- Settle to Market is a recent innovation in derivatives trading.

- It has helped banks reduce regulatory capital and derivatives exposures.

- We look at STM in detail and compare it to collateralisation.

- The CFTC have also issued guidance on the subject.

What You Need To Know

Settle to Market (STM) treats Variation Margin at CCPs as settlement instead of collateral. This has the possibility of reducing Leverage Ratio costs and hence lowering regulatory capital charges.

STM featured in two of our most recent blogs on CEM and Swap Regulations. It first came to light when UBS reported a capital saving of $300m in August 2016, followed by huge drops in Derivatives exposures for BAML and Morgan Stanley.

STM helps to reduce balance sheet usage and probably simplifies life in the event of default.

The CFTC have requested that all CCPs in the US treat Variation Margin as STM.

What is Settle To Market?

Variation Margin on an OTC derivative may now be treated as cash-settling an outright exposure to zero every day, rather than collateralising a contract. Two new acronyms are introduced – CTM (collateralised to market) and STM (settle to market).

Collateralisation

CTM is the traditional trading model, where we calculate a mark-to-market value of an outstanding contract, and an out-of-the-money counterparty posts collateral to us. This is seen as a way of proving that a counterparty is good for the losses on the contract.

The collateral being posted does not expressly have to be in the same currency (or same asset class) as the underlying contract – it depends on our bilateral agreement.

Enter CCPs into the mix. A CCP must ensure that the collateral held against the current replacement cost of a member’s portfolio is accurate and sufficient in the event of default. If collateral (aka “variation margin” at a CCP) is in a different currency to the underlying portfolio, then a CCP is exposed to additional FX risk. Therefore, CCPs standardise Variation Margin flows, requiring that VM is posted to them in cash-only, and in the same currency as the underlying contract – e.g. if you trade HUF IRS, you have to post HUF cash as Variation Margin each day.

This does mean that CCPs (and their members) face the operational burden of processing flows in multiple currencies every single day. However, it significantly reduces the risk in event of default.

Settlement

With variation margin posted in the same currency as the derivatives and as cash-only, it is as if cash settlement of the underlying contract happens each day. Instead of treating this variation margin as reducing exposure to the counterparty (as collateralisation is designed to do), we could instead say that it extinguishes the exposure entirely.

The contract is effectively settled because the counterparty and market risks are realised at the time of payment.

This is similar to how I have always thought of futures markets working. When the exchange closes for the night, you have to cash-settle your outstanding contracts. Then, in the morning, the exchange effectively reinstate your positions from the previous night and you start again.

Discounting

For any long-dated contract, it is important what happens for each daily “settlement”. This will define how a contract is valued.

Consider the interest that is paid on collateral. The interest rate to be paid on collateral defines how the future flows of the contract should be discounted. Typically, this is OIS.

CCPs also pay OIS on variation margin, and therefore OIS discounting is the industry norm for cleared swaps. However, if a contract is cash-settled every night, what do we use for discounting?

PAA is the real innovation

The major CCPs must have surely realised that it would be beneficial if CTM and STM contracts were economically equivalent. That would allow a bank to offset the risks of a legacy CTM contract by trading a new STM contract. But how could that be achieved?

From my understanding of the literature, CCPs have chosen to embed the daily interest on collateral within the contractual cashflows of an Interest Rate Swap itself. From the CFTC response to CME:

Under the settled-to-market model, parties also exchange daily payments via their DCO. In order to fully replicate the economics of the collateralized-to-market model, parties under the settled-to-market model exchange payments of price alignment amount (“PAA”), which are equal to the PAI payments that they would exchange under the collateralized-to-market model.

Therefore, rather than being tied to the type or quantity of the collateral being posted, the interest is calculated using the mark to market of the swap each day, using a pre-defined rate within the swap contract. For this reason, rather than interest being paid on collateral being known as Price Alignment Interest at CCPs, this is known as the Price Alignment Amount (PAA) for STM contracts.

Why Do We Care?

Three reasons:

- Regulatory Capital

- Balance Sheet usage (accounting)

- Bankruptcy

The US Banking Agencies explicitly recognised the regulatory capital savings of STM in a letter here. At least UBS, BAML and MS have availed themselves of the benefits so far.

The SIFMA letter on STM from way back in December 2015 outlines these reg cap savings. Of course, you would be well served in reading our blog on the Current Exposure Methodology too.

From SIFMA:

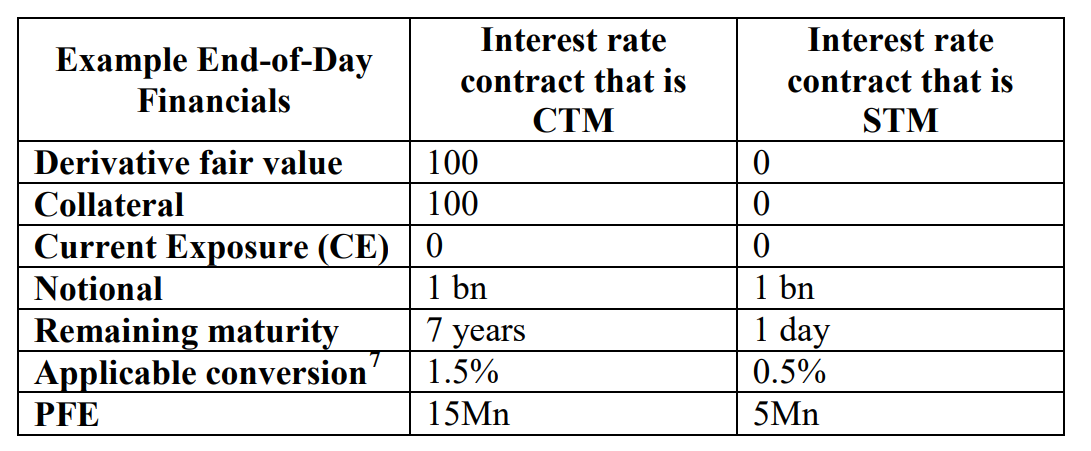

SIFMA are directly quoting Footnote 2 of the “infamous” add-on table in the Basel Current Exposure Methodology. This states that if the mark-to-market is reset to zero, then the effective maturity of that contract should be taken as the time to the next reset date. For STM contracts, that time to next reset is one day.

In terms of the impact on the computed Potential Future Exposures (PFEs) under CEM, this has a big impact in Rates markets.

From SIFMA, for Interest Rate Swaps, we can see up to a 66% reduction:

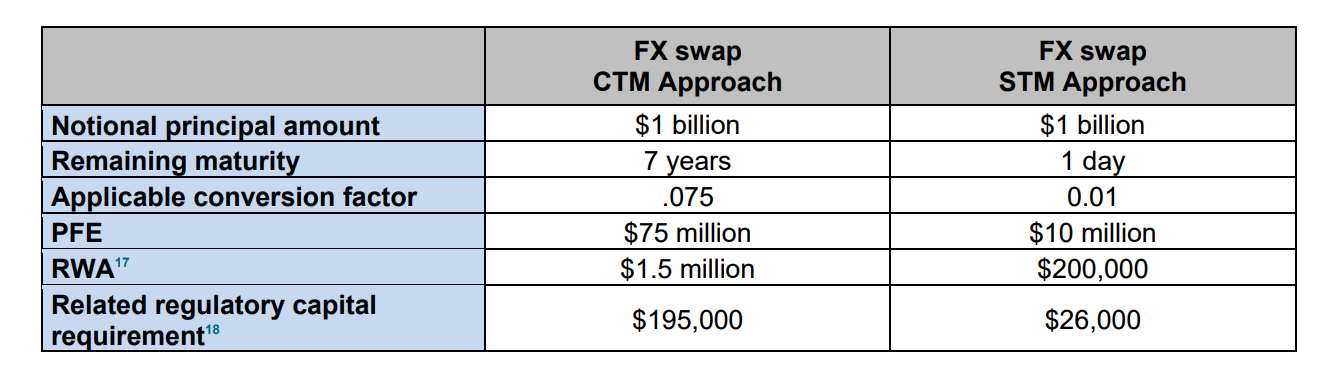

And from Davis Polk, the effect for any FX contracts can be even more profound – up to 87%!

And from Davis Polk, the effect for any FX contracts can be even more profound – up to 87%!

The ISDA accounting guidance here shows that STM removes the large balance sheet consumption of OTC derivatives. Rather than recording an asset (mark-to-market) versus a liability (pledged collateral), hopefully this means that a derivative can (rightly in my opinion) show a single value on the balance-sheet. SIFMA also cover this in their letter.

Finally, it is worth bearing in mind what happened when Lehman’s went bust in terms of “collateral”. Specifically, in the US a counterparty appears to have the right to terminate contracts and keep any pledged collateral! I imagine that in an STM world this is no longer possible.

The CFTC care about this too

This letter from the CFTC (in response to the CME) sets out that all DCOs (i.e. CCPs) should treat variation margin as settlement (STM) rather than collateral (CTM).

I found this circular on the LCH website that is a rulebook change in SwapClear marking all payments as “Settlement” for US Clearing Members.

I’ve also found reference to the fact that the CME changed “Rule 814” to state that:

All payments in satisfaction of outstanding exposure must be paid in cash or any other form of payment approved by the Clearing House Risk Committee; shall be settlement (within the meaning of CFTC Rule 39.14); and shall be final, irrevocable and unconditional…

UPDATE: Eurex also introduced STM back in November 2017.

Clarus Optimisation and Attribution

Clarus provide tools that streamline consumption of margin and capital. We provide calculators – such as CCP margin, SA-CCR, and ISDA SIMM – and the ability to optimize and attribute across all of these variables. STM is another piece of the puzzle towards full optimization.

From my research, I imagine that almost all USD swaps traded are now STM. I’m surprised it’s taken us this long to write about it!

Thanks Chris,

I think this is the rule change at Eurex.

https://www.eurexclearing.com/clearing-en/resources/circulars/EurexOTC-Clear–Amendments-to-the-Clearing-Conditions-of-Eurex-Clearing-AG-and-introduction-of-the-Settled-to-Market–STM–model-for-OTC-IRS-transactions/3244252

Just to be complete.

Brilliant, thanks. Will add into the main text as well so that people don’t miss it.