Swaps Data: How the market responded to Covid-19

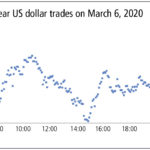

My monthly Swaps Review looks at USD Swap volumes over the volatile February to March period, covering Daily and monthly volumes for USD IRS and OIS Days with largest 1-day price changes and volumes Prices of trades on March 6th Please click here for free access to the full article on Risk.net.

CCP Quant Disclosures 4Q19 – Default Resources

4Q 2019 CPMI-IOSCO Quantitative Disclosures for CCPs have just been published and while we are still focused on the Covid-19 pandemic and resulting market volatility, I thought it would be interesting to see what the data shows as of a Dec 31, 2019, before we had any idea what was coming. So a little different to […]

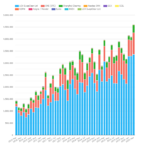

Swap Markets see Record Trading Volumes in response to COVID-19 Market Turmoil

March 2020 saw a flurry of volume records set in interest rate derivatives. The big SEF winners were ICAP, Bloomberg and Tradeweb. Overall, D2D On-SEF volumes for USD IRS hit a new record of ~$1trn. CCPs also saw new combined volume records. Over $50trn was cleared in the top six currencies alone. Over $4.5trn cleared […]

MIFID II Transparency – Can we get it right this time?

There is a new April 2020 ESMA consultation on the Transparency Regime for OTC derivatives. ESMA are proposing potentially wide-sweeping changes to post-trade transparency in their latest consultation. Deadline for responses is currently April 19th 2020. We encourage all market participants to respond to this vital consultation. We could finally witness the beginning of transparency […]

Benchmarks in times of high volatility

Important current benchmarks like LIBOR, other IBORs and ICE SwapRate can have challenging characteristics during periods of high volatility. In some cases, price discovery can be difficult, which can be costly for some users and conversely rewarding for others. In this blog I will look at a few of the current benchmarks and some of […]

USD Swap Markets during COVID-19 Pandemic

Statistical measures show that USD swaps liquidity has deteriorated in the past six weeks. Specifically, price dispersion of 10Y USD swaps has tripled since early February. This is consistent with anecdotal stories in the press. However, we are still seeing higher than typical volumes transacted. Trading may be more difficult, but we are not seeing […]

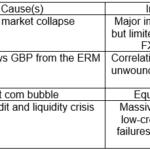

Crises and Volatility – Trading Challenges

Over the course of my trading career I have had the ‘opportunity’ to be part of the trading process during market crises, both as a junior trader and as a manager of trading teams. My previous experiences were: 1987 equity crash; 1992 correlation unwinds; 2001 tech bubble burst; and 2008 global financial crisis The one […]

Mechanics of Central Bank FX Swap Lines

We detail the trades required to raise USD from a local central bank, using the Fed USD swap lines. We show that the cost of these USD is substantially below that implied from FX markets. The FX haircuts on non-USD collateral for these operations vary between central banks. The largest amounts outstanding in these USD […]

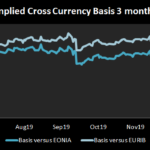

Cross Currency Swaps Trading During a Crisis

Cross Currency Swaps trading fundamentally changes during a funding crisis. I run through the impacts to the risks that are being managed and the daily flow of news that drives trading activity. There are various drivers ranging from FX markets, LIBOR fixings, futures convergence trades, central bank operations and client demand. Most traders will only […]

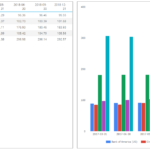

Want to know all about Global Systemic Banks? Introducing GSIBView

GSIBView is the latest data product from ClarusFT. We collect and calculate the GSIB scores for 118 banks. Data shows how GSIB scores and components change over time. Drill-down into components and compare across peer groups. This blog looks at funding data, payments data and derivative notionals of RBS, ICBC and Morgan Stanley. Global Systemically […]