Following up on our analysis of the Brexit effects on Rates markets and Credit markets we estimate how much of the swaps market is now executing on-SEF.

The extent of the move varies from currency to currency and between Interbank markets and their Clients.

We look at each market in turn.

The Irony

The laws of unintended consequences are at play in these early post-Brexit days. We have witnessed Brexit move $4Trn of derivatives to US-registered SEFs before the end of January 2021. That is in stark contrast to the early days of Dodd-Frank, when some US banks set up European entities to retain access to “European liquidity” which was anticipated to stay off-SEF. Now that same European liquidity pool is potentially having to execute on-SEF. You couldn’t make it up….

Methodology

CCPView provides a global view of cleared Derivatives markets. Most CCPs split their activity between Dealer (House) and Client volumes.

SEFView provides us with total volumes executed on-SEFs. Like CCPView, these volumes are uncapped, reflecting the true volumes executed (even above the block thresholds).

The SEF world is split between interdealer central limit order books (CLOBS) such as those operated by tp-ICAP, BGC, Trads etc. These are all D2D venues. Tradeweb and Bloomberg, for Rates, are RFQ platforms and trade D2C volumes.

We can therefore compare the D2D volumes on-SEF versus the Dealer volumes in CCPView to calculate the percentage of the overall global market that is executing on-SEF.

We do the same for D2C volumes on-SEF versus Client cleared volumes in CCPView.

The Brexit-effect is pretty clear! On to the charts….

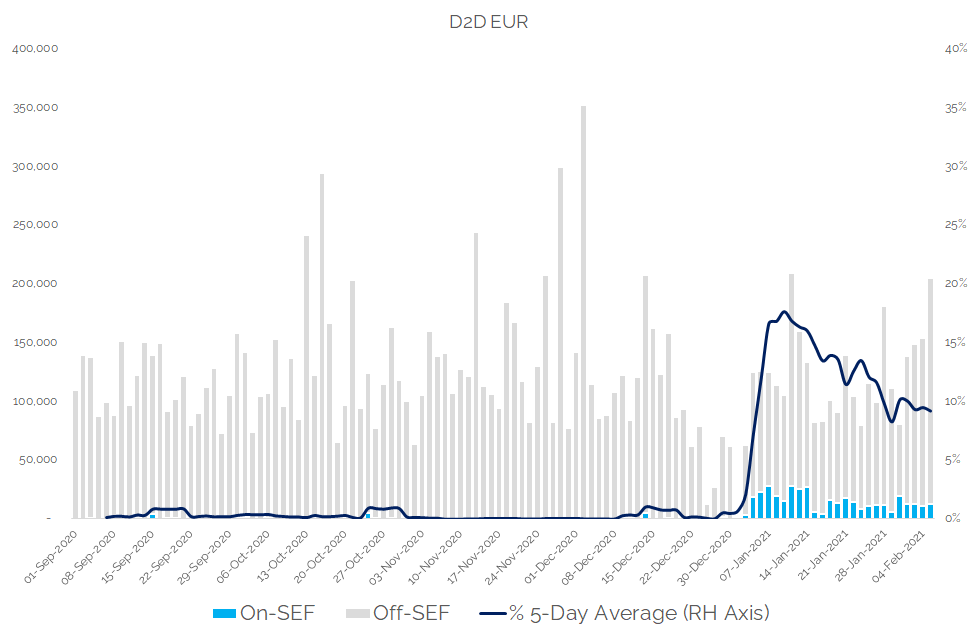

EUR D2D Market

What portion of the global D2D EUR swaps market is now executing on-SEF?

Showing;

- 18% of EUR D2D volumes were being executed each week on-SEF in the early days of January.

- This reached 24% on some days.

- EUR swap trading was rarely seen on D2D SEFs during Q4 2020.

- The move to SEF trading seems to be entirely down to Brexit.

(Please note that 2020 EUR SEF volumes exclude some compression runs reported by BGC. The volumes were forward-starting swaps which we believe were the results of Capitalab compression runs and therefore not price-forming activity.)

It is notable that the proportion of the EUR D2D swaps market executing on-SEF has now begun to creep back below 10% in recent weeks.

Why is this happening and what will the final “steady-state” look like? We can only follow the data to find out!

