- CDX block sizes will more than double in December 2023.

- FX block sizes will increase by many multiples (50x in some cases) under the newly calibrated levels.

- New block sizes in products that have a MAT determination will likely attract the most amount of attention….

- …but there may be consequences for non-MAT products as well, particularly in FX.

- The review process will be interesting to follow.

CFTC Global Markets Advisory Committee

Following up on my blog last week, there is now the recording of the CFTC’s Global Markets Advisory Committee (GMAC) available on youtube:

There are some interesting take-aways:

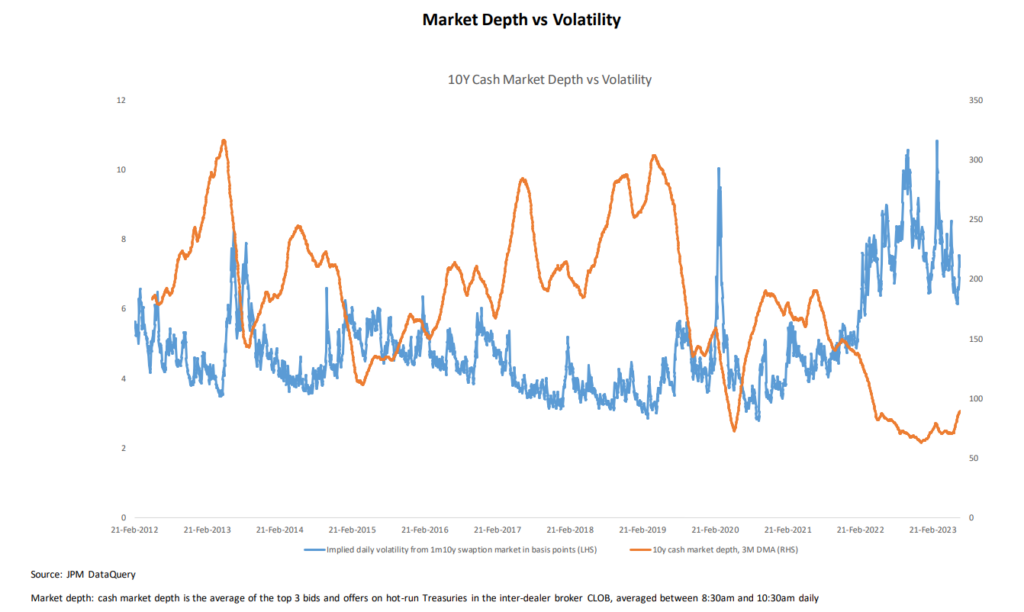

- The industry really needs to develop some type of standard measure of liquidity! Pimco highlighted that we are now in a “high vol, low liquidity” paradigm for the first time in ten years:

Showing;

- The implied volatility in 1m10Y USD swaptions (in blue) versus the market depth of 10Y cash treasuries (USTs) for the top three orders in central limit order books.

- The chart shows that market depth has been at the lows since 2022 whilst volatility has moved to higher levels.

- As we know from Clarus data, this typically means that the price of liquidity has increased.

