Amongst the many questions that standout from the huge losses suffered by prime brokers in closing out the positions of Archegos Capital Management, the two that interest me most are, first the lack of transparency of the derivatives (total return swaps) used for these positions and second the in-adequate risk management by the prime brokers.

Trade Repositories

Transparency of OTC derivatives has been a major reform following the Great Financial Crisis of 2007-8 and is now implemented in all jurisdictions. Under the Dodd-Frank Act in the US, CFTC regulated trade repositories (SDRs, swap-data repositories) were implemented in 2012 and require all OTC derivative trades conducted by US persons to be reported and publicly disseminated (execution time, product, size, price, …) as soon as technically possible; generally within one to two minutes of execution time for the vast majority of trades.

Under the Dodd-Frank Act, the SEC was given authority over “security-based-swaps” which include total return swaps (TRS) on equities (but not equity indices) and credit default swaps on single-names (but not credit indices) and the associated trade repositories known as security-based swap data repositories (SBSDRs) have yet to be implemented.

Surprising as it sounds, 9 years after the CFTC SDRs were implemented and have become an important part of derivatives market infrastructure that participants rely upon, we are still waiting for SBSDRs.

SBSDR

The specific reasons for the delay in implementation of SBSDRs are not obvious; it certainly is not due to law, as the Dodd-Frank Act was in-place, so I can only assume SBSDRs suffered either from not being prioritized sufficiently , or ran into difficulties in implementation (e.g. acceptable costs to implement) or suffered from a lack of political will. The SEC page on SBSDRs sheds some light on the history:

- A Final Rule was adopted in Feb 2015

- Temporary exemption to the earlier of June 2016 or registration of an SBSDR

- Apr and Jun 2016 applications from ICE Trade Vault and DTCC to register SBSDRs

- Sep 2016, a further temporary exemption until April 2017, due to the compliance date not providing sufficient time for consideration of the comments received on the applications and any possible amendments

- Aug 2017, amended filings from DTCC and ICE

- Mar 2018, withdrawal letters from DTCC and ICE

- Feb 2021, a new application to register from DTCC

- Mar 2021, a new application to register from ICE

Phew, a lot going on there, I can imagine a ducks feet madly paddling, while nothing happens on the surface and the timeline above does lend credence to my assumption of “difficulties in implementation” .

The one fact that argues against that is the change in political leadership in Jan 2021, which in the US flows down from the administration into the federal agencies. With Gary Gensler confirmed as SEC Chair, it is no surprise that we see a SEC press release on May 7, announcing approval of DTCC registration and Nov 8, 2021 as the compliance date. This after all is the man who as CFTC chairman from 2009 to 2014, oversaw the implementation of SDRs registered under CFTC jurisdiction.

On a personal note, I have a clear recollection of a SEFCON event in NYC, most likely in early 2013, where Clarus had an exhibition stand and I had the opportunity to demonstrate our SDRView application to Chairman Gensler. I expect it was satisfying for him and his staff to see a tangible implementation and real world use of transparency in OTC Derivatives.

Would SBSDRs have helped?

The $10 billion question is, if SBSDRs had been in-place would regulators or the prime brokers been able to see the build up in risk exposure by Archegos in-time to take mitigating actions and avoid losses?

It is hard to give a categoric answer to this question.

Certainly one would expect that after the event, regulators would have had the data to be able to piece together the puzzle by specifically looking for total return swaps done by Archegos or simply all trades on the stocks reported to be the cause of the large losses i.e. ViacomCBS, Discovery, and others.

Whether they could have done this before the event, say in February or early March is a much harder question.

Given the likely massive amount of data, the fast moving nature of price volatility in the underlying stocks and the amount of resources available to the SEC, it would have been difficult to spot areas of concern and then decide to raise queries with regulated entities (prime brokers or executing brokers/dealers).

However public dissemination of these total return swaps would have been a different matter.

Had these trades been published, it is more likely that out of the thousands of firms active in US equity markets, some would have spotted out-sized or large numbers of total return swaps on the above mentioned stocks. This information as gossip, market color or press coverage would have made it to the prime brokers, who would have been armed with information on possible excessive concentration of trading in specific stocks and could have asked searching questions of Archegos.

