And equally “Why do clients prefer SwapClear?”

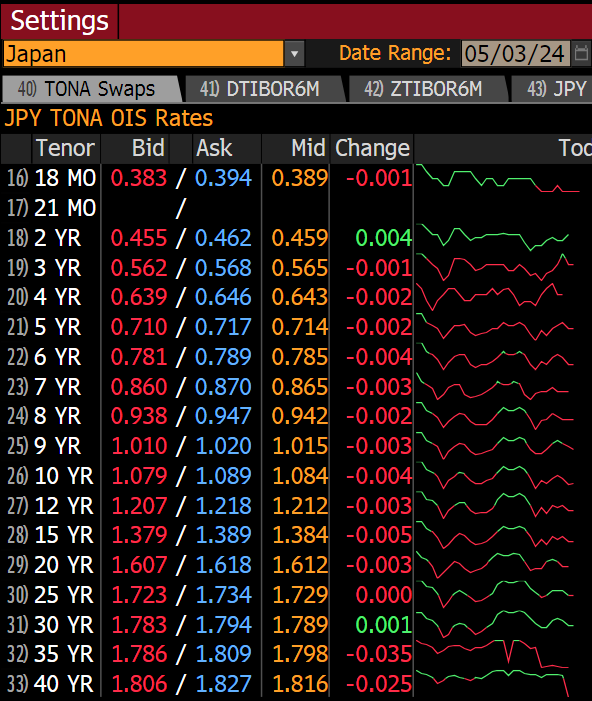

- For JPY Swaps

- This is probably caused by the interplay of regulations in the different jurisdictions.

- As more international (non-US) clients have joined JSCC it has driven the CCP basis less positive (and even negative in some cases).

The Data

It was only recently that I provided a general overview of the JPY Swaps Market in 2024. As so often happens, that blog sparked some conversations, which sparked some number crunching, leading us here.

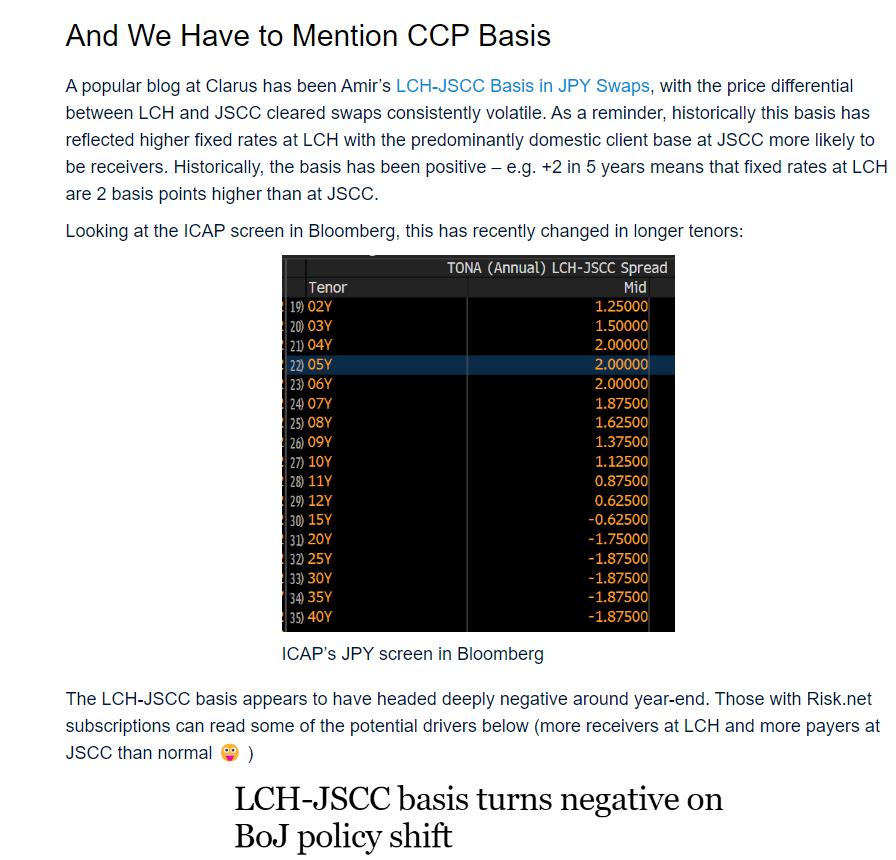

Last time, I noted that the JSCC-LCH basis had shown a significant change in 2024, moving negative in longer tenors:

And whilst I was exploring this I learned that client activity happens at one CCP and dealer activity at another. Which for a market as large as JPY swaps I found quite surprising….

