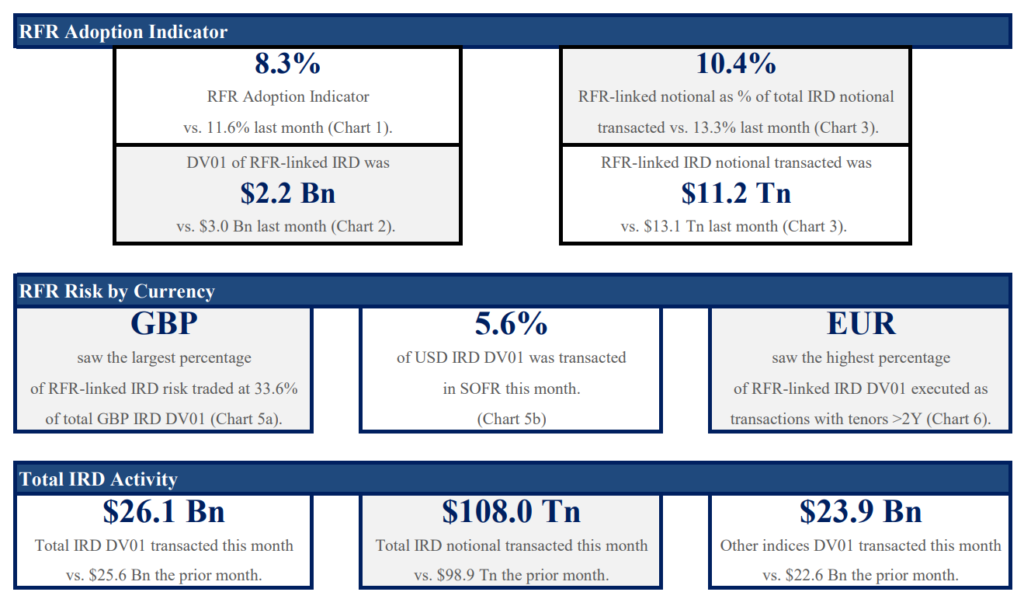

The ISDA-Clarus RFR Adoption Indicator has been published for October 2020. The headlines are:

- The RFR Adoption Indicator was 8.3%, a decline from the previous month (which saw an all-time high).

- This is the fourth highest reading on record.

- 5.6% of all USD risk was traded in SOFR vs 9.7% last month, reflecting the impact of the CCP discounting change.

- The switch to SONIA in interbank markets has seen more long-dated SONIA risk trading than ever before.

- 37% of GBP SONIA risk traded was in maturities longer than 2 years.

Please click here to access the full report.

Transition Thoughts

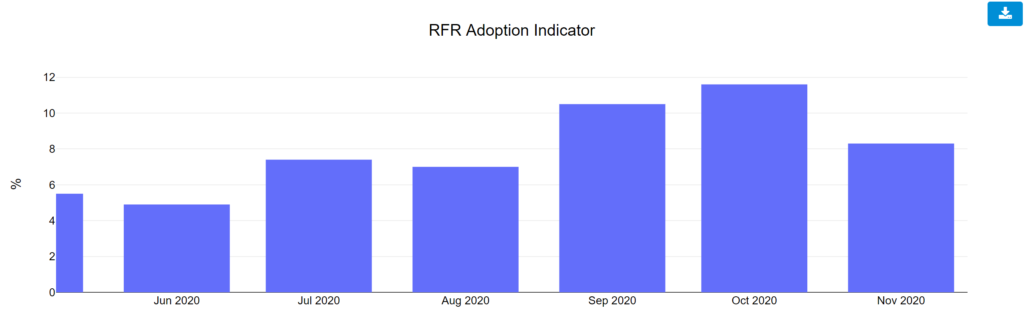

I guess we should be pleased with the progress made by the market since we first published the indicator in June 2020. In the five months of trading since then, it has increased from 4.9% to 8.3%:

However, despite serious questions over whether anyone will actually be able to trade LIBOR-linked derivatives in 2022, we are still in a situation when 90%+ of new risk transacted is versus LIBOR each month.

