This blog looks at Swap Connect, a service enabling offshore parties to trade and clear deliverable CNY swaps.

Key takeaways

- Swap Connect handled 6.4 percent of 2025 cleared CNY rates swaps volume. Without Swap Connect, that share may have gone to LCH SwapClear. Instead, it went to Shanghai Clearing House (SHCH).

- Swap Connect’s unusual clearing model involves two CCPs in clearing a single trade so as to allow an offshore party to trade an onshore market.

Read on for Swap Connect’s market impact and the unique features of its trade acceptance approach, booking model and margin process.

All the charts, data, and statistics in this blog were sourced from CCPView.

CNY swaps background

The CNY cleared swaps market is bifurcated into onshore and offshore components. Onshore, Shanghai Clearing House (SHCH) clears CNY deliverable interest rate swaps (DIRS), settling in CNY in China. Offshore, LCH SwapClear clears CNY non-deliverable interest rate swaps (NDIRS), which settle in USD in London.

The onshore component was spurred by the 2014 China clearing mandate. Offshore CNY NDIRS started life as an uncleared market until the implementation of regulators’ uncleared margin rules (UMR), whose first phase went live in September 2016. The opportunity to lower margin costs led participants to adopt LCH SwapClear’s 2018 launch of cleared CNY NDIRS. In 2025, 94 percent of CNY NDIRS are cleared.

For broader background on CNY swaps, I refer you to our March 2025 blog CNY Swaps – What’s New? and to our June 2020 blog What You Need to Know About CNY Swaps.

CNY swaps in the context of all currencies

We start with the long-range dynamic of CNY compared with other trading currencies.

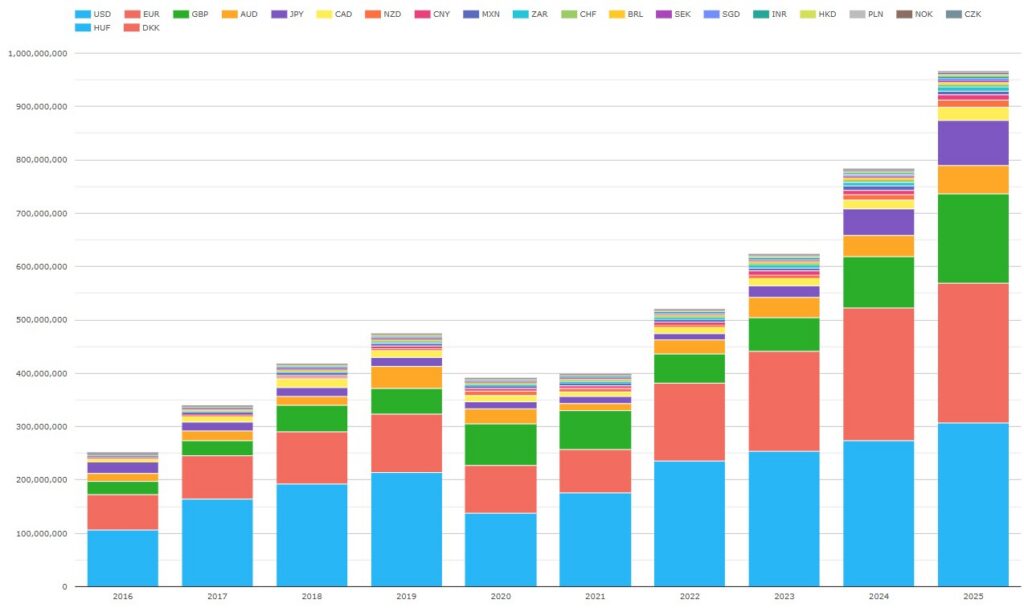

Chart 1: cleared core swaps volumes for selected currencies (notional USD millions). Source: CCPView.

