In my recent post on the same topic, I outlined how deliverable currency FX NDFs are being used to reduce SIMM FX delta, as opposed to a product traded in the usual sense. In today’s article I show the data that underpins my view and consider if NDF delta compression will be a permanent feature or one superseded by more complete but complex solutions.

What does G10 NDF data show us?

To get at this we need to look at daily, not monthly or weekly volumes in SDRView, CCPView and SEFView.

1. US Reported (SDRView)

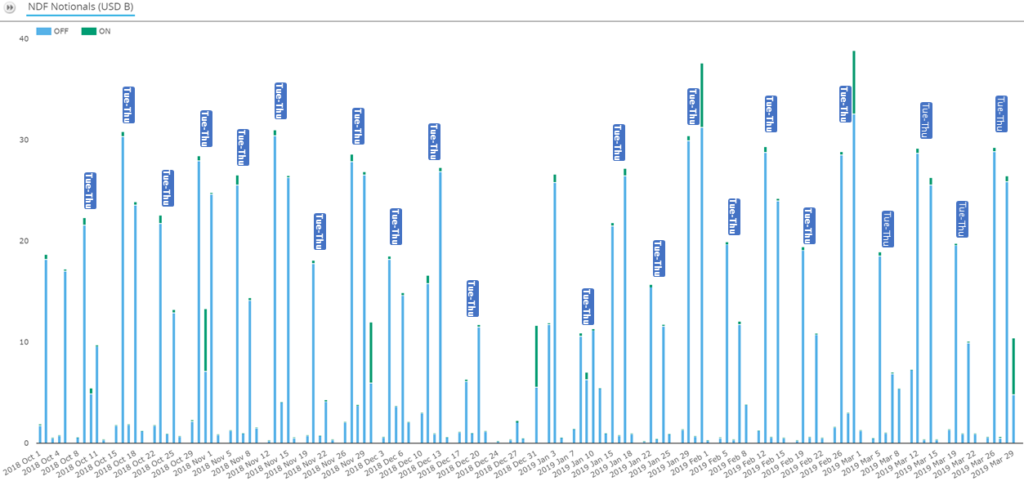

Using the last six months SDRView chart, I’ve highlighted below a repeating pattern.

To convince you further we can aggregate the volumes as follows:

Showing:

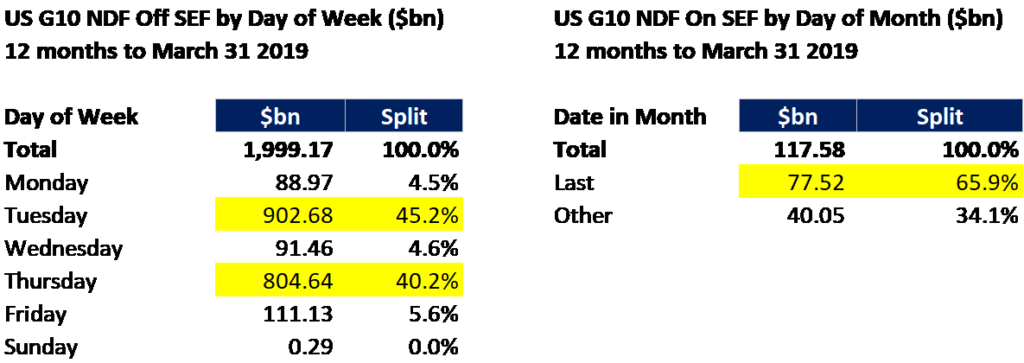

- Off SEF has a clear pattern with >85% of trades on Tues and Thus each week (marked with blue rectangles)

- The only break in the six months is over the end December holiday period

- On SEF has a visible >65% on monthly last working day pattern (see also the green bars in the top chart)

Observations:

- Regular traded markets don’t take three days off a week

- TriBalance runs every Thursday, which ties in with the data.