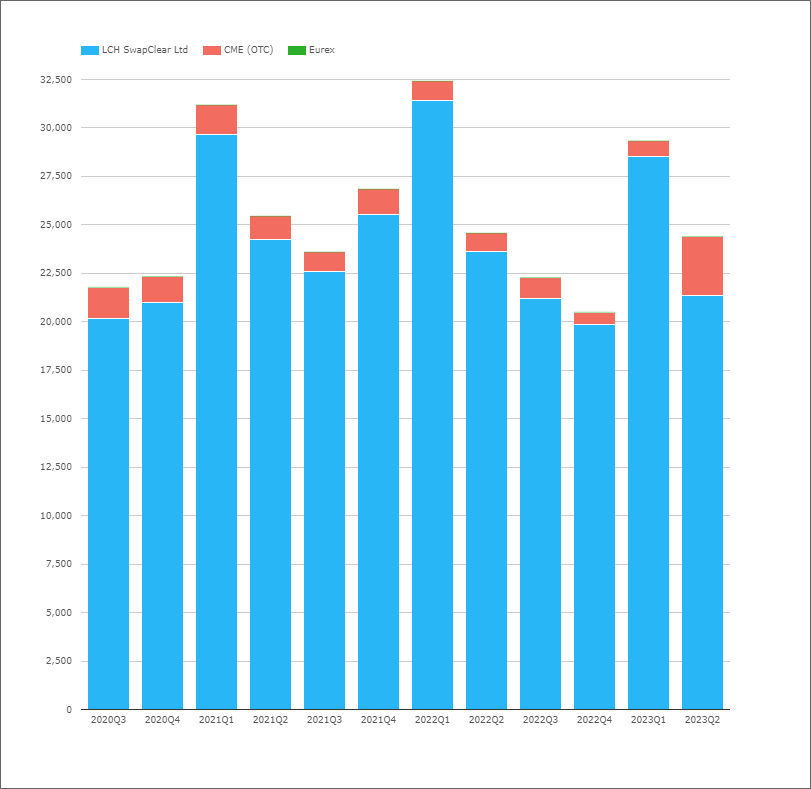

- There is still A LOT of volume transacting though! This is best shown by the rebound in volumes in USD swaps since Q4 2022 (in DV01 terms below):

- So liquidity might be more expensive but there are clearly plenty of people still willing to pay that price. (Does that equate to liquidity inflation or liquidity shrinkflation?).

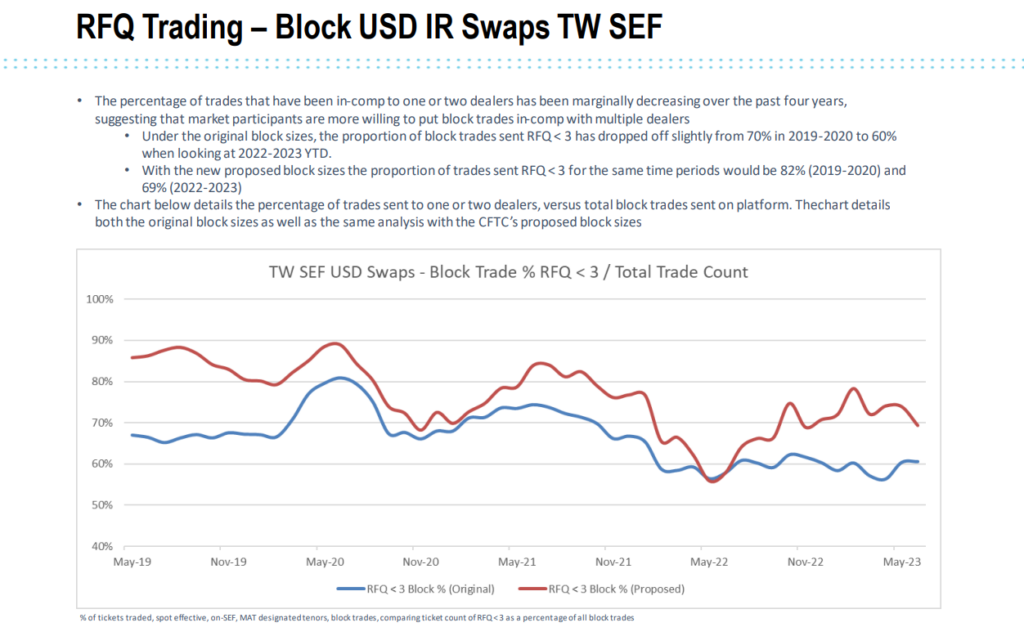

Elsewhere, Tradeweb and Bloomberg provided insights into the RFQ1 vs RFQ-to-many split amongst large trades. This is some really interesting data. The chart below shows that over 60% of block trades in USD IRS are sent to less than 3 dealers. With larger block sizes, over 70% (and even up to 90%!) of block trades would be sent to only 1 or 2 dealers:

(I assume that the 2022 & 23 data includes SOFR OIS, hence the reference to “MAT tenors” on the footnote).

- I would love to know what that chart looks like when trades are grouped 1x, 2x and 3x block size.

- I wonder if there is any evidence that trades are beginning to be broken down into smaller packages?

- The peak in RFQ-to-less-than-3 was around the March 2020 market turmoil – relationships matter in times of stress people!

