CME and LCH propose to change USD Swaps discounting and Price Alignment Interest (PAI) from Fed Funds (EFFR) to SOFR on October 17th 2020. By creating SOFR discounting risk from that date, this change should result in a need to hedge SOFR risk and drive increased liquidity as well as extend the tenors of SOFR Swaps trading.

CME’s latest SOFR price alignment and discounting proposal synchronized watches on the above date with LCH’s SOFR Discounting Letter. Whilst, there remain some subtle differences between the two approaches, there is a feeling of the plan gelling.

Below I give some cleared trade volumes context, outline the main elements of the change and highlight obvious high-level requirements of participants.

Volumes

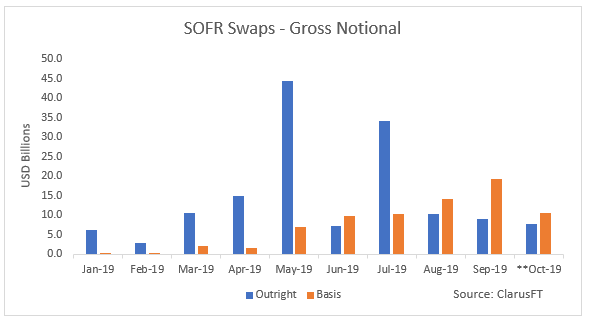

By contrast with USD OIS, the GBP OIS market is already on the chosen RFR; SONIA. CCPs already discount GBP trades on SONIA. SOFR OIS is in comparative infancy with the Effective Fed Funds Rate (EFFR) or “Fed Funds” remaining the dominant USD OIS index. As a result, more forensic data analysis is required to the SOFR swaps. This can be seen in our recent blogs – most recently Amir’s SOFR Swap Volumes – October 2019, from which I present the first chart below.

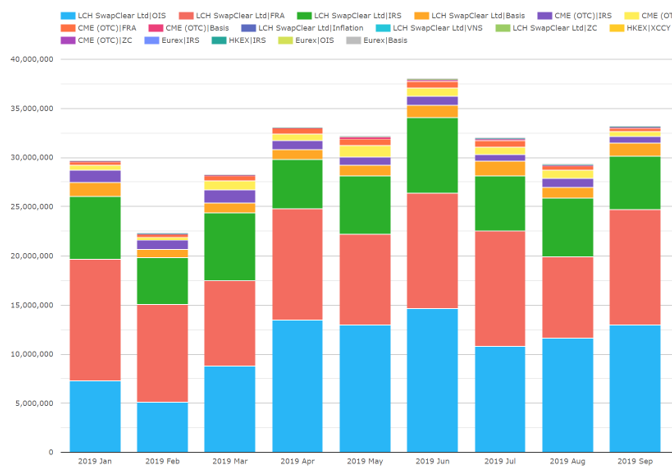

Next a chart from CCPView showing all USD OIS volumes in context of all cleared USD IRD globally by product.

If we compare the two charts and May monthly volumes we see:

- $~40bn or $~0.04tn outright SOFR OIS notional traded (a peak month for the year to date)

- $~14tn USD OIS notional traded so SOFR OIS is less than 0.3% of the total OIS

- $~32tn USD cleared IRD notional traded

It’s hard to predict, but after the SOFR discounting change you, we might expect to see SOFR OIS trading break the $1tn monthly volumes or more.

Discounting change

At this point, it’s worth noting that swap participants will separately make an internal reporting change to transition their own PnL and risk management to SOFR discounting. In this blog the PVs and risk mentioned are those from the CCPs calculations which directly impact on CCP VM and IM. The in-house change is a much deeper and broader impact for participants which impacts participants own PnL and risk management. Nonetheless, managing the SOFR discounting risk effects on CCP margin is reason alone to increase trading in SOFR futures or SOFR OIS.

Requirement –participants may want to forecast the impacts on CCP PVs, VM, IM and risk.

Requirement – participants may want to set up trading and booking infrastructure for SOFR Futures and Swaps.

A quick aside on Tools

If you’re waiting for in-house development to be able to assess these impacts, our LIBOR Transition tools represent a great solution which can easily be set up and integrated with your daily CCP member / client files – with your organizations permission. This integration path has been proven with many clients and no further upfront trade data, market data or discount factor integration is required to enable you to:

- Perform the above forward simulation of the CCP PV and risk change at the SOFR discounting change for your member/client portfolios on a full reval. basis

- Analyze and drill down the impact to trade, risk factor and tenor point details

- Do what if calculations on trades and portfolios to mitigate the SOFR discounting change exposure

Further the tools are flexible to use via integrated GUI, streamlined microservices API in a spreadsheet or integrated fully into trading, XVA, Resource Management or Treasury applications.