Chart 1 includes core swaps (OIS, fixed float, basis and zero-coupon) for the 21 currencies that cleared above $100 billion in 2016. Collectively these currencies grew in volume by a multiple of 3.8 from 2016 to 2025. Over the same period, CNY grew by a multiple of 7.8, about twice as fast, to become the eighth largest currency by cleared swap volume, behind USD, EUR, JPY, GBP, AUD, CAD, and NZD.

From here onwards, we limit to CNY swaps.

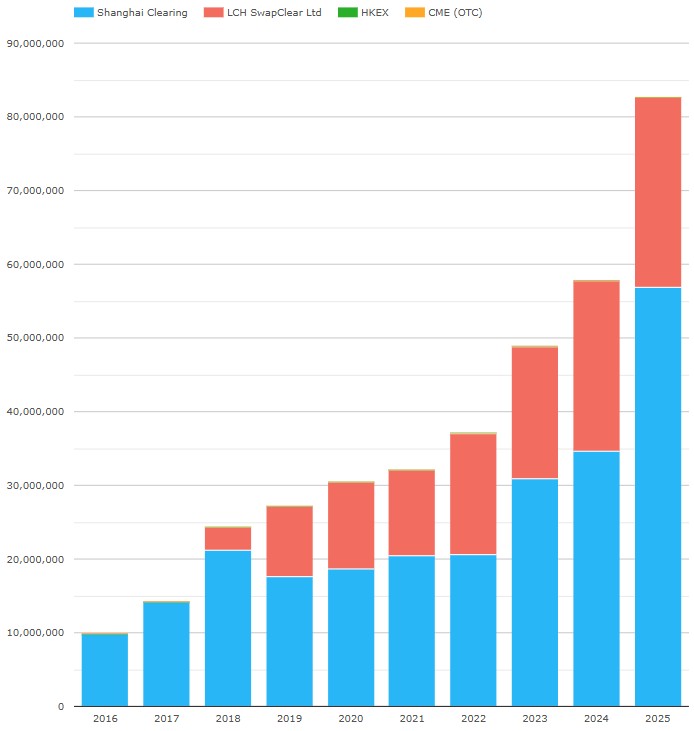

Chart 2: cleared CNY swaps by CCP (notional CNY millions). Source: CCPView.

Chart 2 shows 2025 cleared CNY swaps volumes were CNY 82.7 trillion – up 43 percent YoY.

- SHCH first cleared CNY DIRS in January 2014. In 2025, it had CNY 56.9 trillion – up 65 percent YoY.

- HKEX first cleared CNY IRS in October 2016, but volumes never became material.

- LCH first cleared CNY NDIRS on 30 April 2018. In 2025, it had CNY 25.8 trillion – up 10.9 percent YoY.

- CME first cleared CNY NDIRS on 31 July 2020, but volumes never became material.

Now we look at CCP market shares.

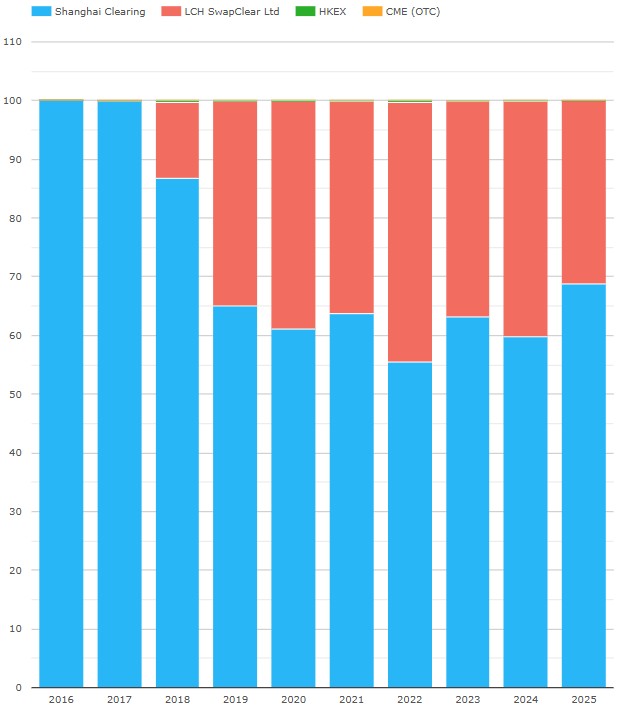

Chart 3: cleared CNY swaps share by CCP (notional CNY millions). Source: CCPView.

