- LIBOR cessation appears to have reduced activity in certain short dated futures markets.

- CHF and JPY used to see volumes of $1.5Trn per month notional equivalent.

- But these two markets have seen reduced activity in 2022.

- However, GBP short term interest rate futures activity has been robust.

- We outline differences in hedging needs for dealer swap books as a result of LIBOR cessation.

Note: This post has been updated since first publication to reflect updated data for CHF SARON contracts at ICE.

2022 So Far….

I think we would all agree that 2022 has been a crazy year for markets. The combination of:

- Central banks all being “in-play”

- Inflation consistently surprising on the upside

- A major war

….all lead to elevated volatility. For dealer desks, frequent re-positioning and changes in risk positions normally lead to elevated volumes.

These elevated volumes are typically seen first and foremost in futures markets (Exchange Traded Derivatives). Why?

- Standardised products

- Standardised pools of liquidity

- 24-hour markets

- No counterparty credit

I’m sure you can all add your own reasons.

However, 2022 appears to be different. Let’s take a look at some markets where Futures are not seeing record volumes and talk about the underlying reasons why.

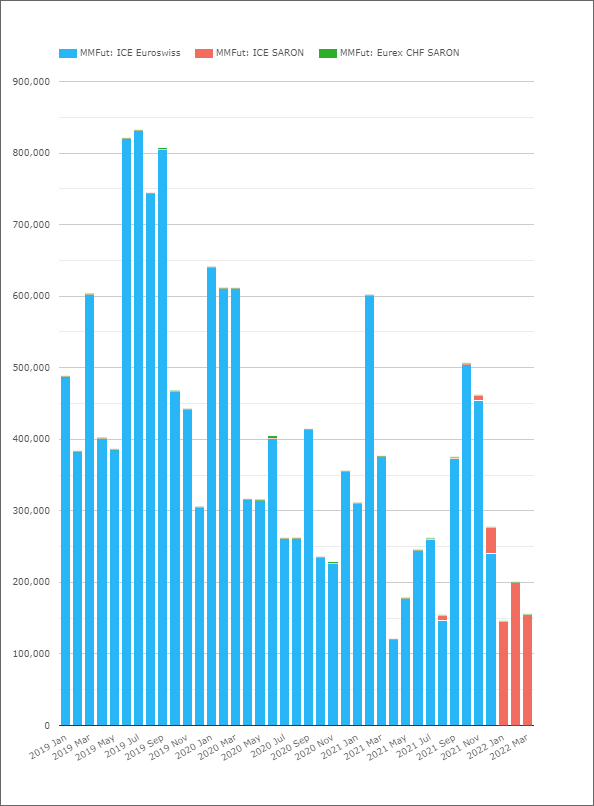

CHF Short Term Interest Rates

Short Term Interest Rate futures for CHF market participants have transitioned from LIBOR to SARON – no news there. Our data in CCPView shows that the transition happened late, but it did happen:

Showing;

- CHF LIBOR STIRs saw volumes as high as $800bn per month in 2019.

- CHF SARON STIRs appear to be in the process of establishing themselves, having reached a peak of $200bn in February 2022, with March on track to beat this.

- Trading in CHF STIRs is bound to pick up as the outlook for the SNB evolves, and it will be interesting to see if SARON based products can replicate the success of their LIBOR-based predecessors.

Are There Reasons to Expect Reduced Activity in RFR STIRs compared to LIBOR STIRs?

From my own experience trading a CHF swaps book (for example), in a CHF LIBOR world:

- Some demand in short term interest rate futures exists from swaps traders hedging their fixing risks.

- The concentration of liquidity into standardised IMM dates is particularly useful to concentrate price discovery of something like CHF FRAs, which are illiquid.

- The “FRA ladders” of dealer books, driven by interest rate swap exposures, probably drove a lot of activity in CHF LIBOR futures.

- This activity was further elevated by market standard interest rate swaps trading versus 6 month CHF LIBOR, whilst futures liquidity was all concentrated versus 3M LIBOR. That means to hedge a single 6 month fixing on an Interest Rate Swap, the first two IMM contracts in Short Swissy would have been traded.

- The presence of so many 6M fixings would also lead to swaps traders running large front month versus second month interest rate positions, which would also need constant hedging/readjustment.

