Clarus were invited along to the CFTC’s Market Risk Advisory Committee on July 21st, for which we are very thankful. It was a great session, and we hope provided an opportunity to highlight to all market participants how vital transparency was to the smooth functioning of markets during March 2020.

We presented on “Rates OTC Derivatives Markets and COVID-19“, providing data-driven analysis of what happened in markets during March 2020.

The replay of the session is now available, please see below. The bulk of the Clarus session starts at 1h50mins:

Transparency Worked

In summary, we found that:

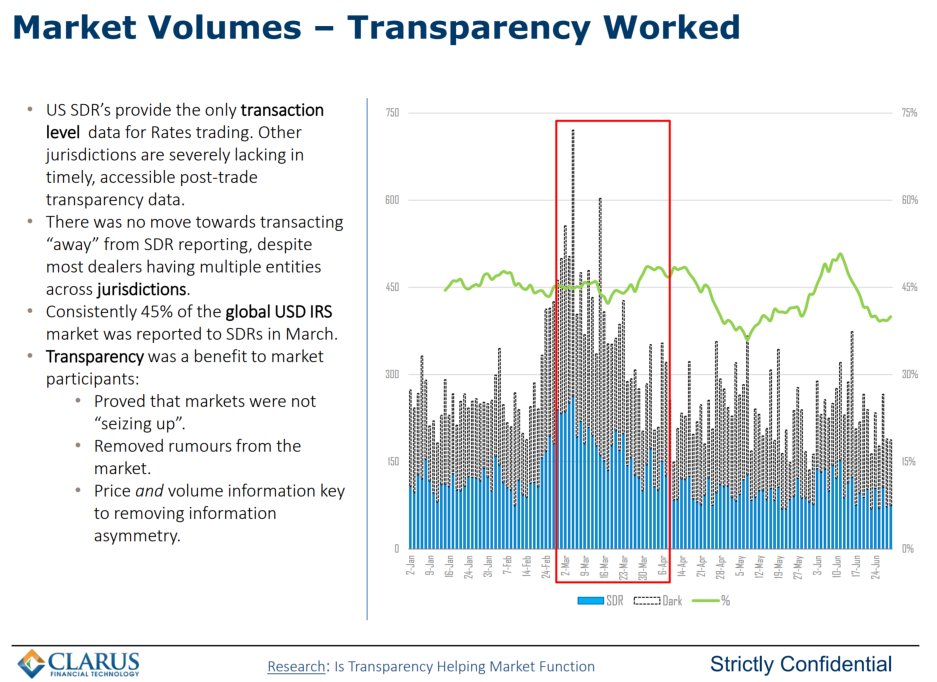

- Transparency worked. Post-trade reporting provided all market participants with clear evidence that derivatives market activity was continuing at pace.

- Volumes hit all-time records in Clearing during March 2020.

- Market participants continued to choose clearing over bilateral markets.

- SEFs had a “good crisis” with record volumes in USD IRS transacted on-SEF.

- D2C SEFs did particularly well (Tradeweb and Bloomberg).

- Block trading on D2C SEFs was also very successful. (Remember this conclusion is data driven, not anecdote-driven!).

- Pricing conditions, when we analyse Price Dispersion, were more difficult. This suggests that whilst liquidity was available (as evidenced by record volumes) it came at a price.

- Volumes in uncleared markets did not see the same records hit. This is puzzling, particularly in the case of Cross Currency Swaps and Swaptions. Hopefully more research can be done on this, as we need more transparency into this important area of the market.

You can read our whole presentation here, linked under the CFTC’s MRAC Event Page as “MRAC Clarus Financial Technology Presentation Chris Barnes July 2020“.

SEFs and CCPs

It was an interesting session. In particular, it was great to hear first hand from the SEFs and CCPs regarding their experiences of the market volatility.

