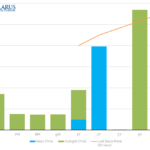

RFRs – CHF SARON Activity

We noticed that the SNB quoted Clarus data at the most recent CHF SARON working group. We show that Open Interest in SARON now stands at nearly CHF60bn. Most of this is in short-dated products, less than 2 years. We find that 77% of risk is traded in tenors shorter than 2 years. Markets need […]

Swaps Data: Volumes Up amid Volatility

My monthly Swaps Review in Risk Magazine looks at: Cleared Interest Rate Swaps in USD, EUR, JPY Cleared Credit Default Swaps in USD, EUR Cleared Non-Deliverable Forwards Volumes in 3Q18 vs 3Q17 Volumes in Oct-Nov18 vs Oct-Nov17 Growth rates in these periods Please click here for free access to the full article on Risk.net.

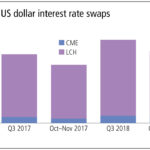

Eurex Swap Volumes On the Up

Given the continuing uncertainty around Brexit as the UK government struggles with a parliamentary vote, I thought it was time to re-visit EUR Swap volumes, which I last looked at in early October 2018. I noted then that Eurex market share in the third quarter was 0.96% and little changed from the corresponding quarter a year earlier. […]

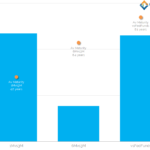

What is Left Uncleared in 2018?

We take a look at the total size of uncleared derivative markets. FX Options are the largest Uncleared market, followed by Swaptions and NDFs. Cross Currency swaps are the fourth largest uncleared market. Around $5.5trn each month trades uncleared – almost equivalent to the US market for cleared IRS. Uncleared Markets The death of uncleared […]

Non-Dealer users of RFRs: The need for term rates

Over the last year it has become obvious that Libor will not have a long-term future; so why are market participants still writing derivative and loan deals as well as issuing bonds linked to Libor?

Liquidity in markets linked to new benchmarks is gradually increasing but still falls short of dominating Libor-based product.

LIBOR Basis Swaps

For the first time, basis trading reported to the SDRs has topped $1trn in a single month. Similarly, global basis trading has now topped $2trn cleared at LCH SwapClear in a single month. We see that average maturity of basis trades varies according to the indices being traded. Activity in 30y and 50y basis trading […]

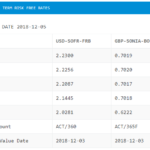

RFRs – ISDA announce LIBOR fallback methodology

ISDA have announced a preliminary methodology for Libor fallbacks. This will be the RFR plus a historical spread. This announcement could have a pronounced impact on basis trading. Elsewhere, we have seen continued SOFR trading and the results of the BoE Term Sonia consultation. CLARUS01 already replicates this LIBOR fallback methodology. Risk Free Rates Everywhere […]

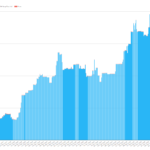

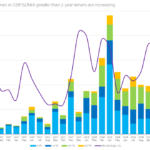

RFRs – OIS trades are getting longer!

OIS trading is seeing increasing activity in longer tenors in both USD and GBP. We look at tenor data out of LCH SwapClear to present the volumes in DV01 terms. We find that the amount of long-dated risk traded in 2018 is 2-3 times higher than in 2017. Our series on Risk Free Rates, looking […]

ISDA SIMM 2.1 – Are You Ready for Implementation?

ISDA SIMM 2.1 is effective December 1, 2018 Updated with a full re-calibration and industry backtesting Initial Margin will change for all counterparty portfolios Our Customers can check the impact leading up to the effective date And can be confident on implementing SIMM 2.1 on time If you are interested in joining them, we offer free […]

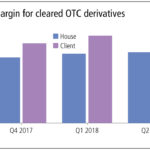

Swaps Data: Cleared vs Non-Cleared Margin

My monthly Swaps Review in Risk Magazine looks at: Initial margin for non-cleared OTC derivatives Initial margin for cleared OTC derivatives Growth rates in each of these Multilateral netting benefits Increasing Clearing Please click here for free access to the full article on Risk.net.