And what happens when LIBOR ceases and Interest Rate Swaps all trade versus the overnight rate, SARON? I am sure everyone is well aware by now:

- A floating rate fixing on an OIS (for CHF, the SARON leg) does not create a term interest rate exposure for 3M or 6M like a LIBOR interest rate swap did.

- Each (daily) fixing creates an overnight exposure.

- For a LIBOR based interest rate swap, a fixing today is not perfectly hedged by a fixing tomorrow. A 0.5 basis point difference in the fixing of 6M CHF LIBOR on a CHF500m swap would result in a PnL (loss or gain) of CHF12,500.

- A 0.5bp move frequently happened from day to day on the old LIBOR fixings.

- That may not sound like much, but it only takes a couple of fixing moves like that to result in serious PnL moves (so-called “bleed” as these are considered second-order risks).

- OIS are different.

- An OIS fixing today shares over 99% of its subsequent fixings with an OIS that fixes tomorrow. A 0.5bp move from one day to the next on a CHF500m OIS results in just CHF69 of PnL!

Of course, this doesn’t preclude the fact that market participants still need to hedge themselves against long-term changes in the structural level of SARON. The SNB cannot maintain negative rates for ever – I can personally testify to the fact that day-to-day inflation is alive and well here in Switzerland! And standardised products such as futures serve as an extremely efficient hedge, particularly in Switzerland where SNB meetings tend to coincide with IMM dates.

Long-term, we will be monitoring where the balance lies between OTC SARON products and SARON futures. The ISDA-Clarus RFR Adoption Indicator already maintains a measure of the percentage of risk traded in Futures vs Swaps (see chart 4 here).

Primers on Short End Trading

For those of you a bit lost in the technical details, we have some resources here on the blog that walk through the intricacies of trading short-end risk in interest rate derivatives. Some examples include:

The blog below on Toxic FRAs was also really well received last year. I guess we could update this one for those still grappling with USD LIBOR transition:

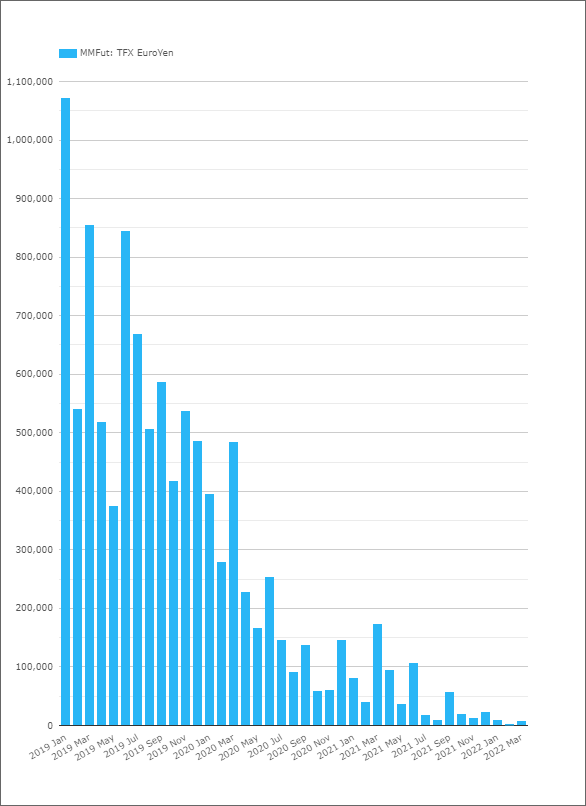

JPY Short Term Interest Rates

Back to the topic in hand. With JPY LIBOR also ceasing, we have seen a dramatic reduction in volumes in JPY STIRs. Also from CCPView:

Whoah, I find it surprising that this chart is so different to the market behaviour in CHF!

- This shows monthly volumes in the TFX Euroyen contract. See contract specs here.

- Note that this contract is versus JPY TIBOR – which has not ceased!

- Indeed, TIBOR swaps are continuing to trade (and are cleared at JSCC). Our ISDA-Clarus RFR Adoption Indicator suggests that TIBOR swaps are settling somewhere between 5-10% of the overall market.

- However, from memory, I recall TFX Euroyen was by far the deepest pool of liquidity for hedging fixing risk on JPY IRS. Even when those JPY IRS were versus LIBOR.

- As far as I know, there are no active JPY TONA ETD contracts. Only a suspended TFX offering (detailed here, suspended July 2017).

