This is my final blog for the year, but the 2023 retrospectives will have to wait for January once all of the data is in.

However, as the year draws to a close, I doubt 2023 will be remembered as the year that USD LIBOR finally ceased. That has to be considered a good thing. Nothing (systemic) went wrong, and IRD volumes remain huge post-cessation. Cessation was a non-event on the markets side, although I doubt project teams who gave up numerous weekends would agree!

Cessation does mean that there is now a huge legacy book of “fallenback” trades out there. I wonder how many trading relationships really have the desire to run those until maturity? That could be one to monitor in 2024, but predictions in this space have been famously wrong. I certainly never expected so much Fed Funds trading after LIBOR transition.

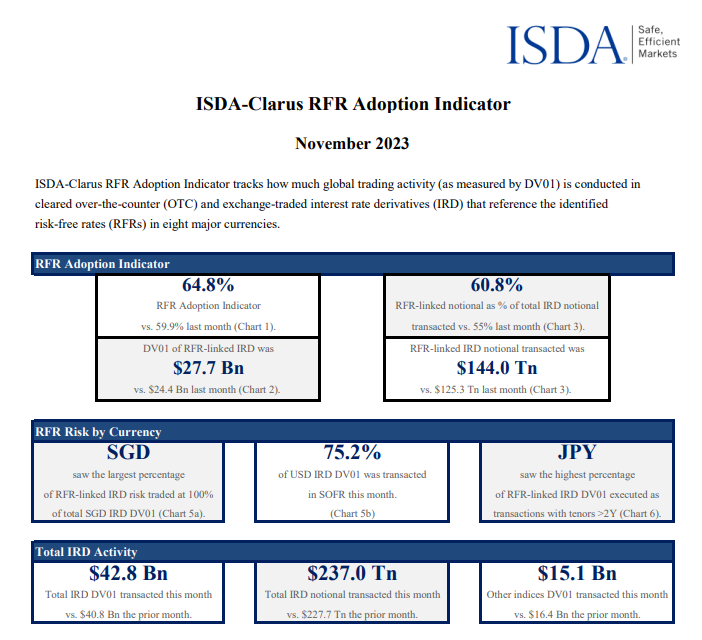

November 2023 – Big Increases But Falling Short of New All Time Highs

ISDA has now published the November 2023 review of RFR Adoption. In summary;

Showing;

- RFR Adoption up to 64.8%, nearly 5% higher than last month but still falling short of the 66.1% August high.

- SOFR adoption up 7% (!) in the month to 75.2%, just shy of the 76.2% August high.

- Total risk traded was large at $42.8bn of activity. That makes 2023 the most active year to the end of November that we have seen since the time-series began back in 2018 (yes, we’ve really been doing this that long!).

- It looks like 2023 will have been about 10% more active than last year. Maybe some of that is from the huge spike in activity in March associated with conversion exercises, but it is still a reassuringly large amount of risk being traded.

- In notional terms, November 2023 was the second largest month for RFR notional to have traded, and the largest outside of a conversion month.

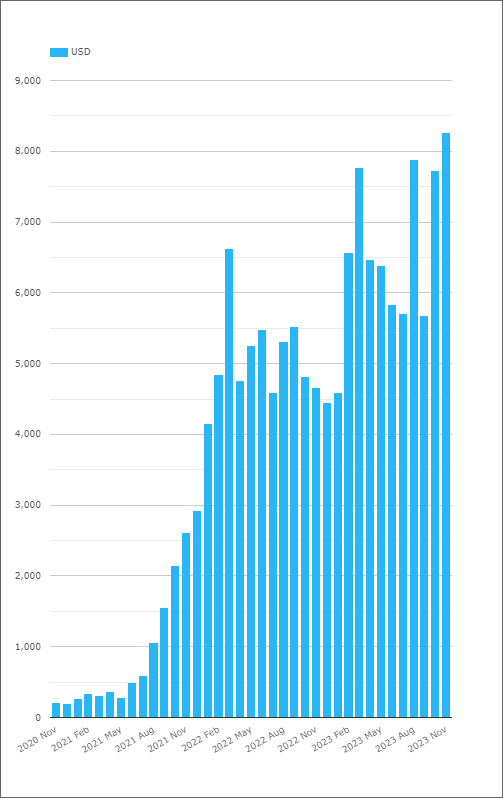

Size Matters

The SOFR market is now a beast. No matter how you cut it, November 2023 was a big month for SOFR risk. Remember this was before the recent Fed meeting and the repositioning around Rate cuts next year.