JPY Swaps Are Flying!

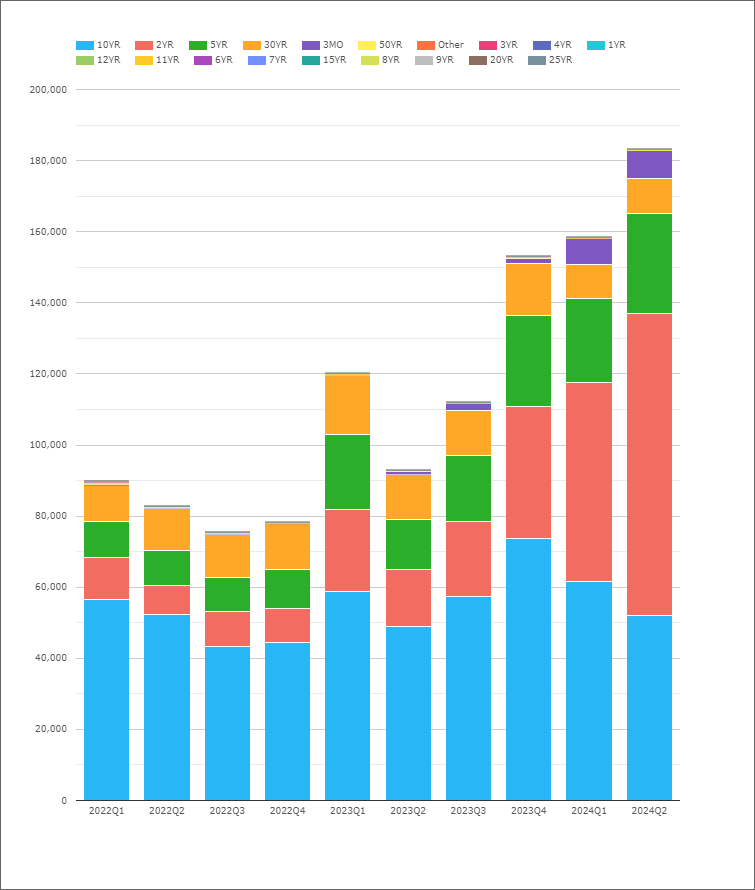

Less surprisingly, CCPView shows that Average Daily Volumes in JPY IRS have increased quarter-on-quarter since Q2 2023, which had already seen decent growth since the “low point” of activity in Q3 2022:

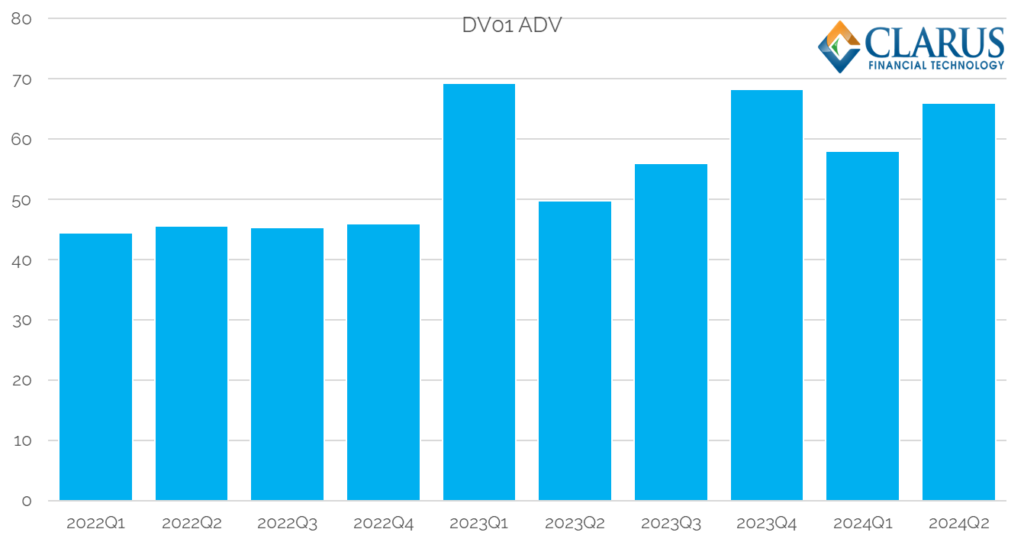

The tenor split above gives the game away here – volumes did not increase in the same way when looking at DV01. It is rare for the data to so unambiguously scream “more short-end trading” but that is exactly what is happening here – just look at the size of the 2Y notional traded so far in Q2 2024. The shorter-end of the JPY IRS curve is many many times more active than we have seen for years. Thank you (Arigatō, ありがとう) cards should be addressed to the BoJ for being “back in play“!

1. SwapClear Is Mainly Client Activity

Has this big increase in notional activity resulted in any changes for the CCPs clearing JPY Swaps?

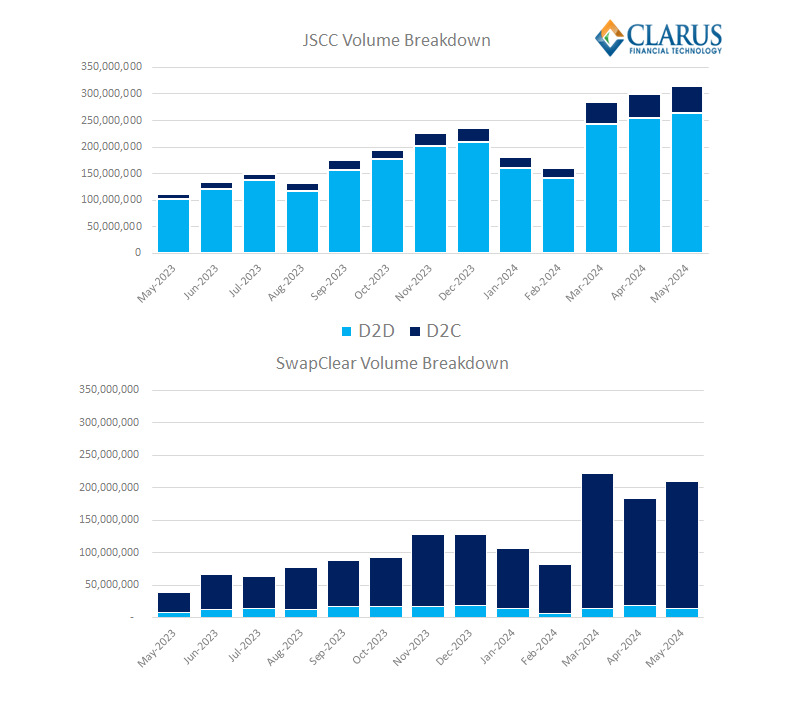

LCH SwapClear JPY activity is almost all labelled as “Client” activity, something I was completely unaware of prior to my previous blog. And these volumes have sky-rocketed in the past two years (lower chart):

What a great marketing chart for JPY clearing at both of these CCPs. I am not so interested in the notional amounts above (you can read this blog about relative market shares of the CCPs), but rather the split between Dealer and Client. Concentrating on the SwapClear (lower) chart;

- 90% of volumes at SwapClear are related to Client activity.

- This is the same when measured by both notional amount or by DV01.

- Is it really the case that only a small proportion of the D2D market executes at SwapClear?

- Given the importance of the JSCC-LCH basis, it may be that most of the D2D volumes at SwapClear are now related to CCP basis trades.

- It is worth noting that, in DV01 terms, dealer volumes have been remarkably stable at SwapClear for the past 2-3 years.

I think the market still has some work to do in terms of transparency here. For example, when I look at JPY IRS screens in Bloomberg, nowhere does it state “these are JSCC rates” unless you navigate to the individual IDB pages (Meitan and Totan run multiple pages for different products at both JSCC and LCH):

Also, are non-Japanese dealers mainly facing each other at JSCC these days? Or are there just not many members of SwapClear that self-clear JPY? More data/investigation is required…..