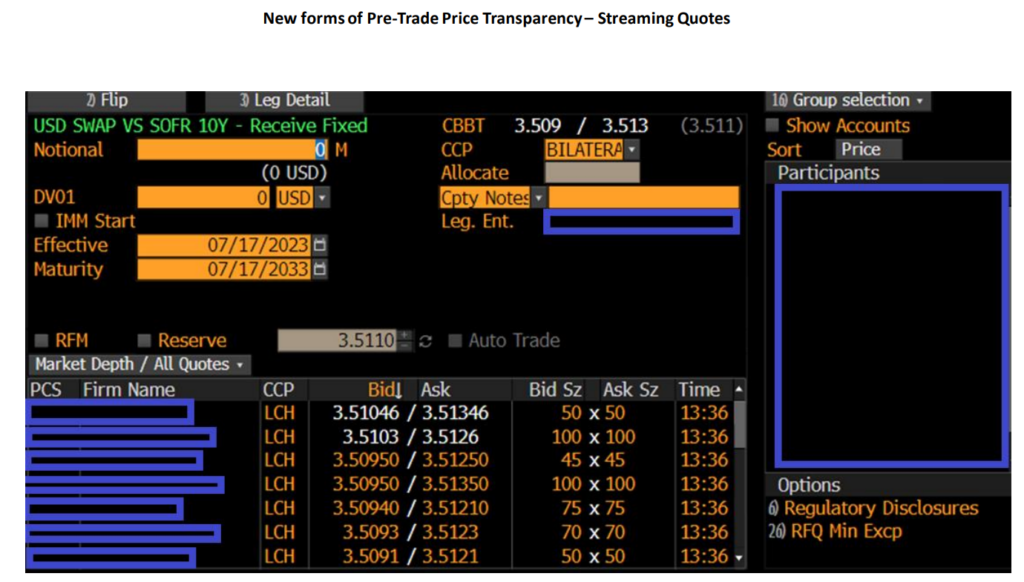

And for those of you without regular access to Bloomberg, you might be interested to witness the level of pre-trade transparency that SEFs have introduced. It is really impressive to have reached this level within ten years of SEF trading. And if anyone knows what the “Auto Trade” option that is greyed out below does, please let me know!

The take-aways from the GMAC were:

- ISDA stated that they have requested a one year delay for the new rules to come into effect. I personally think we have had more than enough time to prepare since I first blogged on this 3 years ago!

- Everyone who spoke supported “more investigation” into the proposed levels.

- Everyone was far too polite to speak about specifics, such as why do the block thresholds increase so much at longer maturities for USD swaps?

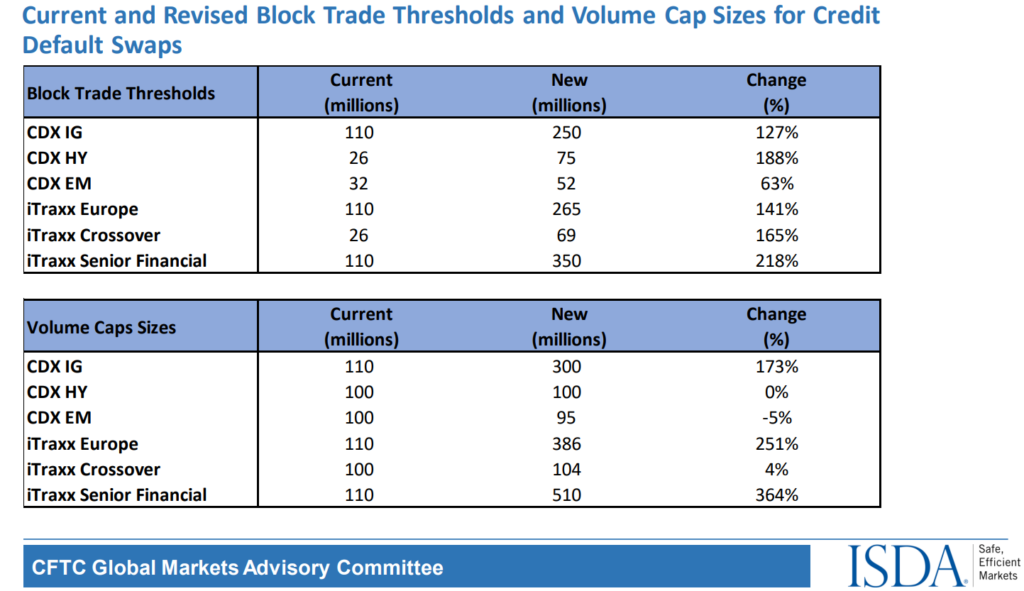

CDS Index Blocks

Happily, ISDA saved me a bit of Excel work this week! I will shamelessly copy their slide showing the block threshold changes for CDS Index trades (I am sure they won’t mind):

Showing;

- Block trade increases in CDS Index trades are much larger than for IRS.

- This was somewhat anticipated because 15-30% of trades each month are currently designated as “Block” in CDX reported to SDRs:

- This is higher than the 4-6% that are reported as Blocks and Capped trades for Rates products.

It will be interesting to see how these are received by the market – most of the attention has been on the Rates products so far, so I think it is well worth flagging here. Similarly….