Of-course hindsight is a wonderful thing and we will never really know the answer to these questions, however having the data available in SBSDRs, whether private data for a regulator or public anonymous data, could certainly have helped identify the potential build up of concentration risk on specific stocks. This concentration risk seems to have been the key missing information as TRS are exempt from stock and derivative position filings on SEF Form 13F, which themselves are due 45 days after quarter end.

The much more timely (intra-day) and granular (transaction level) SBSDR data would be a much better information source and certainly one that regulators and risk managers would have liked to have in place prior to 2021.

Prime Broker Margins

Transparency on possible highly concentrated positions that Archegoes held is one thing, the other is how much initial margin prime brokers required for these positions.

Archegoes was not large enough to be subject to phase 5 of the uncleared margin rules for OTC derivatives which come into force in Sep 2021, as these are for firms with > $50 billion notional in derivatives, so it would have been margined by each prime brokerage using in-house margin methodologies. I don’t have insight into the specific methodologies used by each of the prime brokers, but no doubt they consisted of one or more of the following:

- a risk based methodology such as Value-at-risk and/or Stress-testing

- rules of the road methodology, e.g. empirical rates and aggregations built up with experience

- dynamic or adhoc adjustments to account for higher price volatility

- adjustments to account for concentration risk of outsized positions or illiquid stocks

- static or dynamic haircuts on collateral held and eligible

Given the huge variation of losses between the prime brokerages reported by the FT on April 21 (table reproduced below), there is bound to be scrutiny of the margin held by each broker and actions taken to close out the positions.

There is speculation in the press that some firms such as Morgan Stanley and Goldman Sachs acted faster to close out their positions and so minimized losses, as well as that some firms gave materially higher leverage/lower margin levels than others.

While the PB margin models in question are not public, we can consider the hypothetical scenario that had Archegoes been subject to UMR and used ISDA SIMM, would the initial margin have been adequate to negate or significantly reduce the above losses.

UMR and ISDA SIMM

To do so, we need to quantify how the ISDA SIMM methodology would margin a TRS position and how this margin would increase for high concentration risk.

The main risk factor in an equity TRS is the delta risk to the underlying stock which drives the SIMM amount using the applicable risk weight and an adjustment for a concentration threshold.

As an example, lets take a TRS on 10,000 shares of Microsoft, we receive the return on the stock over a period, say 3M and pay an interest rate; for our purposes we will ignore the interest rate leg.

Assuming Microsoft stock is at $252.46, this makes the $ notional of this trade $2.5246 million and the Delta for a 1% move in the stock equal to $25,246. The appropriate SIMM Bucket is 8 (Large, Developed markets, technology) which has a risk weight of 24.

So multiplying $252.46 by 24, gives us $605,904 as the SIMM margin (or to be precise SIMM Margin for Equity risk, in-fact it would only be a little higher if IR risk was included).

Putting on a TRS trade on 10,000 Microsoft shares with a market value of $2.5 million, requires us to provide $606K of margin (24% or 4x leverage).

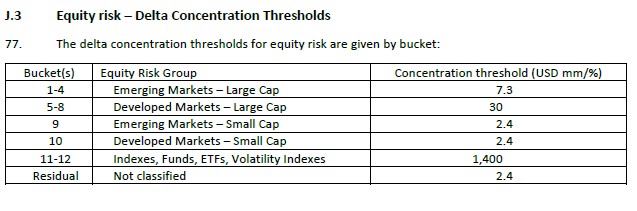

Concentration Risk Thresholds

And what happens if I create a massive position?

The following table kicks in:

So we need to exceed a Delta of $30 million for Developed Market – Large Cap stocks, where the latter is defined as >= $2 billion market cap.

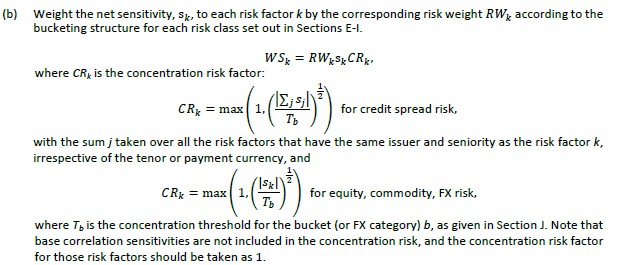

And the formula we need is:

So our Equity Delta divided by the concentration threshold, all to the power of 1/2 and only used this if this is greater than 1.