That is still a pretty scary situation with a little over 12 months left – or 275 LIBOR fixings.

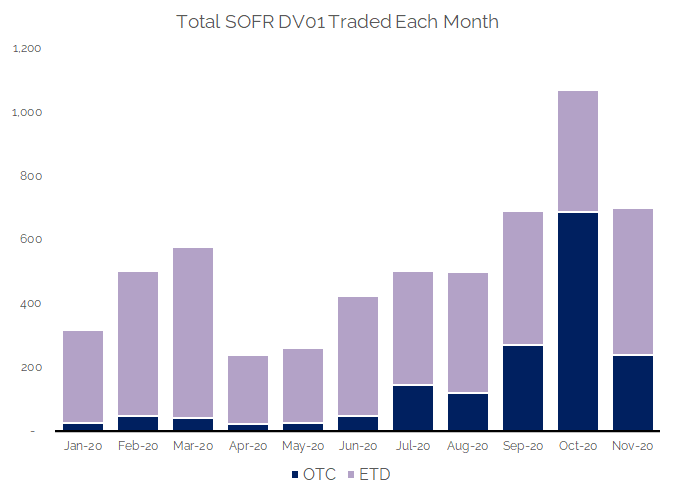

SOFR

I don’t think it comes as a surprise to anyone that the amount of SOFR activity this month was lower than last month, now that the discounting switch auctions have taken place.

Our data shows just how large those auction impacts were on the total amount of SOFR risk transacted in derivative markets:

Showing;

- October 2020 was the only month on record when total SOFR DV01 topped $1bn.

- This reduced by about 30% this month.

- The total amount of SOFR risk transacted this month was comparable with September 2020, however, when some of the pre-positioning for the discounting auctions was bound to have taken place.

- November 2020 was the second highest month on record (just) for SOFR risk. This does therefore suggest that the discounting risk is resulting in more SOFR risk being traded on a day-to-day basis than previously.

For those interested, we have tried to also find the auction swap records in the SDR data. But there remains no sign of swaps with the matching coupons as reported by LCH:

The CFTC reporting delay for these swaps was meant to be only four weeks, so I am somewhat surprised these do not show up for the SDR records on October 16th yet. Strange?

