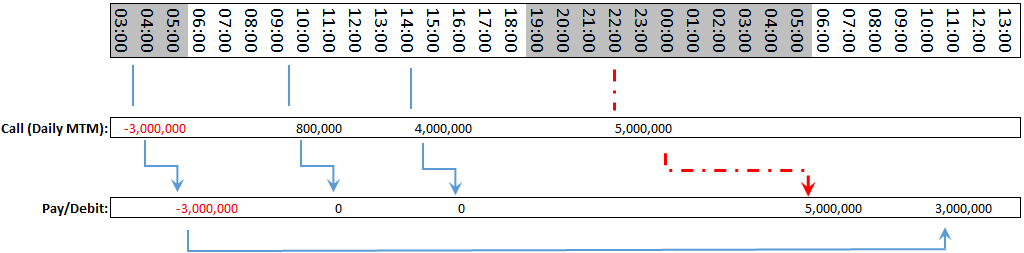

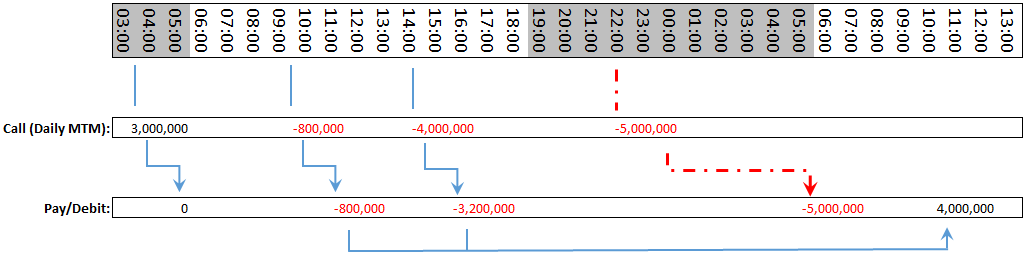

Hence for our account #1, we might see the following margin call behavior:

We can see here for this account that:

- Around 3 AM ET, with the market down -15bp, our positions have lost $3 million today, so a call is generated.

- These intraday calls need to be paid quickly, I’ve used a 1-2 hour window, so this is paid by 5 AM.

- By 9 AM ET, the market has fully recovered and is slightly up +4bp on the day, so our MTM based from last nights close is now up $800,000.

- However this is not paid back to us. That is, neither the $3 million we paid earlier, nor the additional $800,000 is given to us.

- By 2 PM ET, the market has soared higher and is up +25bp, so this account is now $4 million in the black. Once again though, we are still out -$3m in cash on the day.

- Around 5 AM on the next business day, we get paid our +$5 million from REAL variation margin

- Around 10AM on the next business day, we get our $3 million back from the previous days intraday call

In summary, the issues highlighted here are:

- Having to pay when you are down intraday, but not receive when you are up

- Not even getting your previous intraday payments back when the market turns back in your favor

- Having to wait until well into the next day to get your intraday payments back

But you could chalk this up to prudent risk controls at the clearing house.

ANOTHER EXAMPLE

Let’s now assume we only had account #2. This is the account that has LIBOR receivers. So this account profits from the early morning action in the market when yields drop 15bp. But as the day goes on and the yield curve adds on 25 basis points, the account is losing -$800,000 by 9 AM, -$4 million by 2 PM, and -$5 million by the official close. So, just a bad day at the office.

However if we look at how this is then covered throughout the day:

We can see:

- There were intraday calls paid on the 2nd and 3rd intraday runs totaling $4 million

- There was an end of day margin call for $5 million. This is in addition to the $4 million already paid. This is often referred to as the “double dipping” effect. Paying twice for a losing position.

ONE FINAL EXAMPLE

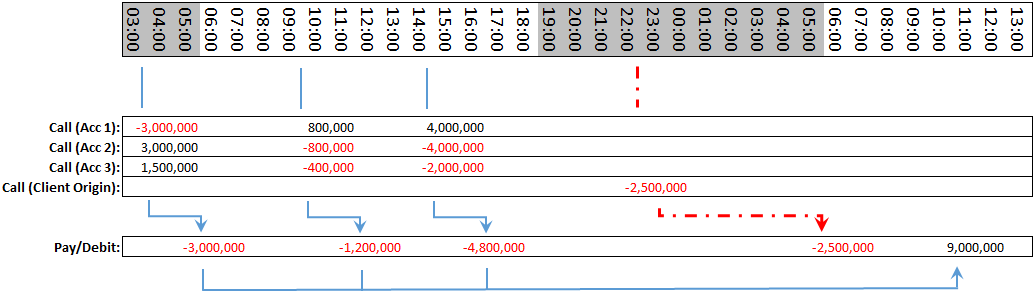

Now let’s put this all together, and assume we have all 3 accounts. We might see something like this:

I have assumed here that, for client protection purposes, these accounts are setup as LSOC-style accounts, meaning that each account has to be maintained whole, and you can’t cover account A’s losses with Account B’s gains (which is nice if you are Account B).

Hence this example highlights that intraday calls are done on a gross basis. Such that on the 1st intraday run, the client Origin is up $1.5 million, but we’re having to make good for all losing accounts by paying $3 million.

