- US regulators have announced that banks should cease entering into any new contracts referencing USD LIBOR from 31st December 2021.

- This is consistent with the announcement last week from the UK regulators, who pointed out that LIBOR fixings may be published after end-2021 but that no new business could be written against them.

- These announcements were coordinated with announcements from ICE that they will consult on the specific timelines for LIBOR cessation. These consultations will end in January 2021.

- We may see USD LIBOR continuing to be published all the way into 2023, but that may only be used for legacy contracts.

- Clarity is coming!

What happened?

The last time we covered changes to ICE LIBOR, it was way back in April 2018, when ICE were introducing the waterfall methodology. Clearly, a lot has happened to LIBOR since then!

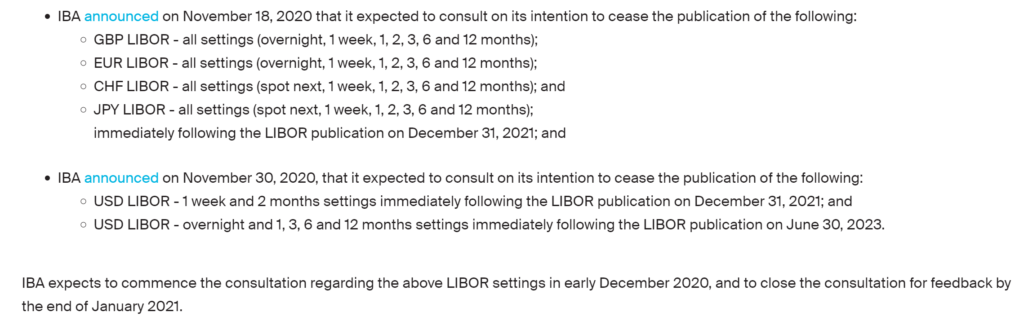

These past two weeks saw two announcements from ICE, the administrator of LIBOR. They are summarised well enough on the ICE website:

So we have:

- A consultation that all GBP, CHF and JPY LIBORs will indeed cease to publish at the end of 2021. EUR is also included, but seeing as hardly any EUR derivatives exist versus EUR LIBOR, and that EURIBOR will continue for a while, I won’t spend any time on that.

- A consultation also proposing that USD LIBOR continues until middle 2023.

- The consultation period will be short, closing end of January. The market will have much needed clarity after that date.

We Do Not Think This Is a Delay

I noticed that much of the press is reporting the second point, regarding USD LIBOR publication continuing into 2023, as a “delay” or “reprieve“. I am not so sure. I see it more as filling a gap in the fallbacks.

What Have the Regulators Said?

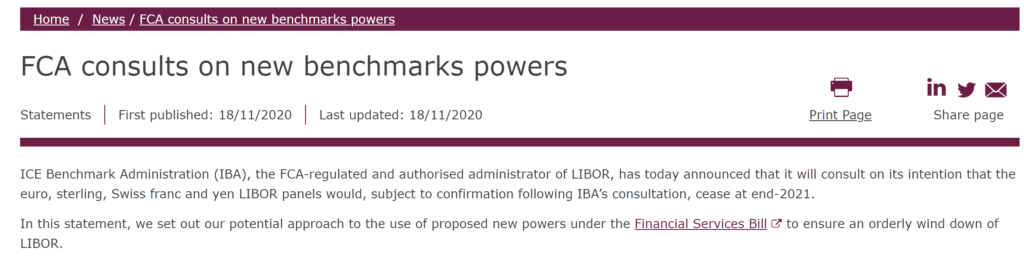

The consultations from ICE were not released by themselves. There were coordinated statements released at the same time from the UK’s FCA, ISDA and the Fed.

I think the statements from the regulators are probably more important than the content of the consultations in this case.

What Did the Fed Say?

In a joint statement yesterday, the banking regulators in the US said:

Given consumer protection, litigation, and reputation risks, the agencies believe entering into new contracts that use USD LIBOR as a reference rate after December 31, 2021, would create safety and soundness risks and will examine bank practices accordingly. Therefore, the agencies encourage banks to cease entering into new contracts that use USD LIBOR as a reference rate as soon as practicable and in any event by December 31, 2021.

Statement on LIBOR Transition, joint statement from US regulatory agencies.

This isn’t an outright statement that banks are not allowed to write any more LIBOR-based business after the end of 2021. But they do need to have a jolly good reason to be writing any LIBOR-based business after that date! The letter even lists the following reasons that LIBOR-referencing contracts could be entered into:

- Default management at a CCP.

- Quoting unwind prices on legacy client trades executed prior to 2022.

- Risk reducing trades in terms of LIBOR exposures for the bank or client.

- Novating out of legacy LIBOR contracts.

They state that these are a set of “limited circumstances”, so I don’t think anyone can expect to enter into LIBOR derivatives as BAU after 2021. Even if LIBOR is still being published.

It is hard to work out how explicit the language is intended to be – maybe we will see some more clarifications after the consultation process?

There is also an emphasis from the US regulators on securing “robust fallback language.” This could call into question how banks can trade with clients who haven’t signed up to the ISDA Fallback protocol in January.

I guess the next step is for all of the Futures exchanges (CME, ICE, Eurex, CurveGlobal) to now line-up and announce their contracts will no longer reference LIBORs either (even if it continues to be published).

What Did the UK Regulators Say?

I feel like the statement out of the UK wasn’t quite as direct as the US regulators:

The full statement is worth summarising, but in reverse order to the original:

- No, this is NOT a cessation, or even a pre-cessation, announcement for LIBOR. Historic spread calculation dates are NOT being crystallised as a result of these announcements.

- The FCA can decide that ICE needs to continue publishing LIBOR to protect market integrity, consumers or if legacy exposures cannot be successfully transitioned.

- However, if the FCA does compel ICE to use a new methodology to publish LIBOR past the end of 2021, no new business can be written against this rate.

- EURO and CHF LIBOR are very very likely to die completely and no longer be published.

- GBP LIBOR does at least have forward-looking SONIA term rates being published. The FCA could, in theory, compel the continued publication of GBP LIBOR fixings after end-2021 using a new transaction-based methodology.

- JPY appears to have a big question mark hanging over it, with a prototype term rate still in development from Quick.

What Have We Learned?

These announcements tell us that;

- It remains the wish of the regulatory community that no new LIBOR business should be written after end-2021.

- The ICE consultations will be important. Please respond. Please include DATA in your response, not anecdotes!

- CHF LIBOR contracts could well be the first to see fallbacks used. Just as they were the first to transition to a Risk Free Rate in OIS markets (TOIS to SARON)

- There is a big question mark hanging over JPY markets.

If USD LIBOR can continue to be published into 2023, and exclusively used for legacy contracts through regulatory edict, then it gives term SOFR a chance to also get off the ground.

All of that said, there must be a serious risk that the ICE consultation responses end up as a barrage of begging to extend the cessation date? Let us know in the comments below how you think this might play out next year.