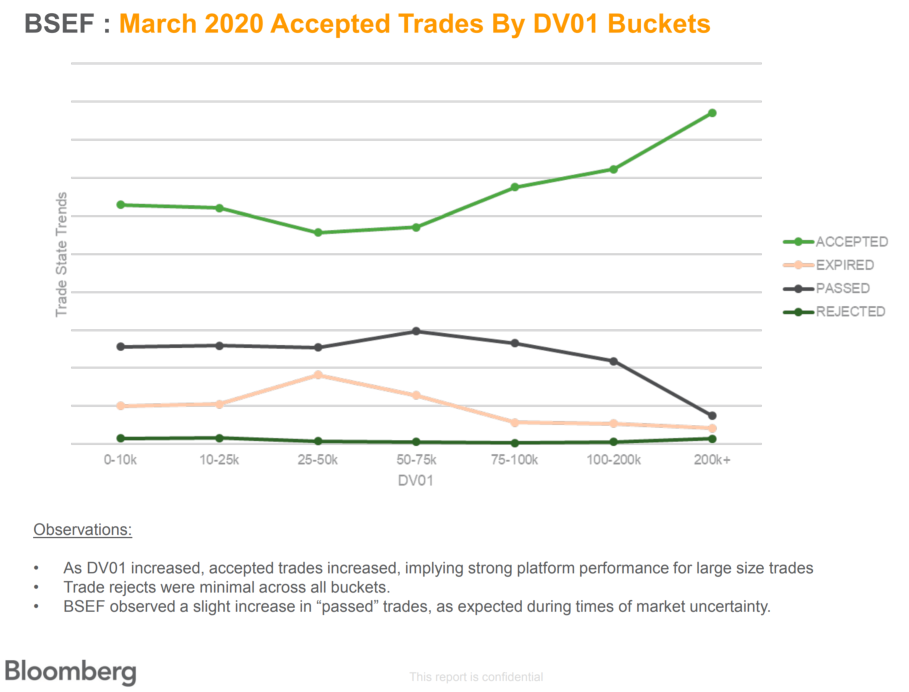

The SEFs have some fascinating data on hit ratios, RFQ acceptance rates and relative “performance” of execution by size. We would love to see more of that data made public, such as the below from BSEF:

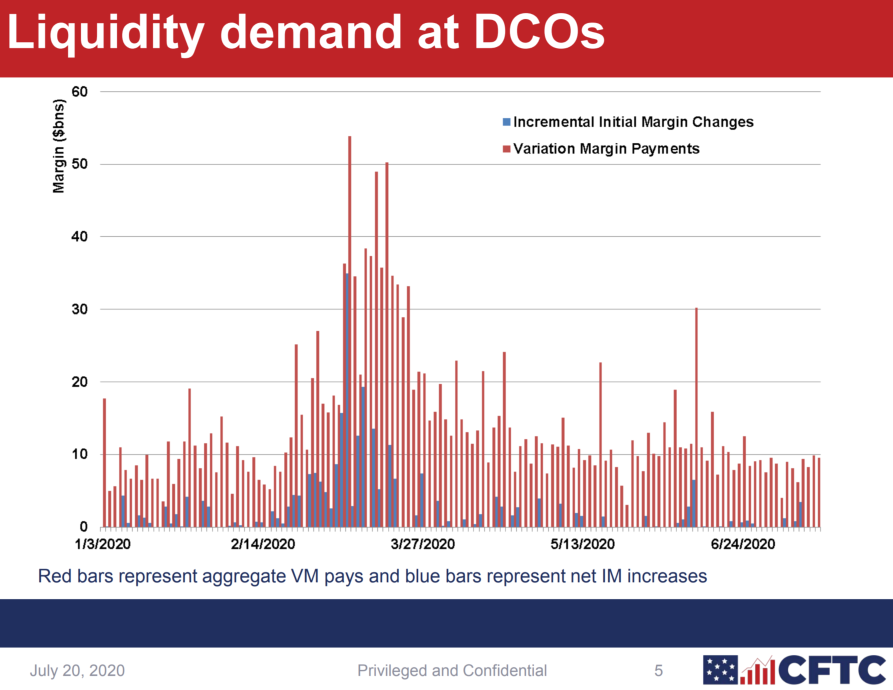

It was also interesting to see the CFTC highlighting the IM and VM liquidity calls that were made:

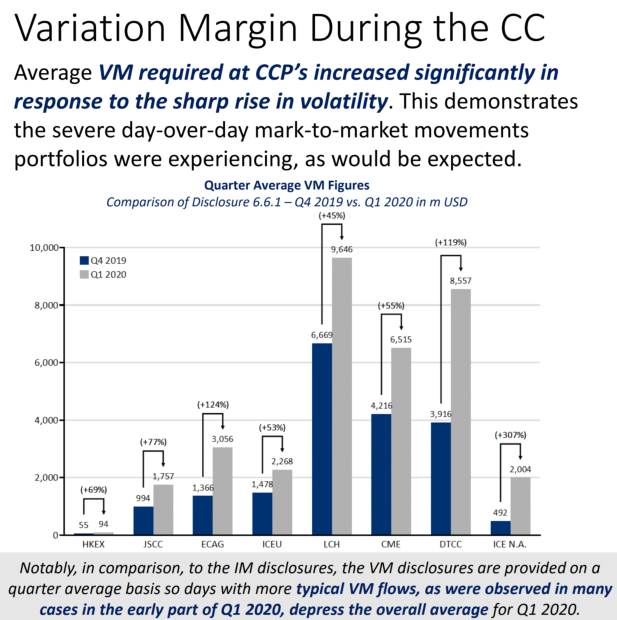

And the FIA and CME did a good job of highlighting how well the Clearing infrastructure performed, with particular reference to a recent CCP12 paper “CCPs again demonstrate strong resilience in times of crisis“:

In Summary

Thanks to transparency data, we know that markets continued to function well during the COVID-19-related market volatility. The market infrastructure was able to scale-up to hit record volumes, across both CCPs and SEFs.

The only blot on the landscape was uncleared markets, where the data shows surprisingly low volumes. We need more transparency into these important uncleared markets to understand why.

And many thanks to Commissioner Behnam for name checking us in his closing remarks (at 3hr52mins)!