- LIBOR swaps traded on spread to US Treasury bonds make up about 70% of interdealer liquidity.

- The floating leg of these swaps is about to be discounted at SOFR.

- This could lead the Spreadover market to start trading versus the SOFR index itself.

- We look at the differences between a LIBOR spreadover and a SOFR spreadover trade.

With the upcoming switch from Fed Funds to SOFR discounting at CCPs, we have a change in the type of rate being used to discount USD interest rate swaps.

What does this mean for the largest pool of inter-dealer liquidity – the Spreadover, or Swap Spread, market?

Spreadovers

USD spreadovers account for about 70% of interdealer volumes. They perform a particularly important role:

- A spreadover links the price of deeply liquid US Treasury bonds to the interest rate swap market.

- They therefore allow dealers to translate liquidity from the cash bond market into the derivatives market.

Currently, virtually all USD Spreadovers have the following characteristics:

- A spot-starting USD swap.

- 3m USD LIBOR leg.

- Semi-bond convention on the fixed leg (30/360 semi-annual payments).

- Cleared at LCH SwapClear.

- PAI (the price alignment interest), commonly referred to as the interest paid on variation margin, is calculated at Fed Funds (EFFR).

However, over the next few months, Spreadovers are about to change. First up is the effect of the discount switch at CCPs.

Step One: Spreadovers after October 16th

After October 16th, the swap leg will subtly change. The interest rate used to calculated PAI (PAA in the case of an STM swap) will become USD SOFR.

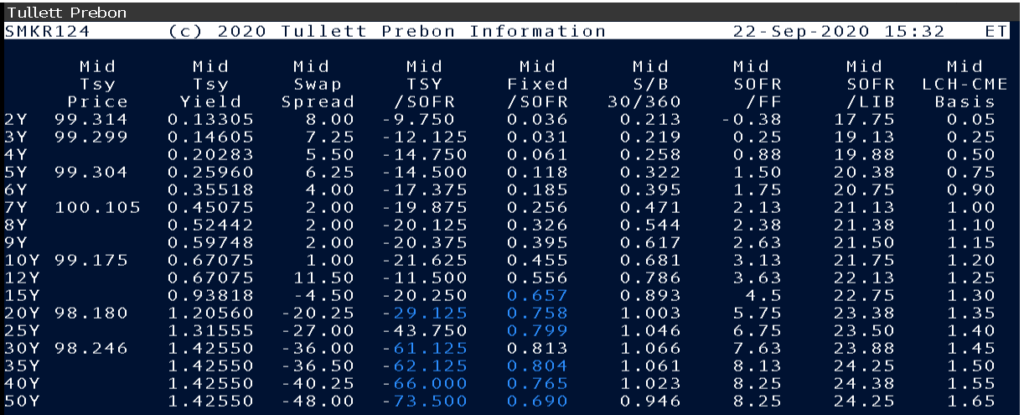

Popular screens used in the pricing of deals, such as ICAP 19901 and Tulletts SMKR99, will soon represent a different instrument. SOFR discounting will be the stated market convention.

The primary intention of these broker pages is clear. They provide transparency and accuracy over where market standard instruments are. This allows capital markets transactions, such as bond issues, to price efficiently. Certainly much more efficiently than if everyone is arguing about where the mid-market reference rate is. It is therefore vital that market participants understand the changes that are about to occur to the underlying transactions on these pages.