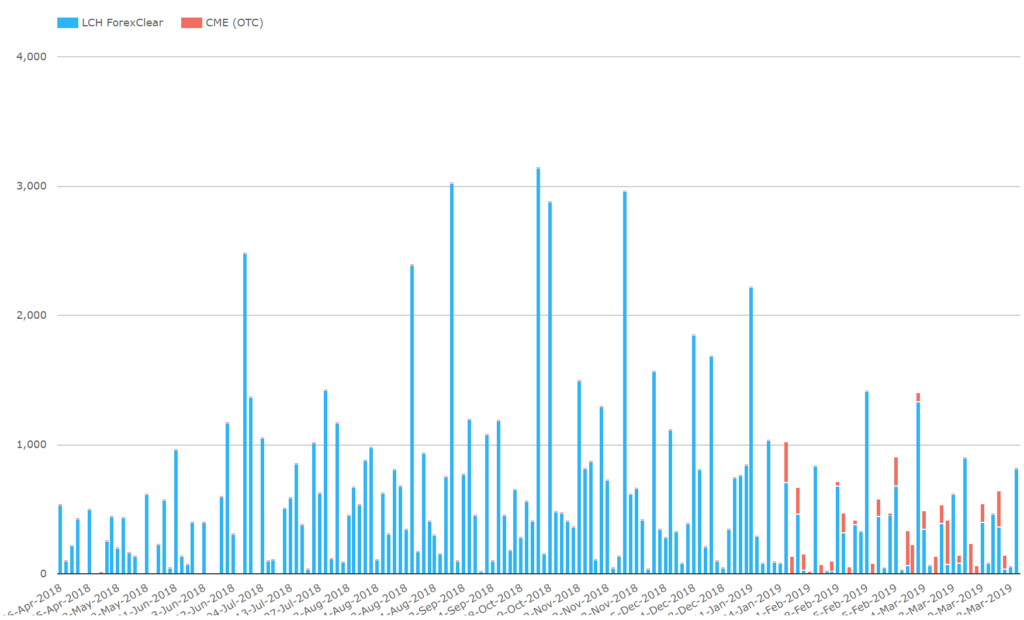

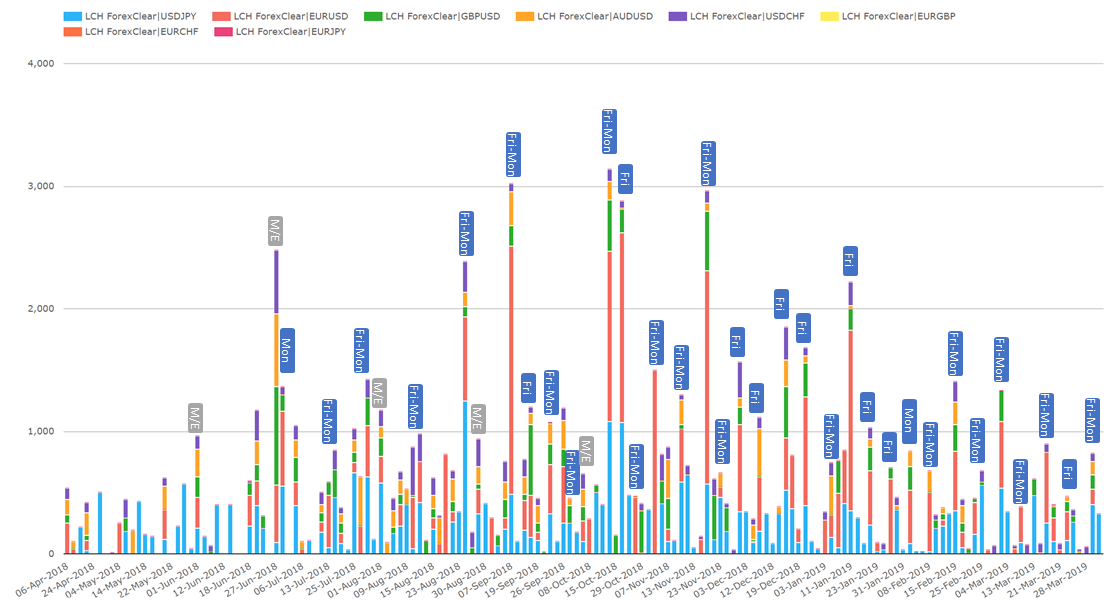

2. CCP Global Cleared Data

There is a less obvious pattern in the cleared volumes.