The total amount of SOFR risk traded in Swap markets was a record in November 2023, as measured by both DV01 and notional amounts:

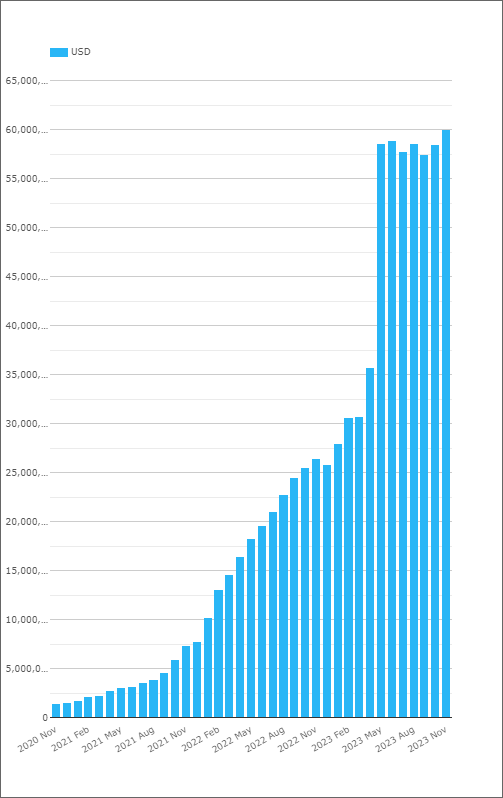

That has resulted in a record amount of Notional Outstanding in SOFR – this will likely decrease again into year-end as GSIBs reduce their gross notionals for balance sheet dressing:

Similarly, outside of a conversion month, SOFR Futures saw the largest amounts of risk ever traded. It all leaves me wondering whether such volumes can really be repeated in 2024? The market is setting a very high bar for “base levels” of SOFR activity here!

Why Has The European RFR Group Disbanded?

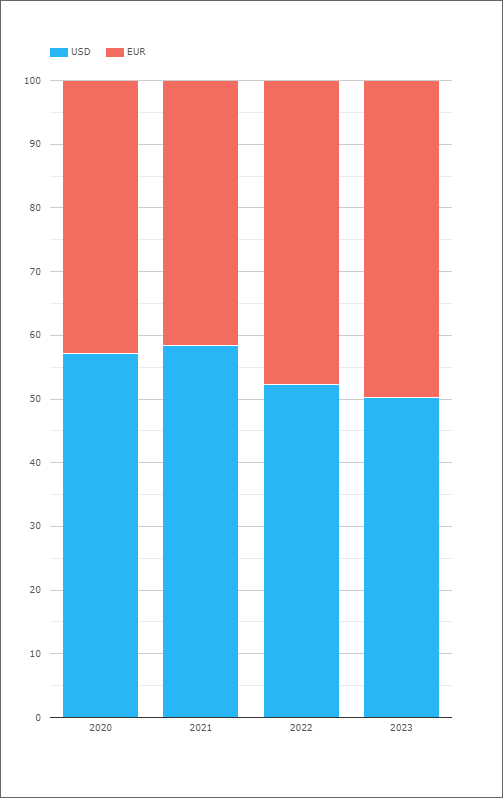

You may have noticed in my last blog that the European RFR Working Group is no longer. It appears that it was working to a much narrower remit than other RFR groups – namely to establish €STR as the successor to EONIA rather than replace derivatives trading in EURIBOR with the RFR.

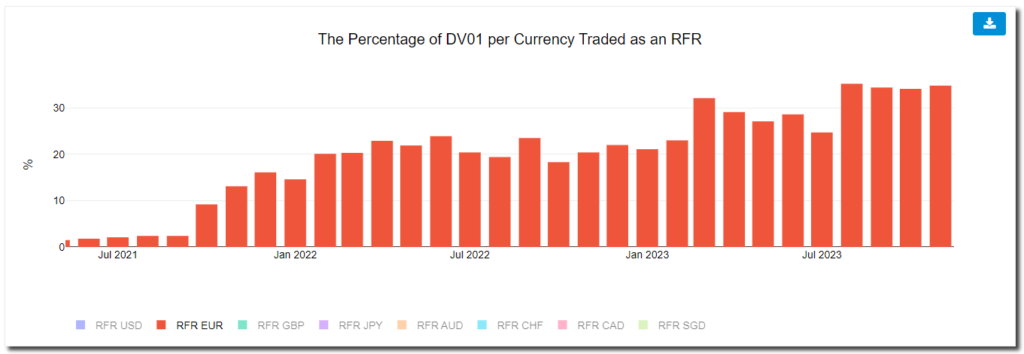

As such, it is hard to envision a meaningful change in €STR trading going forward. EUR Swap markets have grown relative to USD Swap markets in 2023, largely as a result of operating in a multi-index environment (despite such large activity in Fed Funds!):

This relative growth of EUR Swap markets is a particularly interesting one in light of the Active Account Requirement in Europe, and one that will no doubt feature heavily on the blog next year. Don’t forget to:

Read the blog for the latest on European plans to move a portion of the EUR IRD market to Europe:

Take a look at the data for €STR Adoption at rfr.clarusft.com. We have a lot of data over there:

Subscribe to the podcast which will also be covering Europe in-depth over the coming months:

In Summary

- RFR Adoption is no longer making headlines but the data remains really interesting.

- It provides insights into what is happening across Rates markets.

- We find that the SOFR market is larger and healthier than we ever expected…

- …and that the EUR swaps market has grown relative to the USD market since LIBOR cessation.

That just leaves me to say THANK YOU to all of our subscribers, readers and listeners for your support this year. I wish you a very happy festive period, a prosperous New Year and I look forward to being back in 2024.