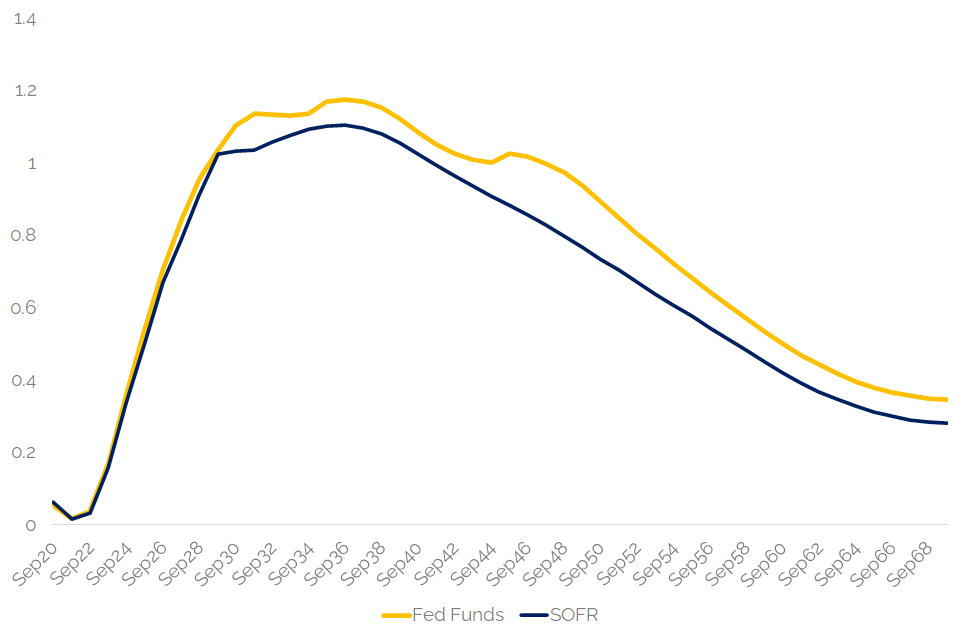

It may sound like a subtle change, but consider the potential difference in forwards on these discount curves. 30Y SOFR-Fed Funds basis last traded at over 8 basis points, implying quite a change in funding curves, particularly in forward space.

Step Two: Consider what a Spreadover currently represents

It is interesting to consider what a Spreadover represents in LIBOR space.

- The UST leg of a Spreadover represents the long-term cost of funds for the US government, as defined by the US Treasury yield.

- The swap leg reflects the interbank cost of borrowing short-term unsecured funds as defined by the LIBOR fixings.

- Therefore the difference between the two (i.e. the Spreadover) could be thought of as the difference between risk free borrowing (as defined by the US government) and the credit spread demanded to lend to a large financial institution (who could access long-term funds at LIBOR flat).

I like to think that this worldview was accurate, once upon a time. However, once the swap leg becomes either a) cleared or b) daily margined you can argue that we are looking at two very different financial instruments.

- The cost to a bank (who, along with hedge funds, are the only active users of spreadovers) of holding this contract becomes a very different animal.

- The mark to market of the swap must be funded daily.

- An off-balance sheet derivative (the swap leg) now attracts a cost of balance-sheet associated with the notional and maturity of the swap.

- The credit aspect of the series of LIBOR-linked flows completely changes. No longer are we entering into an uncollateralised derivative, but rather a daily series of collateralised flows with minimal credit exposure.

- The chances of holding a spreadover to maturity are very slim – the UST exposure will typically be rolled into the most liquid on-the-run bond, and the swap leg compressed away in Clearing.

All things considered, a modern Spreadover trade is therefore a world away from an actual expression of long-term credit funding versus the “risk free” curve.

We can tentatively define a spreadover under current conditions as:

- An expression of the cost of liquidity transfer from one pool of US Rates liquidity to another.

- The term cost of funding a collateralised derivatives exposure combined with the cost of holding a US Treasury bond.

- The relative credit spread of the US government to an over-collateralised (IM plus VM) derivatives contract at a CCP.

Step Three: What is a Spreadover vs SOFR meant to be?