From 30,000 feet we can see:

- CME made inroads into ForexClear’s prior dominance of G10 NDF clearing during Q1.

- CME had approximately a 25% market share of G10 NDF clearing from a standing start at the turn of year.

The aggregates and the CCP specific charts show more of a pattern.

Showing:

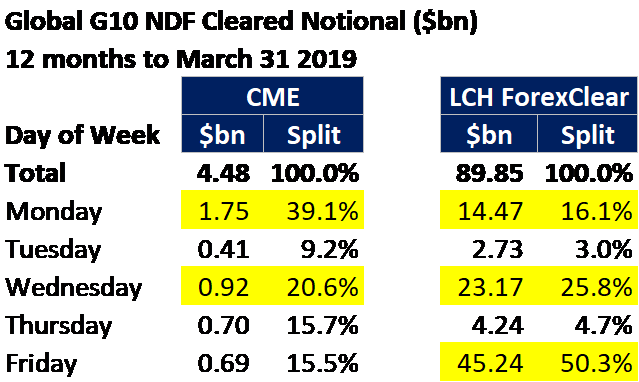

- All the LCH ForexClear peaks above $1bn a day since the turn of the year are on a Friday (blue rectangles)

- Monthly peaks petering out in Q4 in favour of the weekly pattern (grey rectangles)

Observations:

- Clearing at LCH Forexclear unlike LCH SwapClear is done on an immediate backloading basis.

- This may explain the 1- or 2-day lag between Tue and Thu compression runs and clearing of the associated trades on Wed or Fri/Mon.

I would therefore hypothesize:

- TriBalance runs weekly on a Thursday with clearing backloading on Friday or spilling over to Monday.

- Quantile runs regularly on a Tuesday with fewer cleared trades at LCH ForexClear output from those runs.

- TriBalance generates a higher % of cleared trades than Quantile.

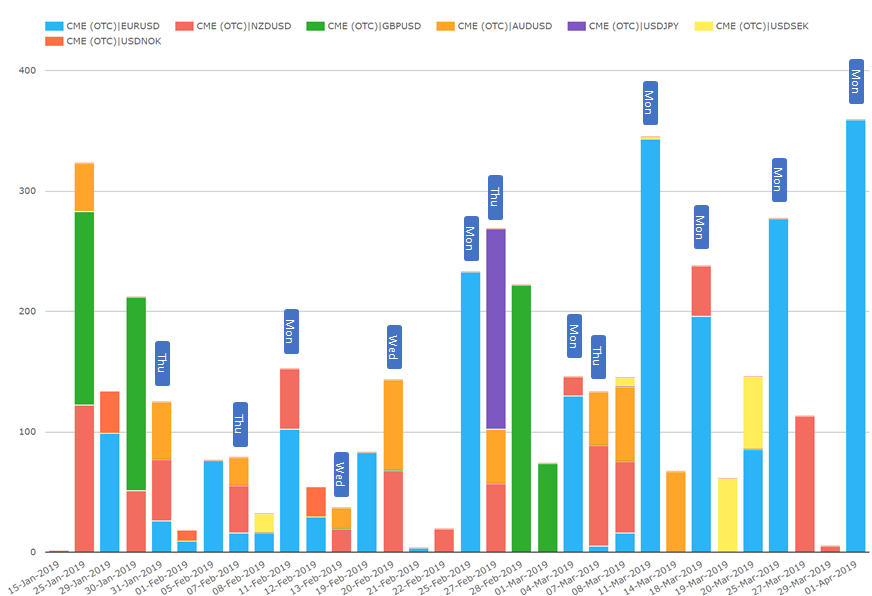

In the process, of getting going CME produces a more irregular pattern:

Showing:

- USDEUR starting to clear regularly on Monday (perhaps backloaded from the TriBalance Thursday run)

- AUDUSD and NZDUSD starting to clear regularly on Wednesday or Thursday (perhaps backloaded after the Quantile Tuesday run)

- The rest pretty ad-hoc – perhaps one-off currency pair specific compression runs or ad-hoc backloading by banks.

