Released: A Julia library for Clarus Microservices

A Julia library has been developed and released to support Clarus Microservices. The library provides convenient access to Clarus Microservices. Source code is available on GitHub. In a previous blog, ‘Microservices: Swap Equivalents in Julia’ we showed that it was possible to call the Clarus API from Julia. We have generalised the code example in […]

Trade Validation: A simple version of FpML rule IRD12

Trade representations in CSV or FpML often have issues with stubs. FpML validation rule IRD12 has simple alternative for a wide range of cases. A form of FpML IRD12 can be represented in XPath for a wide range of cases. During proof-of-concept trials we are often asked to load up a prospects portfolio; either a […]

Array Formulas in Excel

We explain how to work with Array Formulas in Excel. Master the Three Finger Salute CTRL+SHIFT+ENTER. CTRL+/ is an amazingly effective shortcut. It is always easier to expand an array than shrink it. Consistent formatting provides an obvious visual cue when working with arrays. SIMM for Excel SIMM for Excel is an add-in that performs […]

Microservices: ISDA SIMM™ in R

The Clarus API has a function to compute ISDA SIMM™ from a CRIF file contain portfolio sensitivities. What-if analysis can be performed in addition to the portfolio margin calculation. The function is very easy to call from many popular languages, including R, Python, C++, Java and Julia. What is R? R is a language and […]

Bachelier Model: Fast Accurate Implied Volatility

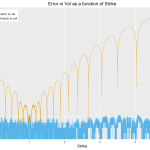

“An industrial solution” – provides computation to near machine precision for option prices over an extremely large range! Fast and analytic in nature, employs rational polynomials to determine implied BpVol. Follows the Bachelier model; that is, dF = σdW. A new method for computing implied BP Vol (basis point volatility) analytically has come to light. It is described by […]

Exploring Seasonality in a Time Series with R’s ggplot2

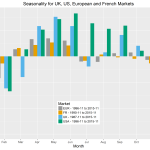

Inflation index values are decomposed into trend, seasonality and noise. Certain types of graph help identify seasonality. Graphs can be created simply and quickly in R. Simple graphs can be refined for stronger visual impact. Recently, I have been looking at inflation indices and studying their seasonality. The best way to see the overall trend and seasonality in this […]

Auto-detecting date format in CSV files

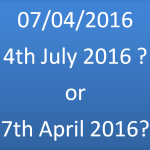

When uploading data into systems, comma separated value format (CSV) is a common choice. A difficulty can arise when editing CSV files in Excel — date formats can easily (and accidentally) change causing upload failures and end-user frustration. It is possible to write CSV uploading routines to automatically detect date formats and alleviate this problem […]

Data correction with fuzzy string matching

We are all familiar with Google’s “Did you mean” correction for misspelt search terms. But how does it work? There is a great chapter by Norvig in the book ‘Beautiful Data: The stories behind elegant data solutions’, that discusses and implements a basic spelling corrector, using only a few lines of python code. The chapter […]

Adapting to Direct Forward Curves

In interest rate pricing direct forward curves are defined on forward rates for a specific tenor as opposed to the more common discount factor representation, or the instantaneous forward curve representation. A simple example of a direct forward curve for 3M LIBOR would consist of a set of points and an interpolator, the points would […]

Quantitative Finance ‘GoodReads’

Two reading lists of books relevant to quantitative finance are provided using the GoodReads platform. Often I am asked to recommend good books to help a student, colleague or customer get a better grasp of quantitative finance. Instead of ad-hoc and incomplete lists, I thought it might be useful (especially for me) to have a […]