The Latest RFR First Initiative in Cross Currency Swaps

For my final blog of 2021, permit me a small amount of self indulgence. I will take a look at the Cross Currency Swaps markets and their reactions to the two waves of RFR First that we have had recently. It turns out I will always jump on any excuse to write about Cross Currency […]

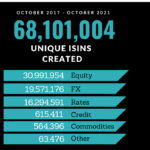

The $7 Trillion Increase in New RFR Positions

The RFR Adoption Indicator hit new all time highs in November of 26.3%. 45% of the USD Swaptions market is now traded versus SOFR on IDB SEFs. 100% of the GBP, JPY and CHF XCCY markets vs USD are now traded RFR vs RFR. We have seen a $7Trn+ increase in the Open Interest of […]

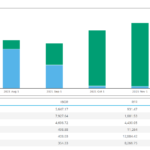

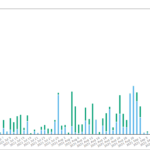

IR Futures Volume – Nov 2021

I last looked in detail at IR Futures volume in February 2021, so in this blog I will update the Average Daily Volume (ADV) and Open Interest (OI) of the major IR futures: Money Market and Bond Futures AUD, BRL, CAD, CHF, EUR, GBP, JPY and USD Relative size by ADV and OI on a […]

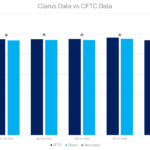

How Much of the Derivatives Market is Now Cleared? (2021 Edition)

83% of Interest Rate Derivatives are now cleared according to CFTC data. We use the CFTC data to benchmark our Clarus cleared data and find them to be in agreement. We therefore assume that the CFTC data for uncleared markets is also accurate, opening up more transparency into these important markets. We find that there […]

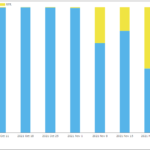

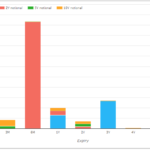

SOFR Swaptions – Month One Update

We recently covered SOFR Swaptions – Week One Update and SOFR First in Swaptions, and now that we have November volumes, I wanted to update what the data shows. November 2021 – SOFR Swaptions In SDRView Researcher, we select USD Swaptions and categorize by reference index as IBOR or RFR. Showing the jump to 29% of […]

What is a Consolidated Tape?

Following on from last week’s blog, I realised maybe I had jumped the gun somewhat. Since the European Commission has now published their report (and a Consolidated Tape for derivatives is included), I thought it worthwhile to take a step back. What actually is a Consolidated Tape and what that might mean for Transparency in […]

Consolidated Tape: Don’t let perfection be the enemy of good for derivatives

Dutch regulators have today stated with regards to European transparency data: Significant regulatory changes are needed to simplify the current fixed income post-trade deferral regime. Common data standards [are required], to set required data fields, and to agree on data access. Trading venues and APAs [need] to contribute the required data fields and supporting commercial […]

SOFR Swaptions – Week One Update

Last week we covered SOFR First in Swaptions and did so the day after the November 8th commencement date. Now that we have more data, let’s look at what this shows. Week One – SOFR Swaptions In SDRView Researcher, we select USD Swaptions and categorize by reference index as IBOR or RFR. Showing that in […]

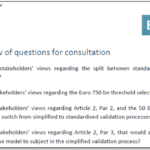

IM Model Validation for UMR under EMIR – Backtesting

Last week the EBA published a consultation paper on its its draft Regulatory Technical Standards (RTS) on Initial Margin Model Validation (IMMV) under the European Markets Infrastructure Regulation (EMIR). This is an important and long awaited publication, particularly for the hundreds of firms in the EU that are complying with UMR IM requirements as of Sep 2021 […]

SOFR First in Swaptions

This is not quite our normal “LIVE BLOG” type of announcement for SOFR First in Swaptions (and other non-linear derivatives). I tend to think that Options markets like to make things (unnecessarily?) complicated, and so there are a number of moving parts to look at for SOFR First in USD Swaptions. In Summary November 8th […]