LIBOR Fallbacks and Uncleared Margin Rules

LIBOR fallbacks and Uncleared Margin Rules are hot topics across the industry. We highlight the Basel guidance that any amendments to LIBOR contracts as a result of Benchmark reform will not trigger the need to post margin. This is important guidance to ensure the uptake of new RFRs is simple. Two of our big blog […]

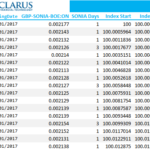

SONIA and SOFR trading and Term Risk Free Rates

The use of Risk Free Rates (RFRs) such as SONIA and SOFR continues to grow. Volumes are increasing as described in recent Clarus blogs, see SOFR Volumes April 2019, SARON Activity and Growth in RFR Markets. But the development of a term market in RFRs is still in it’s early stages. Clearing House data shows […]

LIBOR Fallbacks Again

ISDA has launched a second consultation on LIBOR fallbacks. This extends the number of benchmarks covered to eight currencies. The big one this time is USD LIBOR, which is interesting because USD SOFR has a limited history available. Fortunately, the New York Fed has made a proxy USD repo rate available back to 1998. 78% […]

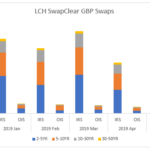

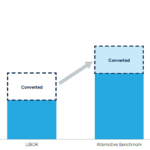

Portfolio Conversion of Libor to RFR trades

The closer we get to year end 2021, the more important the question of what will happen to existing LIBOR Swaps when and if LIBOR is no longer published or declared a non-compliant benchmark by the regulator. One approach is ISDA’s work on new Fallback language in the 2006 Definitions (see Libor Fallbacks: What will […]

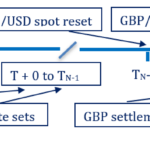

Potential Mechanics of Cross Currency Swaps and RFRs

As references to Libor declines ahead of 2021 and the use of Risk Free Rates (RFRs) increases, derivatives will have to adapt. So in this blog I will look at the cross-currency swaps and the choices needed to move to RFRs. Cross currency swaps can behave quite differently to single currency swaps and I will […]

USD SOFR Volumes April 2019

Is USD SOFR trading becoming a real thing now? We use CCPView, SDRView and Clarus Microservices to measure activity levels. We find a record amount of risk traded in April 2019 versus SOFR. We also see Compression activity of back-dated trades in SOFR. Read on to find out more details. SOFR Volumes April 2019 You […]

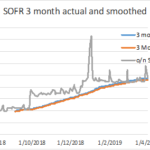

SOFR Impacts From Liquidity Spikes

The Clarus website has a very interesting free service under the LOGIN tab called ‘Term RFRs’. This shows the compounded RFRs for the fixing date (yesterday) looking back overnight, 1, 2, 3 and 6 months for SOFR (USD), SONIA (GBP), TONA (JPY) and AONIA (AUD). This blog will look at the compounded SOFR rates for […]

Indices are the best way to calculate compound interest

To avoid complications with compound interest calculations, administrators of RFRs could publish a single Index each day. The equivalent term rate for any period could then be calculated by looking up the index level from the start date and the end date of each period. Interim rates do not need to be known. This allows […]

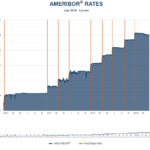

Ameribor: The $1.5bn Index That You Need to Know About

Ameribor is an index of overnight unsecured lending taking place across the CBOE platform AFX. It is mainly concerned with the interbank market between smaller, regional US banks. We take a look at the rate versus Fed Funds and some possible uses. Introducing Ameribor I will try to do Ameribor justice in this post. But […]

NOK Rates – NIBOR and NOWA

I wrote about Scandie swaps in October 2018. In that blog I noted that OIS doesn’t really trade. This hasn’t changed in the interim period – SDRView shows just the occasional DKK OIS trade reported. We did, however, see some SEK OIS cleared at Nasdaq OMX in April via CCPView: Generally, it remains true to […]