How large are Cleared Swap markets?

I published my first article on the ION Blog covering Cleared Swap markets and comparing open interest and volume between Swaps and Futures for Interest Rate Derivatives. Please read at How large are Cleared Swap markets?

SOFR Swaps Volumes and Share – July 2023

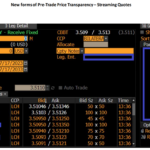

Let’s update my blog on IDB Market Share in SOFR Swaps with the most recent data and expand the coverage to also include D2C venues. Types of SOFR Swaps SOFR Swaps in the IDB (inter-dealer broker, D2D) market trade primarily as Spreadovers to US Treasuries. This is by far the most frequent trade type in […]

FSB Paper on Liquidity in Core Government Bond Markets

I recently took a first look at Central Clearing of Bonds and Repos and in that blog I mentioned a Financial Statility Board (FSB) paper on Liquidity in Core Government Bond Markets. This paper analyses the liquidity, structure and resilience of government bond markets, with a focus on the events of March 2020; characterised as […]

Even More on Blocks and new rules for FX

CFTC Global Markets Advisory Committee Following up on my blog last week, there is now the recording of the CFTC’s Global Markets Advisory Committee (GMAC) available on youtube: There are some interesting take-aways: Showing; Elsewhere, Tradeweb and Bloomberg provided insights into the RFQ1 vs RFQ-to-many split amongst large trades. This is some really interesting data. […]

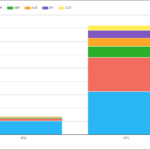

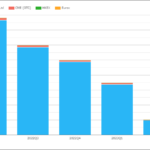

2Q23 CCP Volumes and Share in CRD

A review of Credit Derivatives (CRD) volumes and market share at Clearing Houses (CCPs) in 2Q 2023. All the charts and detail from CCPView. USD CDX, CDS and Swaptions CDX volumes significantly down compared to all the prior quarters shown. Market Share of USD CDX The upcoming ICE Clear Europe shutdown later in 2023, resulting in […]

New Block Trading Rules Will Now Start in December 2023

Those of you with long memories will recall a particular blog I wrote about Block Trading and new rules that were going to come into play: Those new rules could have come into play as early as March 2023, but they have been delayed until December 2023. As a result, we have just seen learnt […]

We Need to Talk About the Clarus API

Most of our readers come to the Clarus blog to receive new information from us. Whether that be on the data side (such as the monthly RFR Adoption Indicator) or about new regulations (such as Central Clearing of Bonds and Repos). But do our readers ever stop to consider which tools we use to deliver […]

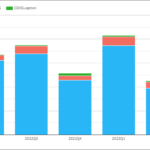

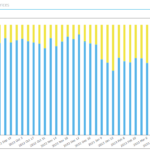

2Q23 CCP Volumes and Share in IRD

Clarus CCPView has daily volume and open interest data published by each CCP, which is filtered, normalised and aggregated to allow meaningful comparisons of volumes. Today we look at 2Q23 Volume and market share in IRD for: Onto the charts, data and details. Volumes and Market Share For major currencies and regions, vanilla swaps referencing IBORs and OIS […]

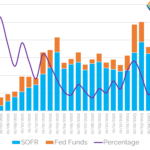

Bollinger, Greenspan and The Millennium Bug: LIBOR Is Now Dead

USD LIBOR is no more: I will likely never type US0003M into my Bloomberg ever again. I doubt many will shed a tear at the ultimate demise of LIBOR because: LIBOR – The Numbers This is as good a time as any to therefore pause and consider some of the things we saw in USD […]

The Latest on Canada and the Transition from CDOR to CORRA

ISDA recently published a very informative webinar on the CDOR Transition: From this, I learned that 30th June 2023 (i.e. Friday!) is a big day for Canada Rates markets. Succinctly, no more new CDOR trading should take place after this date, other than for some well-defined exceptions. The CARR website is a great resource (from […]