Chart 3 shows that SHCH experienced real competition for CNY swaps from LCH SwapClear. In 2025:

- SHCH grew its share to 68.8 percent – up from 55.5 percent, its lowest level in 2022.

- LCH had 31.2 percent – down from 44.2 percent, its peak in 2022.

- HKEX had 0.019 percent – down from 0.281 percent, its peak in 2022.

- CME peaked at 0.00594 percent in 2023 before declining to 0.00004 percent in 2025.

Compared with LCH’s peak in 2022, the last year before Swap Connect launched, SHCH took 13.3 percent from LCH in 2025.

Swap Connect

The Hong Kong Exchange (HKEX) Connect Program allows parties outside China to trade China’s onshore financial markets. The program initially focused on the Chinese equity and bond markets. Shanghai Stock Connect launched in 2014, Shenzhen Stock Connect in 2016, and Bond Connect in 2017. Stock Connect was expanded to include ETFs in 2019.

Swap Connect launched more recently, executing and clearing its first CNY swaps in May 2023. The interest rate swap product scope of Swap Connect comprises fixed float CNY DIRS on the following indexes:

- 7-day Repo (FR007).

- SHIBOR 3-Month (Shibor3M).

- SHIBOR Overnight (ShiborO/N).

- 1-year Loan Prime Rate (LPR1Y).

The Swap Connect service allows offshore parties to trade and clear onshore CNY DIRS on with onshore Chinese banks and dealers, without the need for an onshore Chinese trading entity or a direct clearing account or membership with SHCH.

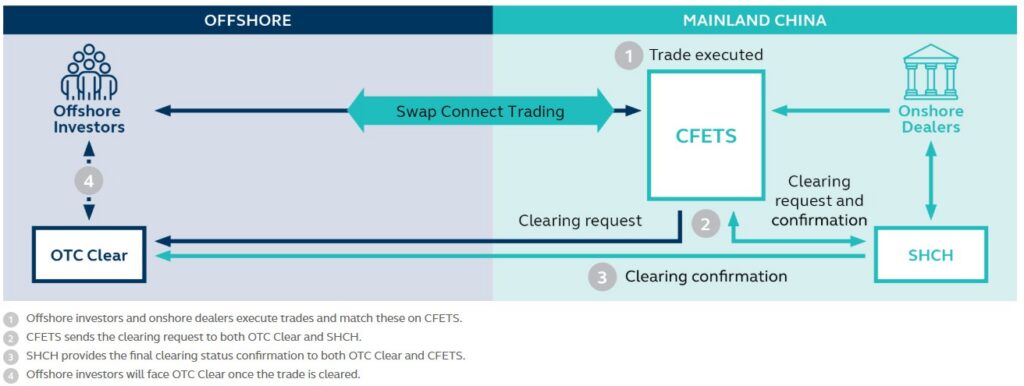

Swap Connect is a collaboration between OTC Clear (HKEX’s OTC derivatives CCP), SHCH, and the China Foreign Exchange Trade System (CFETS), an onshore China multilateral trading platform for CNY DIRS. Swap Connect trades avoid direct interactions between offshore parties and SHCH by having OTC Clear intermediate the cleared trade between SHCH and the offshore investor.

Figure 1: Swap Connect trading and clearing acceptance flow. Source: HKEX Swap Connect

The bullets underneath Figure 1 step through the depicted process of trade acceptance for a single CFETS-executed Swap Connect trade. Once cleared, novated, and intermediated, there would be four cleared trade sides booked in the two CCPs (rather than the usual two in one CCP). For example, suppose on a CNY DIRS the onshore dealer receives fixed rate interest from the offshore dealer, then the four sides would be:

- SHCH pays fixed to the onshore dealer (booked in the onshore party’s account at SHCH).