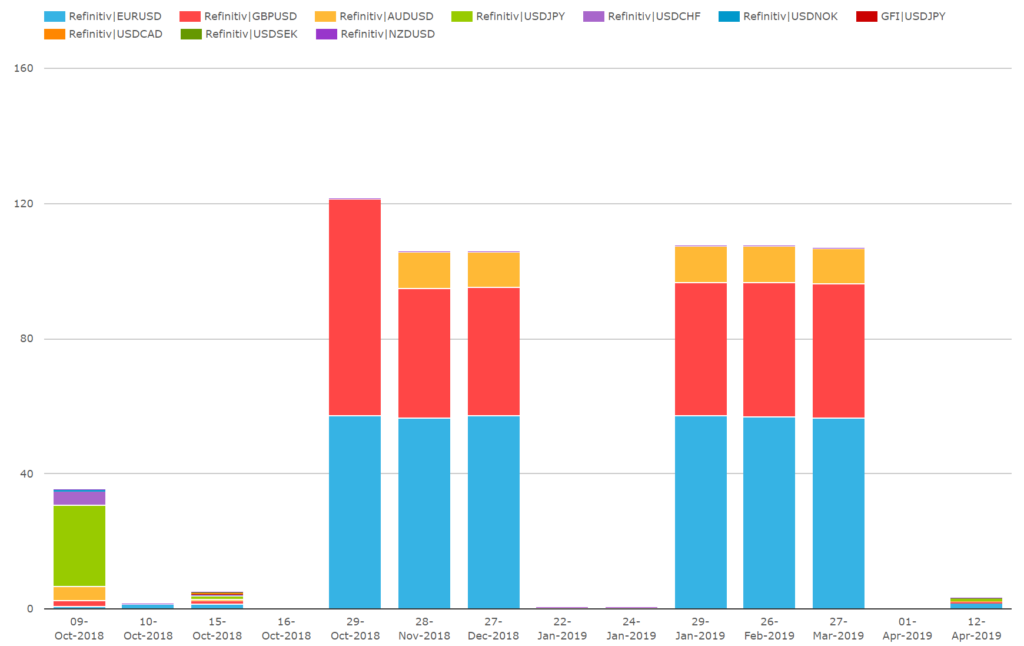

Finally, for completeness, the SEF volumes show that recent SEF G10 NDF volumes are all from Refinitiv.

Showing:

- Volumes are tiny compared with off SEF volumes

- Monthly peaks for the last 6 months which are two days prior to the last working day of the month with EURUSD, GBPUSD and AUDUSD.

Observations:

- I’m aware that there is no special SEF direct trade flow plumbing into ForexClear. Partly this reflects the lack of SEF and clearing mandates for FXD i.e. there is no mandated clearing timeline intraday.

- I expect banks can tolerate this but would expect buy side to demand it if they get involved.

Summary Hypothesis

Currently we have a Tuesday trade execution, Wednesday clearing backloading run (probably Quantile driven) and a Thursday execution, Friday and Monday clearing backloading run (probably TriBalance).

The question is whether this is a permanent fixture or if a more sophisticated but complex approach may supersede it. Let’s look at the limitations of the current approach together with alternatives which might argue they solve more of the problem.

NDF delta compression challenges

Two things seem to matter:

- Participation: Banks are anecdotally split into two largely separate bank groups among the two compression vendors. This limits the risk compression available in each group. Further out in future, it is also critical that the buy side can be enticed to join compression vendors if they want to be long term successful.

- Risk tolerances: Even with all full participation by all counterparties, risk tolerances can prevent maximum effectiveness e.g. banks may not want to limit delta reduction in a given counterparty SIMM portfolio because this would leave uncovered and without margin mitigation the FX delta in the non-SIMM portfolio.

Both of these problems can limit the percentage of delta eliminated, I have heard anecdotes of lower than would be intuitively expected aggregate percentages of delta eliminated.

