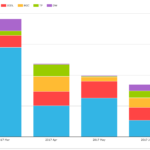

June 2017 Swaps Review in 15 Charts

Continuing with our monthly Swaps review series, let’s look at volumes in June 2017. Summary: SDR USD IRS price-forming volume > $2.1 trillion gross notional, similar to a year earlier SEF Compression activity in USD IRS > $300 billion, 51% higher than a year earlier On SEF IMM Roll volume > $60 billion USD OIS price-forming volume was > $2.7 trillion, again […]

MIFID II Transitional Transparency

ESMA have published Transitional Transparency Calculations for a number of asset classes. These calculations define which asset classes and instruments are deemed liquid for the purposes of making trade data public as of 3rd January 2018. Anything deemed “illiquid” will likely have a two-day lag applied to the trade record being made publicly available. The transitional […]

New Swap Execution Facilities

There have been a couple noteworthy advances in SEF’s in July. The NEX SEF has launched, and LedgerX has been approved. Let’s have a look at these. BLOCKCHAIN We’ll start with the bitcoin venture LedgerX, who applied for SEF registration in January 2017 and was approved on July 6. They put out some press in […]

GBP Swaps for Dummies

GBP IRS markets are the third largest Interest Rate Derivatives market. Almost 100% of volumes are cleared at a CCP. Most trades are standardised contracts versus 6 month Libor (IRS) or SONIA (OIS). SONIA swaps are frequently forward-starting out of MPC dates and IMM dates. 42% of GBP Libor swaps are forward-starting; spot-starting swaps account […]

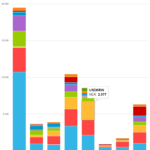

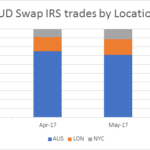

AUD Swaps: What Does the Data Show?

Over the last few years we have published many blogs on the AUD Swap market. Amir also includes an AUD summary in his monthly swaps review. The DTCC does publish some market info from the Australian SDR, but the aggregated nature of this data does not allow for a meaningful analysis of what is actually […]

Swaps Data Review: A Day in the Life of a Swap

My Monthly Swaps Data Review for Risk Magazine was published today. This looks at what can be seen in price data for Interest Rate Swaps by focusing on June 14, 2017 (the most recent FOMC meeting) and three of the highest volume products: USD 10Y Swaps USD 10Y Spreadovers USD Curve/Switch/Butterfly Swaps in 10Y Trade prints, […]

MIFID II: ESMA Trading Obligation

ESMA published their latest Consultation on Trading Obligation for Derivatives under MIFIR on 19th June 2017. EUR, USD and GBP swaps are deemed liquid and will be covered by the Trading Obligation under the current proposal. JPY, NOK, SEK and PLN swaps will continue to be covered by the Clearing Obligation but will not be […]

CME-LCH Basis For Dummies

We occasionally still get asked about the price differential between CME and LCH swaps. I typically refer folks to our online articles that have explained the phenomenon. Since 2014, we have written 18 separate pieces on the CME-LCH basis spread. A few of the ones that begin to quantify it include: May 20, 2015 – […]

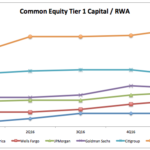

Capital Ratios and Risk Weighted Assets for Tier 1 US Banks

Following on from my recent Supplementary Leverage Ratio: Comparing US Banks article I wanted to look at Capital Ratios and Risk Weighted Assets (RWAs) published by the six largest US banks. Background One of the lessons learned from the Great Financial Crisis (GFC) was that Banks were generally under-capitalised for the risks they were exposed, leading to new […]

NDF Clearing Update

Little has changed in FX NDF Clearing since our last update in March. From the data, Clearing is now a “business as usual” operation for a significant sector of the market. We further refine our data methodology by introducing an estimate of the errors inherent in our market share metrics. These errors look to be acceptably small, at […]