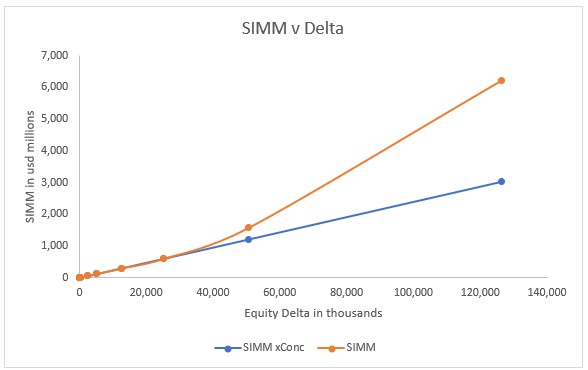

So for our Microsoft trade of 10,000 shares and delta of $25k there is no increase in SIMM due to concentration, but 12 million shares, $3 billion notional will have a Delta of just over $30 million. Plotting SIMM vs Delta in a chart, we see how SIMM increases for concentrated positions.

- A $50 million delta ($5b notional and 20m shares) would have SIMM of $1.6 billion instead of $1.2 billion without concentration risk

- A $126 million delta ($12.6b notional, 50m shares) a SIMM of $6.2b instead of $3b.

Microsoft has a market cap of $1.9 trillion and average daily volume of 27 million shares.

So it makes sense that 20m shares would be in concentration risk territory.

What about the positions held by Archegos?

- ViacomCBS, $38 share price, market cap $25 billion, daily volume 55m shares

- Discovery, $75 share price, market cap $17 billion, daily volume 95k shares

- Farfetch, $41 share price, market cap $14.7 billion, daily volume 8.6m shares

Each of these would be in SIMM buckets 5-8 with risk weights of between 20 and 28.

ViacomCBS fell from $100 on March 22 to $70 on March 24 and then to $48 on March 26, so over four days it lost 50%!

Even with a risk weight of 28, closing out the clients position on March 24, would have exhausted the initial margin held, resulting in a small loss. But waiting till March 26, which is when the forced selling of $20 billion by prime brokers was reported to have taken place, would have resulted in huge losses.

More worryingly, it does appear to me that while the concentration threshold of $30 million delta is appropriate for Microsoft, a mega-cap stock, it is far too high for the reported stocks held by Archegos.

Meaning that as phase 6 counterparties, many of whom will be hedge funds with directional or concentrated exposures as well as sophisticated strategies, become subject to UMR and SIMM, prime brokers should not just simply use the SIMM number for margin.

An assessment of client portfolios may well show the need for additional margin e.g. utilizing stock specific calibrations based on average daily volume data, instead of the SIMM concentration thresholds.

Real-world Portfolios

In reality actual portfolios, will contain TRS on many different equities and SIMM provides for correlations to aggregate the risk in an appropriate and conservative manner. In addition other equity products for example options or variance swaps on indices may also be present.

For such portfolios, the above simple exercise on paper or in Excel rapidly becomes too complex and our CHARM service (GUI or API) is what you really need to calculate SIMM and perform what-ifs. Please contact us if you would like to schedule a demonstration.

Clearing of TRS?

While we are on the topic of margin for bi-lateral TRS, it does seem pertinent to ask the question, would clearing be the answer?

After all underlying equity markets are cleared, as are equity options in the US.

And would this be done with the existing OTC product being novated into clearing?

Or the use of Total Return Futures?

Neither is a simple matter and a proper consideration requires an article in its own right.

Topics for another day.

Final Thoughts

Security-based SDRs will finally become active in the US on November 8, 2021.

The resulting transparency will benefit market structure.

It would have been useful in the lead up to the Archegos episode.

Uncleared margin rules for phase 5 & 6 will standardize and improve margin methods.

However over reliance on ISDA SIMM for all portfolios would not be wise.

Backtesting and calibration to account for specific portfolios is important.

Models are not a replacement for good judgement and sound risk management.