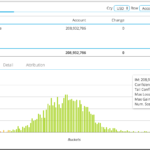

クリアード・スワップの証拠金に係るバッファーの見積もり

中央清算機関(CCP)とクリアリング・メンバー(メンバー)との間で行われる、或いはメンバーとクライアントで行われる、日々の変動証拠金(VM)のフローはかなり大きなものとなっている。例えば、LCHの公表しているCPMI-IOSCO Disclosuresは、メンバーからCCPに支払われる1日の変動証拠金の総額は160億ドル!となっている。

FRTB – The Default Risk Charge

Following on from my articles, Fundamental Review of the Trading Book and Internal Models or Standardised Approach, I wanted to take a look at a specific component of the Market Risk Capital, namely the Default Risk Charge as required under the Standardised Approach. Background In January 2016, the Basel Committee on Banking Supervision (BCBS) published its Standards for Minimum […]

Two Month Update: Uncleared Margin Rules & Swap Data

Over the past 2 months, my colleagues and I have occasionally studied swaps data for hints of impacts from the September 1 implementation of Uncleared Margin Rules (UMR) effecting behaviors. There have been a few general themes: Uptick in NDF Clearing Uptick in Inflation Swap Clearing No notable effect on Swaptions Now with 2 months […]

BRL NDF Market – 30% of Dealer to Dealer flow is now cleared

We look at the USDBRL market in the latest in a series of NDF blogs Clarus data covers over 66% of the market on a trade-by-trade basis For the Dealer-to-Dealer market alone, our coverage increases to 73% Our data shows that clearing has increased from 6% to 31% of dealer-to-dealer flows. Bringing Old Blogs Up To […]

Calculating MVA under ISDA SIMM™

We describe how to calculate Margin Valuation Adjustments under ISDA SIMM™. This is a simple four step process starting with Risk Projection and IM calculation. And concluding with present valuing the margin costs. We then compare the MVA adjustments for both cleared and uncleared swaps. What is a Margin Valuation Adjustment (MVA)? As Amir stated back […]

Sizing the Margin Buffer for Cleared Swaps

Daily Variation Margin flows between Clearing Houses and Clearing Members and between Clearing Members and their Clients are sizeable e.g. we know from LCH SwapClear’s CPMI-IOSCO Disclosures that the highest VM paid on a single day by all members to the CCP was $16 billion! As Clearing Houses make intra-day margin calls, Clearing members generally maintain […]

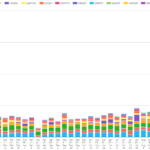

ブローカー間におけるスワップ証拠金の最適化

相対取引に係る証拠金を減らすために、バックローディングと言う賢明な選択がある。そこで清算参加者がいかにクリアリングを要する取引のために必要となるキャピタルを削減できるかについて、8月に記事を書いた。

Microservices and the Amazon Cloud

Capital Markets have been at the leading edge of adopting software technology to gain advantage and increase automation, but in the recent past have fallen behind the curve compared to the infrastructure, practices and technologies used by the Tech sector. Background I remember like it was yesterday (actually 1990 🙂 ) using Cobol on an IBM Mainframe while […]

Optimizing Swaps Margin Across Brokers

Back in August I wrote an article about how large, self-clearing firms can reduce the amount of capital required to support their cleared business by wisely choosing to backload margin-reducing bilateral trades. While I wrote that about large banks, there is an analogous case for trading firms that do not self-clear. In fact, we’ve been […]

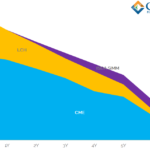

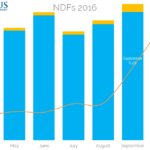

BIS 2016 FX Data – how much of the NDF market is Cleared?

We look at the FX data within the BIS triennial survey And show the evolution of NDF clearing since the UMRs came into force in September 10% of the market is currently being cleared, up from just 2% in April A background to NDF Data This blog will tie together a couple of themes from my recent blogs covering BIS […]