Is Transparency Helping Markets Function?

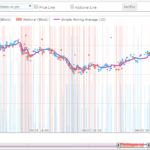

Trading has continued uninterrupted across the markets that we monitor, despite the extreme levels of volatility we have seen over the past week. Transparency data shows that Rates, Credit and even Funding markets continue to function “normally” in terms of volumes transacted. Crucially, markets have not “seized up” during some crazy price moves. Market participants […]

Crashing Rates and Swap Margins

In observing the markets over the last few weeks there are so many significant moves; Oil prices collapsing by 30% in a day, S&P500 declining 7.6% in a day, the 7th worst move since WW2 and worst since 2008, the whole US Treasury Curve out to 30Y trading below 1% for the first time ever. […]

SONIA Update

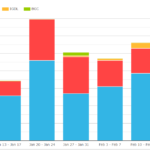

70% of GBP risk transacted last week was in SONIA. Just 7.6% of GBP notional cleared at LCH SwapClear was in LIBOR last week. In these extremely volatile markets, much of this activity is due to large amounts of short-dated risk trading. 91% of SONIA risk was in short-dated tenors (2 years and shorter). There […]

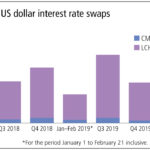

Swaps Data: Cleared volumes drop for all markets – except FX

My monthly Swaps Review looks at 4Q 2019 volumes compared to 4Q 2018 and CCP market share for: Interest Rate Swaps in USD, EUR, JPY Credit Default Swaps Non-Deliverable Forwards Please click here for free access to the full article on Risk.net.

‘Dear CEO’ letters to Asset Management Firms

On the 27th February 2020, the UK FCA wrote to asset management firms to emphasise the need to prepare for LIBOR to likely become unusable after December 2021. This extended previous ‘Dear CEO’ letters from 2018 to major banks and insurers and was designed to ensure firms are well prepared for LIBOR cessation. As we […]

SONIA Day – LIVE Blog

Today has been circled in the calendar for a while now. Monday 2nd March is intended to see a change in GBP swap markets. From now on, the market convention should be to trade SONIA swaps instead of LIBOR. We covered the original announcement in this blog. 19:24 London Final post for this live blog. […]

SOFR Swaps and SEF Venues

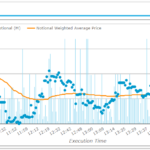

We have dedicated Risk Free Rate (RFR) views in most of our data products and today we complete the picture by adding these to SEFView, which aggregates daily volume from all Swap Execution Facilities. Let’s use this to see where SOFR Swaps are trading. D2D Venues The inter-dealer market trades SOFR vs FedFunds Basis Swaps, […]

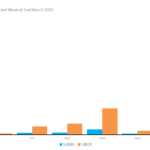

Block Trades in HKD Derivative Markets

HKD Interest Rate Derivatives are the 5th most traded APAC currency. They trade in a range of maturities out to 30 years, but the block thresholds and lack of SEF market prevent us seeing the true size of trades. USDHKD FX Options are at least a $750bn per month market. Transparency in this market also […]

Trading RFRs

Clarus will be talking about trading RFRs at the ISDA/SIFMA AMG Benchmark Strategies Forum 2020 in London next week, February 26th 2020. For more information on the event and to register, please check out the event details page. It is free to attend for the buyside. Among the topics, you will hear our thoughts on: RFR […]

Spotlight on RFR Swaps

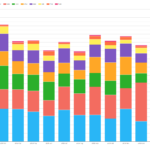

As the spotlight turns to RFR Swaps, in a “will they won’t they take off and replace Libor”, we have added new RFR views in most of our data products, to help answer that question. Today I will use SDRView Researcher and our new IBOR-RFR view to shine a spotlight on RFR Swaps. RFR Swaps […]