2. JSCC Is Mainly Dealer Activity

Shortly after publishing my previous blog I discovered that JSCC split their activity by Dealer and Client in their monthly summaries (I have to commend them on the amount of data that is published – a very good thing!). Summary below:

Showing;

- JSCC activity is mainly Dealer to Dealer (and yes, notional amounts show a similar amount of growth to SwapClear above).

- (The split between clients and dealers is provided monthly, without tenor detail. So we are unable to perform a DV01 analysis in CCPView).

- 2022 and 2023 saw upwards of 90% of activity at JSCC related to Dealers.

- Client activity has been gradually increasing since the middle of last year, with 15% of activity tied to Clients in April and May 2024. The full list of clients is available here from JSCC.

- Does more client activity at JSCC drive the CCP Basis negative? Does it drive the CCP Basis negative in the long-end specifically? Discuss!

3. Is Change on The Way?

Will this apparent separation of dealer and client activity at the two CCPs continue? Whilst JSCC appears successful in attracting more clients (see below), there is a big regulatory hurdle to overcome first.

Currently, if you are a US client, you can only trade cleared JPY swaps at CME or LCH SwapClear. The JSCC is not a registered DCO with the CFTC. Risk.net recently covered this and highlighted that the JSCC are continuing to petition the CFTC for recognition:

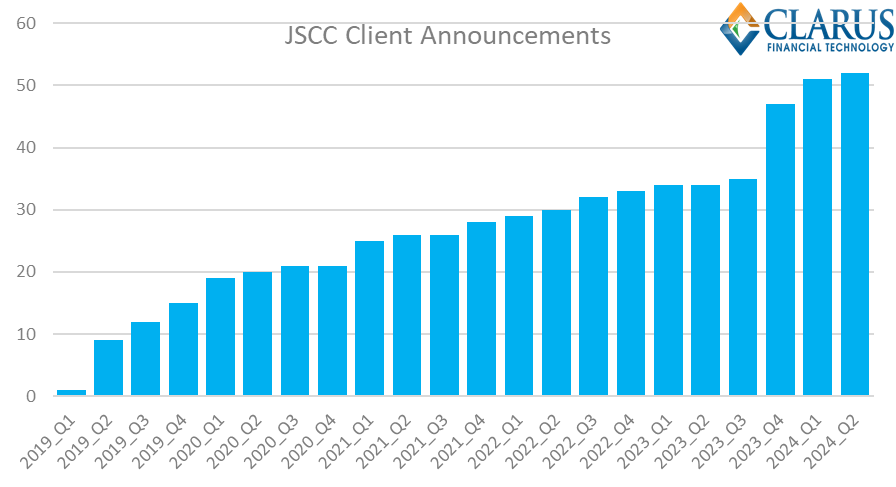

JSCC can, however, clear for other international clients. And it has a successful track-record for doing so, with each client announced on their website (which is an impressive level of transparency). Many of these clients have been hedge funds in the recent ramp up to over 50 clients (yes, I really noted down the date of each website announcement!):

Are the increasing numbers of clients clearing at JSCC causing a shift negative in the CCP basis? I don’t think we can say, but given the CCP basis is largely driven by market structure (see below), it is likely a contributing factor.

On the flip-side, LCH does not have a licence to clear for Japanese (clients/banks?) accounts in JPY (other currencies are fine), which has been the case since April 2016.

Maybe it is obvious to market participants trading this day-to-day, but why this regulatory divide forces dealers to JSCC and clients to SwapClear isn’t immediately obvious to me. What IS immediately obvious is that this regulatory-enforced separation leads to a lot of volatility in the CCP basis. The CCP basis significantly decreased after the first hedge funds began to onboard in 2017 and has been seen to react to potential regulatory changes as well (see Risk.net coverage). It still seems odd to me that Europe would like to intentionally introduce this dynamic with the Active Account Requirement.

A combination of clearing mandates and commercial determination has created two successful JPY swap franchises in clearing. There is nothing to say that business would flood from one to the other in the event of regulatory change – but it would be sure fun to watch what does happen!

In Summary

- In JPY swaps, JSCC volumes are mainly Dealer to Dealer, whilst LCH SwapClear see client volumes.

- Both Clearing Houses have seen significantly higher notional volumes recently, driven by increased activity at the short-end of the JPY swaps curve.

- Having different market participants active at different CCPs is likely to drive volatility in CCP basis.

- JSCC has recently announced its 50th client joining the service.