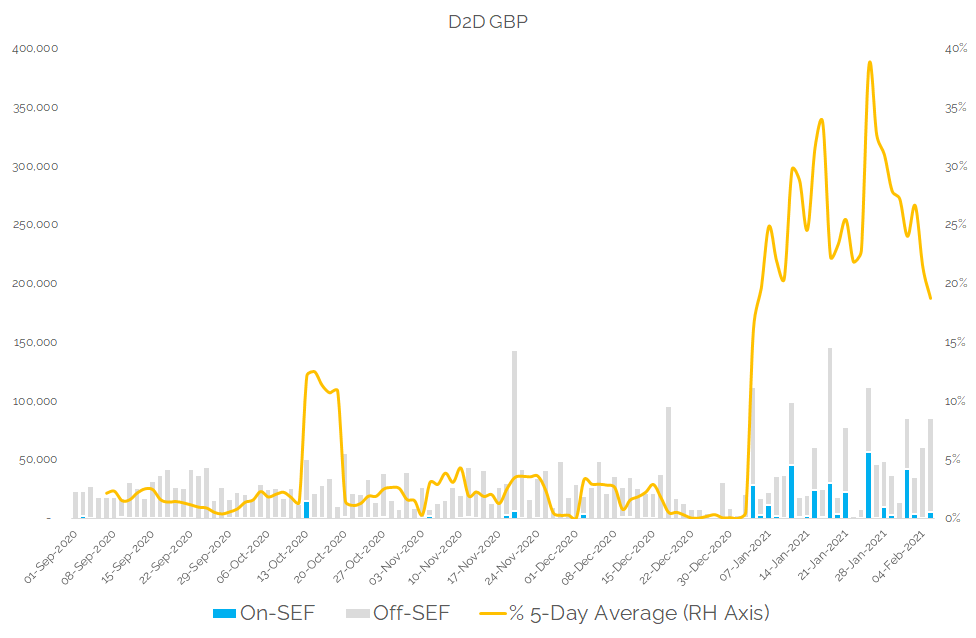

GBP D2D Market

The effects on different markets is striking.

The move in EUR D2D swaps is the “purest” representation of what is happening as a result of Brexit alone.

In GBP markets, two factors have combined to amplify the move – benchmark reform AND Brexit. Just look at the data:

Showing;

- In some weeks, 40% of total GBP IRS in the global market has traded on-SEF.

- This is largely a result of weekly operations on the NEX SEF.

- The GBP volumes across NEX, that used to be FRAs, have now switched to Single Period Swaps.

- The volumes in these SPS in GBP has increased from virtually zero in 2020 on the NEX SEF to over 50% of the global GBP IRS market on some days in 2021!

- There are also regular volume spikes reported by the TP SEF. We assume these (smaller) spikes are also due to FRA runs converting to SPS in GBP this year.

To estimate the Brexit-alone impact on GBP, I ran the same data excluding the NEX SEF. This shows much the same pattern, just shifted lower to represent ~10-25% of the overall GBP IRS market. That is still a significant move higher from basically zero in 2020!

Other Markets

Completing the analysis of D2D markets, the USD data is equally as messy as GBP. There is also evidence that market participants are switching out of USD FRAs and into USD SPS (such as on the Dealerweb SEF). As a result we’ve seen as much as 65% of the global USD market executed on-SEF in 2021.

However, it is not clear from the data whether Brexit has moved a (meaningful) amount of volumes on to SEFs for USD swaps.

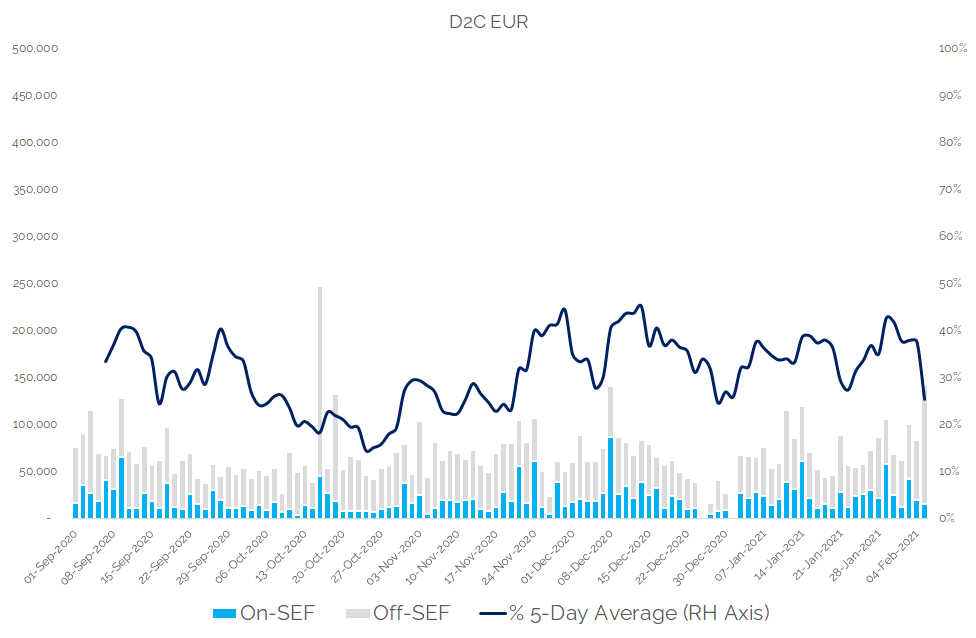

Meanwhile, in D2C markets, the EUR market probably best illustrates the lack of impact that Brexit has had. We don’t see any significant change in client behaviour when comparing EUR volumes on D2C SEFs to client-cleared volumes in EUR:

In Summary

- 10-20% of the interdealer EUR swaps market now executes on-SEF. This is because of Brexit, rising from virtually zero last year.

- Up to 40% of the interdealer GBP swaps market now executes on-SEF. This results from the twin impacts of Brexit and a move to SPS trading instead of FRAs.

- There has been little impact to Client markets.

- The move onto SEFs from interdealer markets in both GBP and EUR seems to have waned in early February.

- We need to keep an eye on the data to follow this trend.