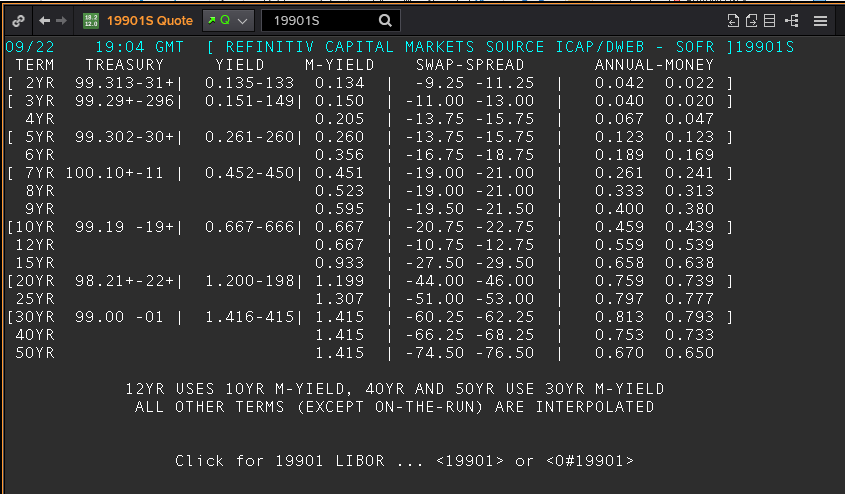

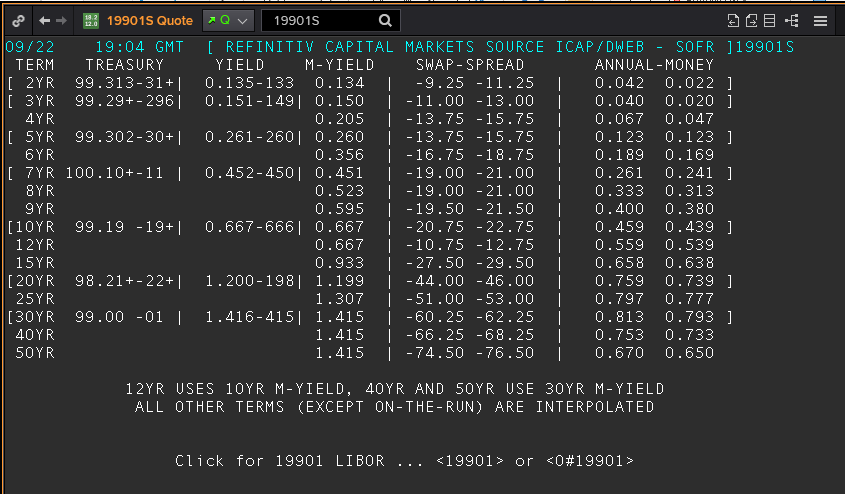

And now, added to this existential assessment of what a swap spread really represents, we introduce a brand new instrument. The swap is now done versus SOFR, as shown on the new ICAP page 19901S below:

If (when) liquidity transitions out of LIBOR products and into RFRs, Spreadovers may predominantly trade versus SOFR. This sounds like a fundamentally different product to the one used today.

A Spreadover traded with the swap versus SOFR has the following characteristics:

- The UST leg is identical to a spreadover vs LIBOR.

- The USD swap leg is still spot-starting.

- The SOFR leg is compounded in-arrears and paid annually.

- The fixed leg is paid on an Annual Act/360 basis (in a change to LIBOR standards).

- The swap will be typically cleared at LCH SwapClear (other CCPs can also clear the swap leg).

- PAI (the price alignment interest), i.e. the interest paid on variation margin, will be calculated at SOFR.

Now recall what SOFR actually is – an overnight cost of Repo.

So we are compounding the daily cost of Repo versus holding a UST that we could…repo out! If you take the cashflows of these actual trades, you could introduce a no-arbitrage argument to state the value of a Spreadover traded versus SOFR should always be zero. Irrespective of the term.

We are essentially stating that the Spreadover curve has become the term repo curve.

The Cost of Term Funding

From the ICAP screen we can see that the Spreadover curve versus SOFR is far from flat. It is deeply negative sloping:

30YR swap spreads are at -61 basis points! That is both:

- A large liquidity premium in USTs.

- A huge term premium for entering into a long-dated rolling repo contract!

I find this one of the most fascinating insights into how bank capital regulation, term funding and liquidity premiums can all combine to completely override the economic fundamentals of what a financial contract is meant to capture in its essence.

So I will leave our readers with one final question.

Would a cash-settled Spreadover contract trade at flat versus SOFR across the whole curve? Or are the supply/demand dynamics so severe that even a theoretically pure contract will deviate from its intended purpose?

Hey Chris, Just trying understand what you mean by spreadover. Is spreadover the same concept as an asset swap? If so are we talking coupon matched or matched maturity?

Yes same concept as an asset swap. A Spreadover is the standardised instrument that trades in the USD interdealer market. It is not quite either a matched maturity or a coupon matched package. It is an on the run UST, e.g. the current 10 year, versus a spot starting 10Y interest rate swap. So neither the coupons nor the maturities are exactly matched, but you are trading a package of the two benchmark instruments in the chosen maturity.

Thanks Chris – got it. The spread would be a proxy for risk free to bank credit.

Thanks Chris – got it. The spread would be a proxy for risk free to bank credit. What are the chances of the market quoting the spread without Libor?