SUMMARY OF ISSUES

To summarize, let’s recap what seems to be all of the issues using this final example:

- Having to pay when down, and not receive when up

- The double-dipping effect of having to pay net daily VM (of $2.5 million) even though you’ve paid $9 million already

- This example highlights that, due to customer protection, you’re intraday topups are gross losses across accounts intraday.

- Lastly, let’s not forget that the intraday calls are done in some “IM” currency such as USD; it is value given, as opposed to specific payment in currency. What this means is that you might pledge US$9 million throughout the day to cover EUR swaps, but when it comes to the formal EOD VM payment, you will have to pay $8 million EUR.

This all implies a couple things:

- In times of financial stress, there are increased liquidity requirements both intraday and end of day. Not the best time to have to find billions of dollars.

- There is a direct funding cost associated with raising these additional funds. FCM’s are not a charity, so will have to pass it on somehow. Particularly as rates head higher, this becomes more significant.

Of course, my examples are just a few small accounts. Give these accounts larger positions, and add another 1,000 accounts, and you amplify the numbers. One of the articles claims VM calls were well above $10bn during Brexit.

CHANGES

As the Risk.net article discusses, the LCH is amending some procedures. I found a couple items on their website, as follows.

Change 1. MDR timing here.

The timing of the MDR runs were altered. Most notably, the final (3rd) run was changed from 14:05 ET to noon ET.

What I can glean from this change is quite specific to the handling of cash by the LCH. In order to secure the value of margins that are pledged to them, the LCH take all cash and invest it overnight in safe, government securities (reverse repo).

This is a prudent risk management feature (short of giving it to the Central Bank!). However this means that cash movement is dictated/restricted by the timing of the repo market. For one thing, this explains why firms do not get their intraday cash back early in the morning the following day – we need to wait for the repo to settle for the cash to be available.

But I also glean that there was a problem with the previous 14:05 ET intraday margin call. It seems banks were making good on this by about 4pm ET, which meant that it missed the cutoff for the overnight repo market. I further glean that this meant that by the time it (the 3rd call) was pledged, it was not to be delivered back to the clearing member until effectively T+2.

Moving this final margin call forward in time to noon ET allows for the cash to be put into the repo market and returned for T+1.

Change 2. Treatment of Unallocated Excess here. This change, per the document, appears to have gone into effect last week.

This change seems to imply that some of the surplus cash the FCM has lodged at the DCO can be used for intraday requirements.

You can quickly get lost in the weeds of the various customer protection models (LSOC with excess, LSOC without excess, etc, etc). And this is no different. But here is my take:

- Unallocated Excess is surplus funds held at an FCM’s account at a DCO that is not attributable to any particular client account. These funds can never be used by the DCO to fulfill a client account obligation (because they don’t know which client account should get it). And in the case of default, Unallocated Excess is given to the trustee to figure out if and how it can be used. Basically, Unallocated Excess cannot be touched / used by the DCO; it exists as a cushion.

- Client accounts that are treated as “LSOC without excess” have an amount of legally segregated collateral that is equal to their Initial Margin requirement. (Note that clients treated as “LSOC with Excess” have an amount of legally segregated collateral that is defined/reported to them by the FCM. Eg: Account ABC has 10 million dollars.)

- Hence, day over day, as margin requirements for “LSOC without excess” client accounts change, this unallocated excess will go up and down (amount of total client collateral being constant and client requirements changing)

- Under this new rule, it seems as though this unallocated excess can be used for intraday margin calls (by transferring / re-labelling it “FCM Buffer” instead). Per the LCH letter: “enable the excess collateral to become available for trade registration or to cover intraday margin calls”.

So this seems nice, and might help to get through some of the intraday calls unscathed. The only caveat would seem to be that some of that collateral value MAY be attributed to a client. I suppose the assumption is that every day, as clients IM requirements reduce, that it’s the clients job (under “no excess”) to get their money back from the FCM. Hence if that were true, any unallocated excess at the DCO could be thought of as FCM collateral.

Also, there seems to be such an account already for SCMs of LCH Swapclear (under EMIR segregation rules) called Client Buffer, that already does basically this. This leads me to believe this specific issue of using excesses intraday is only an issue for US FCMs.

Both of these changes would seem to help, but I think they miss what I would consider the most glaring issue with the hindsight of Brexit and Trump election: If I’ve paid to topup a losing account earlier in the day, and that account has now turned positive, why would I not get any previous intraday payments credited back to me?

I must say, of all of the topics I’ve researched, this whole Intraday MDR one is as clear as mud. So don’t take anything I say here as the gospel.

CHARM

Whenever I research things like this, I am always reminded of the importance for FCM’s to have a clear view of risk. That should include both appropriate risk estimates well in advance of stressful days (running stress tests / worst case scenarios), as well as having real intraday numbers updating for you when that day eventually comes.

It’s why we built CHARM.

MUCH OF A MUCHNESS

Before I close, I wanted to point out that this intraday margin call process should not be construed as better or worse than other clearing houses. Every clearing house has their own prudent risk management processes, all with benefits and consequences.

Look no further than my recent article on the CME margins post-election. We observed there that in times of stressed markets, CME’s initial margin model is significantly more reactive than LCH’s. On the flipside, we see here how LCH’s covering of intraday “initial margin” is much more reactive than CME’s (CME does not have normal intraday cycles for cleared swaps).

Hence each clearing house has its own ways to ensure appropriate coverage of client accounts.

Good article

Quite helpful – thank you.