- SHCH receives fixed from OTC Clear on the inter-CCP trade, instead of from the offshore party (booked in an inter-CCP clearing account for OTC Clear at SHCH).

- OTC Clear pays fixed to SHCH on the inter-CCP trade (booked in an inter-CCP clearing account for SHCH at OTC Clear).

- OTC Clear, instead of SHCH, receives fixed from the offshore party (booked in the offshore party’s clearing account at OTC Clear).

A Swap Connect trade will always lead to a booking in each inter-CCP account, regardless of the offshore party or onshore dealer on the original trade. Hence, a large portfolio of trades will accumulate in both inter-CCP accounts, which operate like each CCP was a clearing member of the other. This means that OTC Clear settles net trade cash-flows, VM, and IM with SHCH according to SHCH rules and margin calculations, and vice versa. Cash flows and VM should be the same in both CCPs’ calculations and will settle via a single net cash payment per day in one direction or the other. Inter-CCP IM requirements are asymmetric with each CCP requiring IM from the other.

OTC Clear recovers the total inter-CCP IM paid to SHCH from OTC Clear members with Swap Connect trades via something called “Participating Margin” (PM). PM is a kind of Swap Connect IM surcharge on OTC Clear members, which may well be calculated in proportion to their Swap Connect trade exposures as a fraction of the gross total of all member’s Swap Connect exposures.

Setup required

Offshore parties wanting to trade Swap Connect trades do not require either a Chinese trading entity or a SHCH clearing account. OTC Clear collateral eligibility includes USD/EUR cash and US government bonds as well as HKD/RMB and HK/China government bonds. However, offshore parties still need:

- A CFETS trading agreement.

- An OTC Clear clearing agreement.

- The ability to settle RMB cash at OTC Clear.

- The ability to process PM within their margin processing.

Swap Connect volumes and market share impact

In CCPView, we represented Swap Connect as the exchange “SwapConnect” within the CCP “Shanghai Clearing”, while keeping the total of SwapConnect and OTC exchanges within SHCH the same.

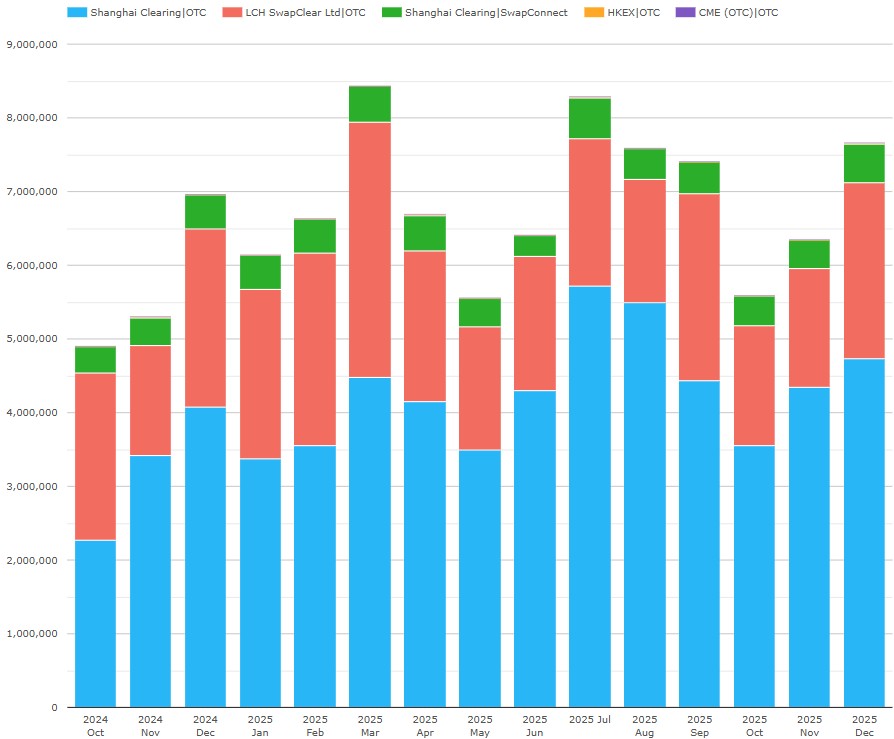

Chart 4: Month-by-month cleared CNY swap volumes (notional CNY millions). Source: CCPView