- It is hard to believe that a $1Trn+ market can almost completely disappear.

- From $1Trn to $3.2bn traded in February 2022 – a 99.70% reduction in volumes.

- Amazing to consider that the reduction in JPY activity has been gradual month on month, where-as CHF STIRs still saw $500bn of activity 3 months before cessation and have transitioned a portion of activity into SARON.

When will we see a TONA futures contract again? Puzzling….

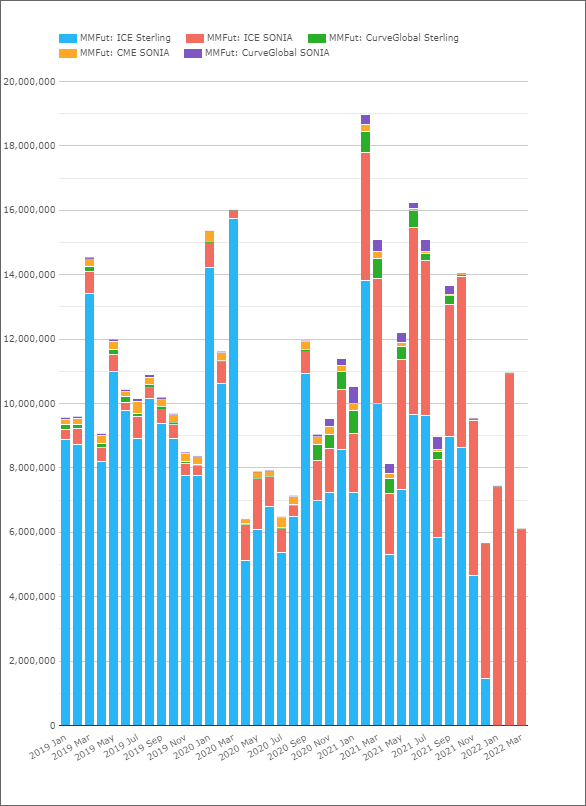

GBP Short Term Interest Rates

The GBP market has seen acute competition recently. With new entrants and multiple different offerings in SONIA futures, it has been a competitive landscape (see here for example). Now that GBP LIBOR has ceased, it is no longer quite so competitive!

Showing;

- A relatively successful transition from GBP LIBOR to GBP SONIA futures in terms of maintaining volumes.

- Before cessation, there would have been some volumes linked to LIBOR vs SONIA basis positions. These have now disappeared.

- Nevertheless, monthly volumes are pretty healthy! Particularly compared to the JPY experience above!

- 2019, GBP STIRs average monthly volumes were $10.25Trn.

- 2022, GBP STIRs have averaged monthly volumes of $8.15Trn.

- That seems to be a pretty good outcome for the exchanges as a result of LIBOR cessation?

In the intervening years (2020 and 2021), I find it hard to unpick the impact of LIBOR vs SONIA positions and the potential “replication” of liquidity across different exchanges. The key points going forward for GBP SONIA trading are:

- Can demand continue at such elevated levels without all of the “event risk” in the markets?

- Will there be a long-term impact from the reduction in interest rate swap related hedges on market demand?

- Interest Rate Swaps can still be hedged with SONIA futures! How healthy is the relationship?

Remember – Futures can Still Hedge Swaps!

Finally, please note that futures can still be used to hedge the term interest rate risk arising from the fixed leg of an interest rate swap. Trading the four front SONIA futures versus a one year SONIA OIS is a perfectly valid hedging strategy. It is just that as the SONIA fixings come in on the one year SONIA OIS, even if the dates do not match the underlying futures, there is little need to rebalance the hedge. Rebalancing will be focused on date differentials, particularly over MPC periods, and these will be very carefully monitored/managed across dealer desks.

For what it’s worth, I think all futures contracts on overnight rates should not be traded on IMM dates, but should match the underlying central bank meeting dates. But I think that is a blog for another time.

In Summary

- Trading activity in some Short Term Interest Rate futures contracts is being impacted by both event risk and LIBOR cessation in 2022.

- LIBOR cessation appears to have played a different role in the JPY market compared to CHF and GBP.

- GBP SONIA activity has been notably robust.

- Hedging interest rate swap fixing risk was a consistent source of flow back in the LIBOR world.

- STIR markets may therefore need to see more hedging interests entering the market to replicate volumes from the past.