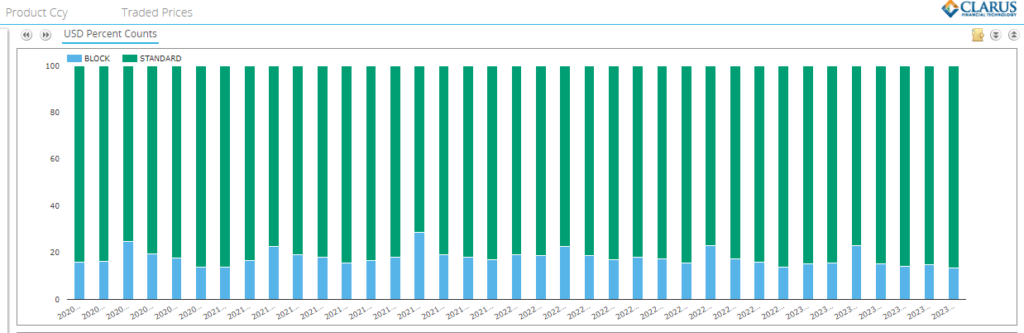

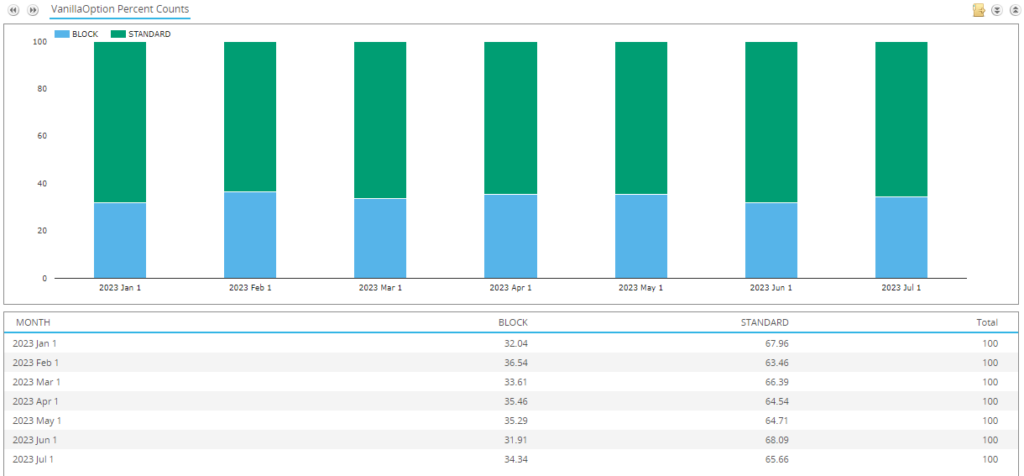

FX Block Sizes

For FX Options reported to SDRs, over 35% of trades are currently reported as blocks in the major currency pairs – EUR, GBP, JPY, AUD & CAD vs USD:

