Basel III Leverage Ratio

The Basel III Leverage Ratio, often referred to as the Supplementary Leverage Ratio (SLR), is one of the important new metrics introduced as a response to the Financial Crisis of 2007-08 and one which continues to receive a lot of press coverage and discussion. In this article I will provide an overview and some of the […]

NDF Trading After 1st March

Open Interest of NDFs has set new records recently. Volumes have continued to be elevated compared to 2016. We have not seen a significant change in behaviour since the 1st March VM big bang. Overall, we estimate 15% of the entire market is now cleared. Up to 35% of D2D volumes are being cleared during any […]

Impact Of March 1st VM Regime

The big VM deadline has come and passed. Did trading grind to a halt? Prior to the date, based primarily upon what I had read in news articles, I would summarize my sentiment around the VM implementation as: The industry had not gotten through even half of the required new paperwork Large asset managers being […]

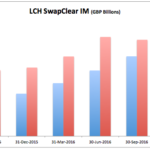

Initial Margin Optimization

Summary: Initial Margin requirements for OTC Derivatives are large and increasing at CCPs IM Optimization is a periodic or trade by trade analysis that seeks to reduce overall IM Clearing members can achieve significant cost and capital benefits Similar techniques can be extended to UMR and ISDA SIMM Client IM is growing much more rapidly than […]

Exploring Energy Swaps On The SDR

Back in August, I had a look at the wealth of commodity data on the US Swap Data Repositories. The general takeaways were: There’s lots of data Much of it is murky. Describing many OTC commodity trades require lots of details that are missing. Case in point, we found the second most active commodity to […]

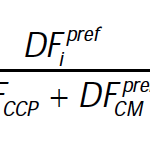

ISDA SIMM™ in Excel – Equity Options

We build an IM calculator in Excel for Equity Options under ISDA SIMM™. The methodology builds on the margin methodology for Swaptions, and uses very similar formulae. We cover all forms of IM. This blog is for the Vega and Curvature Margin. There are subtle differences to the implementation for Rates. UPDATE: We now offer free […]

Swaps Data: Volumes rise, CCP Switches Spike

I wrote an article for Risk.net, reviewing recent trends in Swap volumes, available at this link. (Complete with my bang up to date picture, time has flown by ……, only 15 years to be precise.)

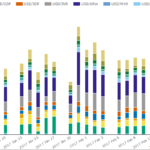

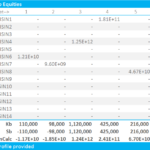

Capital requirements for exposures to CCPs

Following on from my article SA-CCR: Standardised Approach Counterparty Credit Risk, I wanted to look at the related topic of Capital requirements for Cleared Swaps and get a sense of the size of these requirements. Background In March 2014, the Basel Committee on Banking Supervision (BCBS) published it’s Standardised Approach (SA-CCR) for measuring exposure at default […]

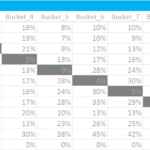

ISDA SIMM™ in Excel – Equity Derivatives

We build an IM calculator in Excel for Equity Derivatives under ISDA SIMM™. The methodology builds on the margin methodology for Rates products, and uses very similar formulae. We cover all forms of IM. This blog is for the Delta Margin. There are subtle differences to the implementation for Rates, mainly around the concept of “buckets” […]

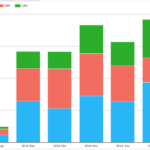

January 2017 Swaps Review

Continuing with our monthly Swaps review series, let’s look at volumes in January 2017. Summary: SDR USD IRS price-forming volume > $2.3 trillion gross notional 21% higher than a year earlier On SEF vs Off SEF at 62% to 38% is lower than average; 65% to 35% SEF Compression activity in USD IRS was > $220 billion USD OIS volume at […]