If you would like to discuss or get a demo, please reach out via [email protected].

Mandatory Compensation

CCPs could limit themselves to changing the discounting. The CCP’s normal VM process would exchange cash to compensate the difference in PV. Participants would hedge the change in portfolio risk directly in the market. Perhaps for convenience and good order in consultation with participants, they have decided to mandate compensation. This flattens the PnL and risk effects in two steps:

- Calculating and settling a cash payment (or receipt). The amount is equal and opposite to the aggregate of trade level changes in PV across the USD swap trades in a client or member portfolio

- Creating a set of on-market FedFunds-SOFR basis swaps. The basis swaps aggregate risk is equal and opposite to the aggregate change in sensitivities in a client or member portfolio.

Both changes are flat cash and risk at the CCP level i.e. across all participants. As a side note, while LCH proposes to exclusively use basis swaps, CME offers a choice of basis swaps or economically equivalent pairs of FedFunds and SOFR OIS trades. Given the economic equivalence, I ignore this difference for brevity in the rest of the blog. However, SA-CCR watchers may want to take note that FedFunds-SOFR basis swaps are a separate hedging set from outright USD IR swaps. (See paragraph 162 of BCBS SA-CCR). This may affect US banks most directly, if the FRNs proposed July 1, 2020 SA-CCR go live is confirmed.

After the discounting change and mandatory compensation, participants are left with a cleared portfolio consisting of:

- USD IR swaps discounted using SOFR instead of FedFunds, including fixed float IRS, OIS, basis swaps, inflation swaps, ZC swaps, VNS and non-deliverable Swaps (settled in USD).

- Flat PnL with a shift between NPV and cash (in either direction)

- Flat FedFunds risk and flat SOFR risk with a shift in the trades representing the risk from FedFunds-discounted IRD trades to SOFR-discounted IRD trades plus the FedFunds-SOFR basis trades.

In effect the FedFunds discounting risk has been separated into different trades from the LIBOR projection risk. Now, LIBOR and FedFunds legacy risk can be separately hedged or traded out using normal market mechanisms (voice, electronic etc.). I expect participants will terminate or offset trades in the legacy index and replace with SOFR trades in various combinations. We hope to blog on the details of trading out as they emerge.

Requirement –members and some other participants need to prepare to trade, book and risk manage FedFunds-SOFR basis swaps .

Residual Complexities

I’m grateful for Risk.net’s interesting recent webinar Shining the Spotlight on SOFR, which helped to bring to life some residual aspects which remain to be finalized:

- Basis swap client opt out – clients can opt to receive (or pay) cash instead of receiving the FedFunds-SOFR basis swaps.

- Basis swap auction – mandatory for members, this process will sell the opted-out basis swaps to the highest bidder and provide the cash to compensate clients opting out of basis swaps.

- Basis swap pricing – the auction winning bids will help to set the FedFunds-SOFR basis swap closing price for CCP margin purposes.

- Swaptions exercised after the change – discussions remain in train on how to compensate parties to swaptions exercised into cleared swaps after the CCP change has happened.

For today’s blog, I’ll hold of elaborating these points, but will shortly produce a follow up blog to cover them.

Summary and takeaways

The picture is solidifying of how the CCP SOFR discounting change will happen.

- CCPs will apply the discounting change and render participants flat PnL and risk on the change by providing mandatory compensation in the form of cash (PnL) and basis swaps (risk).

- Participants may need to forecast the effects of SOFR discounting effects on CCP margin.

- Clients can opt out of receiving basis swaps and instead receive cash generated by a basis swap auction among members.

- Participants may need to be ready to hedge the resulting portfolio by being able to trade and risk manage SOFR futures, SOFR OIS and FedFunds-SOFR basis swaps.

We’re interested in any and all your views and questions on the CCP SOFR discounting change. Please comment on this blog or click [email protected] to email us if preferred.

Before I go, did I mention Clarus tools can help?

Clarus LIBOR Transition tools can help foresee and optimize the CCP SOFR discounting change impacts on your organization. You can be up and running in a matter of days. If of interest to you, please email us at [email protected] to ask us for a discussion or demo.

That’s all for today.