This a key variable which will affect whether this solution is good enough to last. Now let’s look at the alternatives.

Vega risk compression

G10 FXO volumes do show some uptick but – unlike G10 NDFs – it’s harder to observe a regular calendar pattern given the huge and well traded market. Also, unlike G10 NDFs, we’ve seen no press attesting to FX options risk compression runs. FX options data forensics are for another post.

Whether happening or not, this approach is certainly more challenging than FX delta only compression with NDFs for three reasons:

- More complex algorithm: the risk compression algorithm has to handle two types of risk simultaneously – both vega and delta. Once vega is optimized, delta then has to be handled. This is because risk tolerances for delta can be different from those for vega given non-SIMM portfolio contains delta which contributes to ccRWA.

- Deliverable FX delta adjustments: one way to address the delta problem is to add delta only trades to further adjust FX delta to within risk tolerances. Unfortunately, NDFs don’t always work leading to the complexity of using synthetic FX forwards i.e. same strike FX option collars to adjust delta.

- Extra leverage cost: the FX option collars have twice the trade notional as NDFs meaning this approach incurs greater leverage cost.

Not sure but I speculate this is not yet happening – mainly because NDF delta compression can address the ten parts delta SIMM IM compared to one part vega SIMM IM in a typical portfolio.

Let’s see if vega alone reaches the point of management pain when delta has been tamed…

Cleared options (and forwards) trading

From my recent post, we are definitely seeing a D2D clearing ramp up – but per that post the ramp up has to be further order of magnitude or two to become the main event solution.

Clearing does have the advantage of preventing both FX delta and vega in SIMM altogether and without the leverage overhead of risk compression. Also, we can clear the FX forward hedge with the option as a package which as the further advantage of eliminating FX delta in the package and in CCP IM. Once the investment to set up clearing infrastructure is made it can be convenient. The hurdles to overcome are:

- Upfront infrastructure investment / commercial arrangements: A participant has to become a member at a CCP or procure client clearing services from a clearing broker.

- Wide enough counterparty participation: All the biggest banks are either members of LCH ForexClear already or about to become members. This is a good sign.

- Automation to include the buy side: to avoid operational cost at high volume, and encourage the buy side to come in I suspect a further round of investment is needed to replace the current manual backloading post trade approach and probably hook up the main D2C SEFs to be able to pipe trades direct to ForexClear. Remember: dealer to client portfolios are where the majority of gross counterparty risk and therefore SIMM IM will live in future.

- CCP IM, leverage and RWA cost management: A participant has to set up the capability to optimize IM at minimum and – for banks – the CCP IM and balance sheet impacts. These will be manageable with wide enough participation but will still need a capability to monitor them. This is the topic for my next post.

Buy side participation

Buy side D2C portfolios are where the majority of gross counterparty risk and therefore SIMM IM will live in future – especially as the banks will have partially solved D2D FX risk by then. Not including the buy side will severely crimp the forward benefits of a given solution. Even for D2D portfolios an overriding key factor when comparing clearing and compression is breadth of participation.

The more participants involved in each solution, the greater risk reduction through counterparty netting accrues and improves IM, leverage and RWA costs / benefits in each case.

Summary

The volumes above strongly suggest that risk compression vendor runs dominate G10 NDF volumes – with a weekly Tuesday / Thursday pattern established as set out.

Remember all of the above is about optimization of SIMM FX delta contained largely in FX options. This led me to briefly consider the alternatives – vega compression and cleared FX options trading.

Whether the NDF compression status quo survives depends on several variables outlined (and probably more) in comparing the three solutions. Each of these are hard to quantify and project forward in time.

A key overarching variable is the consensus on participation in each solution among both banks and buy side firms – especially as UMR 4 comes in September 2019 and buy side firms start paying SIMM IM soon thereafter.

Predictions are hard but we will get a very clear signal from the trade volumes – I will check in and post again on them over time as we see strong signals.

My next post will be on FX ccRWA and CCP IM optimization. Please look out for that.