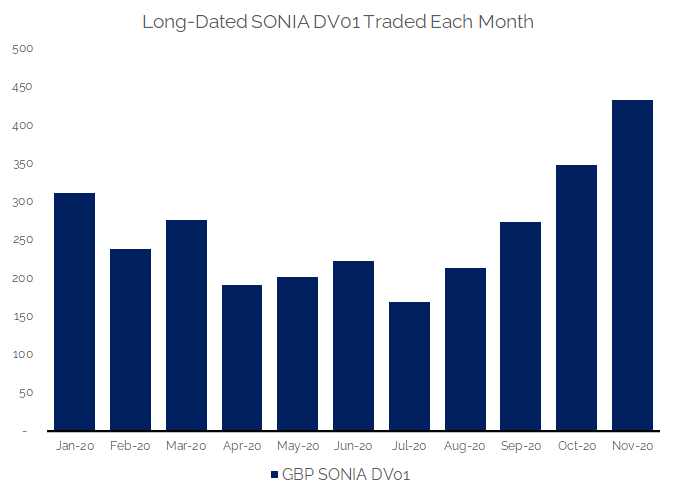

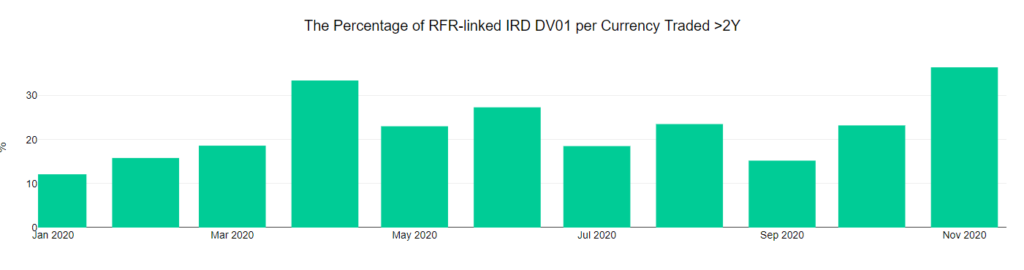

SONIA

Shortly after the discounting switch in USD, there was another significant milestone in the transition story. On October 27th, the BoE officially “encouraged liquidity providers in the sterling swaps market to adopt new quoting conventions for inter-dealer trading based on SONIA instead of LIBOR”. See our blog covering the switch here.

The SDR data for the days surrounding this announcement did not suggest a massive change occurred. However, when we look at the RFR Adoption Indicator data for the global market, we do see encouraging signs.

Showing;

- The amount of GBP SONIA DV01 traded in maturities longer than 2 years.

- November 2020 saw a record amount of long-dated SONIA risk traded.

- This increase in long-dated activity in SONIA markets can also be seen by the fact that 36.4% of SONIA activity was in tenors longer than 2 years, a new record:

Interestingly, for anyone thinking SOFR is not yet a long-dated market, 27.7% of SOFR activity was also in tenors longer than 2 years.

So, there are clearly positive signs out there for the transition story!

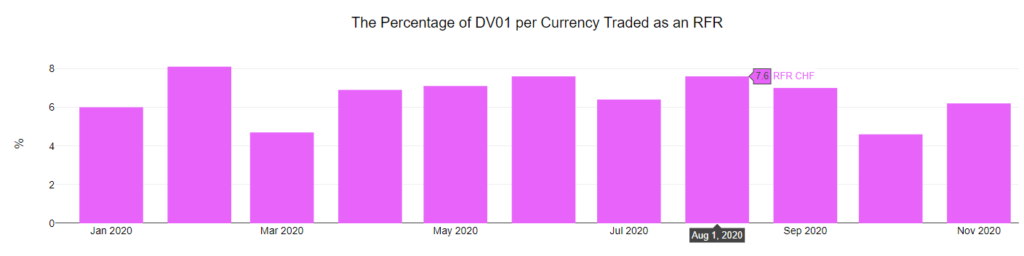

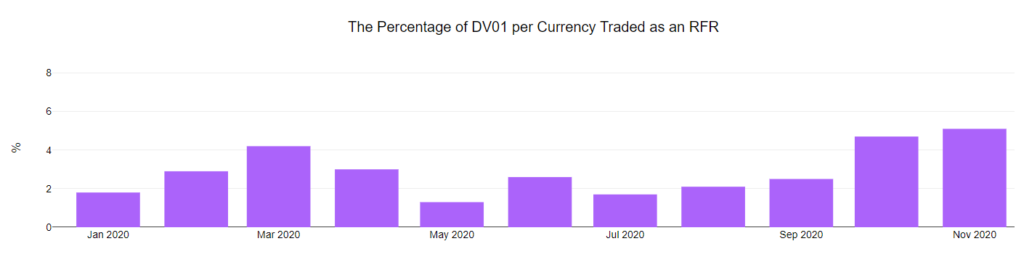

SARON and TONA

The “ICE LIBOR Consultation on Potential Cessation” has now been published. From last week’s accompanying regulatory announcements, there were two stand-out features.

One is that CHF LIBOR could well be the first LIBOR to cease publication and see Fallbacks used. You would therefore expect to see SARON adoption picking up at speed in the coming months. It is still at low levels:

Secondly, there is still no term rate for JPY LIBOR (the Quick TORF is still in prototype form). Therefore, JPY markets seem to be in a somewhat similar situation to CHF. However, TONA trading continues to make up just 5% of overall risk traded in JPY derivatives markets:

ICE Consultation Responses

With all of that said, we again encourage market participants to respond to the important ICE LIBOR consultations in January. If you need any of the data underlying the RFR Adoption Indicator, including granular breakdowns of DV01s traded in RFRs per tenor, please contact us for a CCPView subscription.