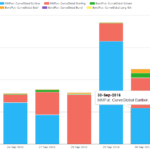

September 2016 Swaps Review

Continuing with our monthly review series, let’s take a look at Interest Rate Swap volumes in September 2016. First the highlights: On SEF USD IRS Septmber 2016 volume was 5% higher than August Curve trade volume was down and Outright up from prior month SEF Compression activity was a healthy $200 billion in USD IRS USD OIS Volumes at >$2.4 trillion, again exceeded […]

BIS 2016 Data and Clearing Mandates

We look at the BIS Triennial Survey to calculate what percentage of global derivative markets are currently being Cleared. We use CCPView to look at trends in this data. The CFTC have recently published their Clearing Mandate for Additional Currencies, with other jurisdictions announcing clearing mandates for next year. We therefore look at the timelines for things to change. As more […]

CCP Disclosures 2Q 2016 – Trends in the Data

Central Counterparties published their new CPMI-IOSCO Quantitative Disclosures, so we now have four sets of disclosures covering a whole year. Lets look at trends in the data, similar to my article on 1Q 2016 trends. Background Under the voluntary CPMI-IOSCO Public Quantitative Disclosures by CCPs, over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity […]

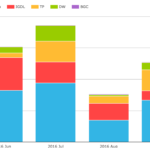

New EUR & GBP Interest Rate Futures

Last week saw the launch of a new futures exchange – LSE’s CurveGlobal. We have pulled the data for the first week, and I thought it appropriate to explore this market. The general overview of CurveGlobal: 30% owned by LSE Group. Remaining 70% owned by CBOE, BofA, Barclays, Citi, Goldmans, JPM, SocGen, BNP STIR (3-month […]

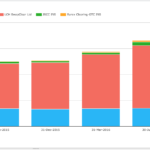

NDF Clearing – what is trading?

We look at the volumes being cleared in NDFs The growth is impressive, with nearly $200bn cleared in September This growth accelerated in the final weeks of September USDINR saw the highest volumes and USDBRL saw the largest growth Tod took a look at NDF clearing as of the 20th September, noting that volumes were really beginning to take-off. […]

ISDA SIMM マルチ・カレンシー・ポートフォリオ

ISDA SIMMを使ったIMの計算をマルチ・カレンシー・ポートフォリオで見てみよう

ISDA SIMMでは、異なる通貨間のセンシティビティの合算には、相関係数として27%が指定されている

クリアーとアン・クリアーから生じる証拠金額の差異は、リスク・プロファイルに依存することが解った

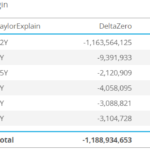

Moving Euro Clearing out of the UK: the $77bn problem?

We estimate the Initial Margin impact from moving EUR Clearing out of the UK This could happen as a result of Brexit We can make an estimate as to the maximum margin impact possible using publicly available data In terms of Initial Margin, we only see a small impact on the LCH SwapClear portfolio in London But […]

Direct Clearing For Dummies

Back in July of 2016, the CME submitted a proposal to the CFTC for a new class of clearing membership which they call “Direct Funding Participant” (“DFP”). I was drawn to the topic last week when Bloomberg wrote an article about its imminent effective date of Sep 23, 2016. As it happens, it appears that date was […]

Trading Obligation for Derivatives under MiFIR

I last looked at this in Oct 2015 in my article MiFID II and the Trading Obligation for Derivatives and now that a year has passed there is a new ESMA Consultation. The accompanying discussion paper is here and in this article I will review the key elements of the consultation. Background Once a class […]

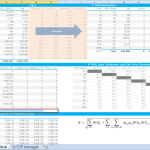

ISDA SIMMをExcelで計算する

ISDA SIMM の方法書を見てみよう

金利商品について、ISDA SIMMに従って当初証拠金(IM)を計算するためのExcelスプレッドシートをつくりたい

そして、ISDA SIMMまたは中央清算における、単独トレードとポートフォリオに関するIMの計算について概略をのべる