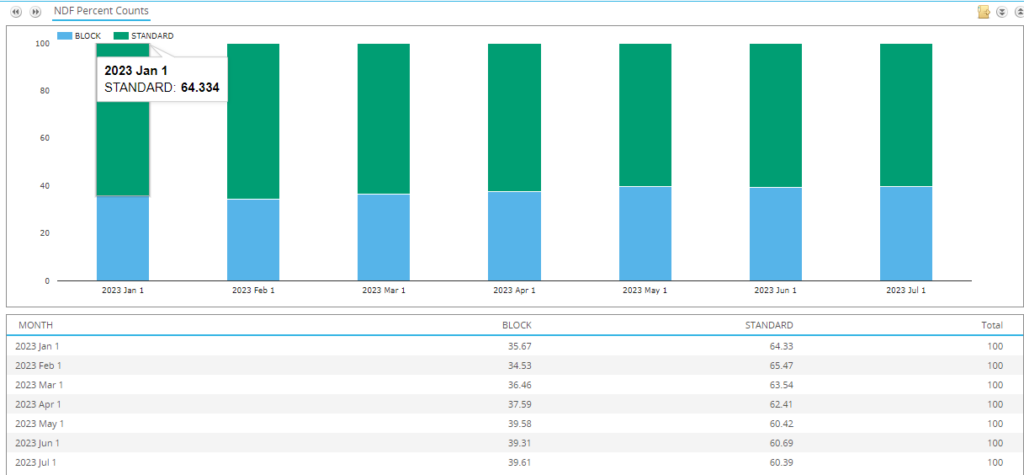

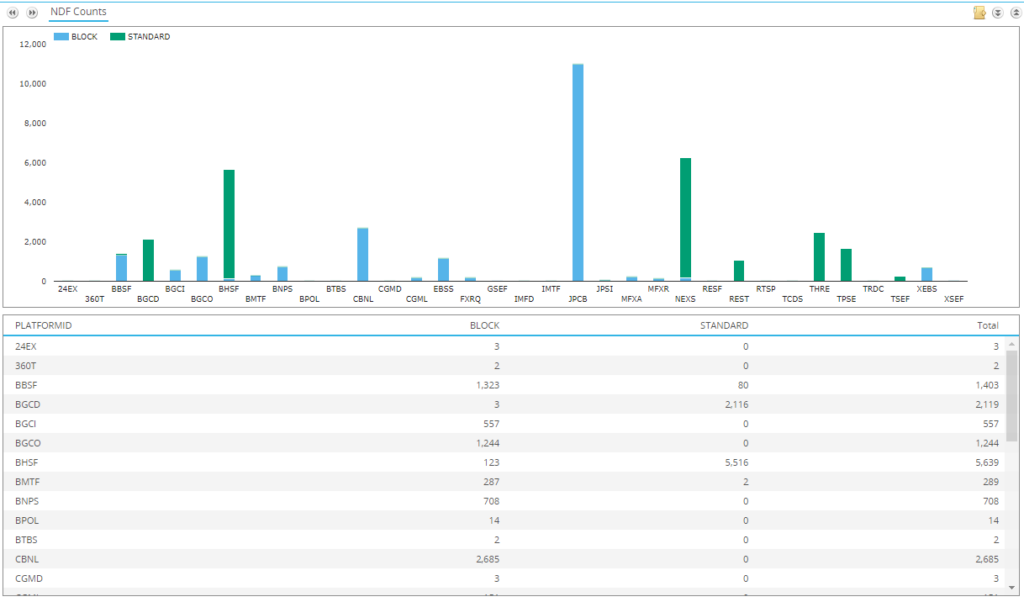

And for NDFs, the data is similar, if a little higher. In CNY, INR, KRW & BRL vs USD 40% of trades were reported as block trades in the past three months.

I believe that the high number of block trades in FX is intentional, because some currency pairs do not have any block limits set. Therefore, no matter what the size, any trade in INR or CNY can be treated as a block trade:

All swap transactions subject to part 43 in these unique currency combinations may be treated as

blocks. The changes to § 43.6(b)(4) will significantly reduce the number of swap categories.While not affording block treatment to all swaps in the FX asset class subject to part 43, these modifications will increase the number of currency combinations which will be eligible to be blocks, many of which have limited liquidity

CFTC, 17 CFR Part 43 Procedures To Establish Appropriate Minimum Block Sizes for Large

Notional Off-Facility Swaps and Block Trades; Final Rule

My understanding is that this means all FX trades in INR and CNY (for example) can be treated as Block trades, irrespective of size. And that is what we see in the data, where some platforms report all trades as block trades (data below for trades executed on-SEF in July 2023):

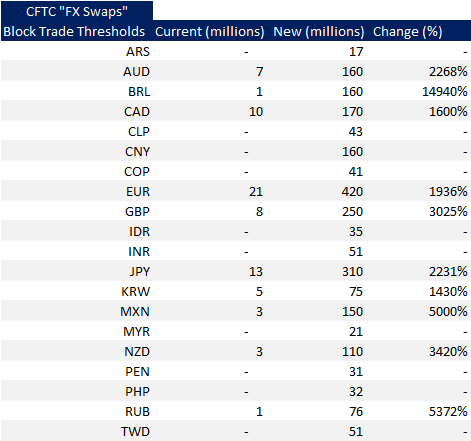

This is, therefore, the first time that FX block thresholds have been truly calibrated. It will be interesting to see how the review process goes because most of the changes are many multiples of current levels:

MAT Determinations and Clearing Mandates

Whilst the changes in FX block levels are eye-poppingly large, the impact on the industry may be different because there are no MAT determinations or Clearing Mandates in the FX Asset Class. However, it could have particular impacts on certain FX trading venues, who may have implemented minimum order sizes above the current block thresholds to simplify trade processing.

The review process will be interesting that’s for sure!

In Summary

- Block sizes are changing in all the asset classes – Rates, Credit and FX (and even Commodities).

- The existence of MAT determinations and Clearing Mandates will likely mean that the impacts are most keenly felt in Rates and Credit markets.

- However, this is the first time that block sizes have been calibrated using market data for FX swaps (NDFs and FX Options).

- This has resulted in some huge increases and will likely attract further comment from industry review.