Chart 4 shows December 2025 global cleared CNY swap volumes totaled CNY 7.65 trillion – up 9.9 percent YoY. Of this:

- SHCH OTC (non-Swap Connect trades) saw 4.74 trillion RMB – up 16.4 percent YoY.

- LCH SwapClear reported 2.38 trillion RMB – down 1.8 percent YoY.

- SHCH Swap Connect had 532 billion RMB – up 14.0 percent YoY.

- HKEX OTC Clear (non-Swap Connect trades) showed 780 million RMB – down 43 percent YoY.

- CME had zero volume.

Now we move on to full-year market shares.

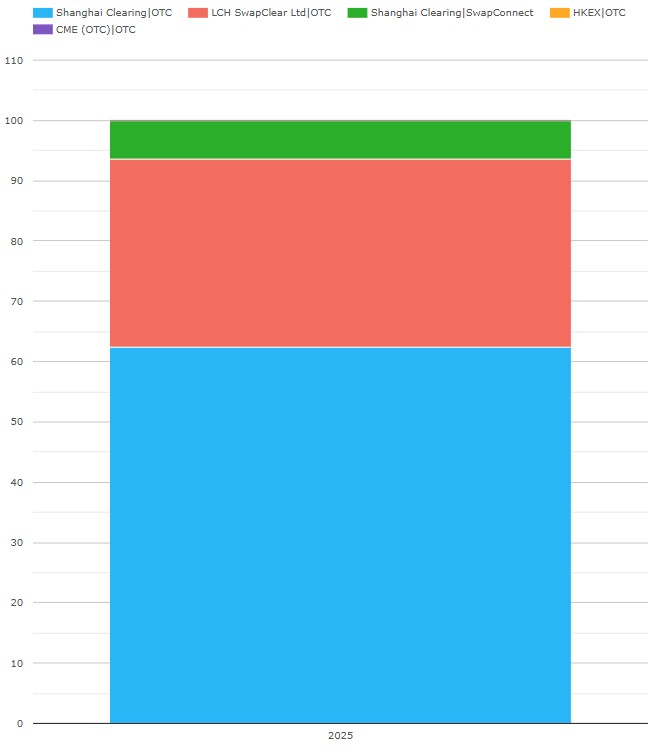

Chart 5: CCP shares of CNY swap volumes (notional CNY millions). Source: CCPView

Chart 5 shows that SHCH Swap Connect trades had a 6.4 percent share of cleared CNY swaps volumes in 2025, the first full year of publicly available volumes. Without Swap Connect, LCH may have taken that 6.4 percent. This would have limited SHCH’s market share pick-up from 2022 to 2025 to 6.9 percent instead of 13.3 percent.

As well as a shift from LCH to SHCH, the 6.4 percent is also a shift in market making share from offshore market makers (US and European banks) to onshore market makers (Chinese banks).

Competitive factors

Two factors may help LCH SwapClear maintain a solid CNY swaps share:

- The cross-currency offsets in the SwapClear IM model may enable parties with substantial major currency swap portfolios at SwapClear to incur lower IM costs to clear CNY swaps at SwapClear than via Swap Connect.

- It is not clear to me whether offshore buy-side firms can use Swap Connect / trade on CFETS. If not, they will continue to trade CNY NDIRS uncleared or cleared at LCH SwapClear and traded on Tradeweb or Bloomberg.

Time will tell where these market shares will settle down.

End note

Skip back to the top to reread the key takeaways if you like.

You can find a lot more data in CCPView. Click the link to see a summary of the range of data available.

Contact us if you are interested in a subscription.