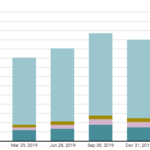

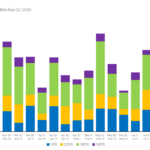

CCP Swap Volumes and Share – 2Q 2020

In today’s blog, I look at interest rate swap volumes and CCP market share in major currencies, focusing on 2Q 2020 and comparing QoQ and YoY figures. After the massive volatility and volume we saw in 1Q 2020, the most recent quarter was much quieter. Even so, there are interesting changes in volume and market […]

Margin Calls During COVID-19

John Maynard Keynes said in the 1930s; The market can stay irrational a lot longer than you can stay solvent. Keynes Since March 2020, the bounce-back in almost all “risky” assets since the nadir of the crisis has been breathtakingly sharp: Motivated by Amir’s blog last week on Initial Margin, I got to wondering how […]

CAD CORRA Futures and Swaps

We last covered CAD Rates Markets and CORRA Reform in Oct-19, so I wanted to look at what’s new and in particular the news that TMX launches CORRA Futures. Background on CORRA The Bank of Canada took over the calculation and publication of the Canadian Overnight Repo Rate (“CORRA”) on June 15, 2020 , subsequent […]

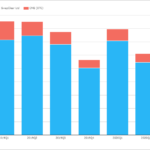

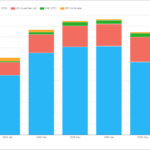

Clearing House Margin calls in Q1 2020

Clearing Houses have recently published data on the magnitude of margin calls they made in Q1 2020 and these are interesting to say the least. Given the massive price volatility we observed in March across all asset classes, we knew these were going to be big numbers, so let’s dive into the detail. Variation Margin […]

Swaps Data: Initial Margin Soars in Q1 2020

My monthly Swaps Review looks at Initial Margin requirements as disclosed in the recently published 1Q 2020 CPMI-IOSCO Quantitative Disclosures for CCPs, showing: The extent of the IM increases in Q1 2020 The wide variance by product class 23%, 46%, 66% for IRS, CDS, F&O respectively The wide variance between CCPs in the same product […]

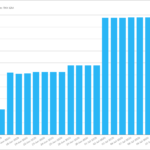

SONIA Q2 2020 Update

43% of GBP risk transacted in Q2 2020 was in SONIA. And only 24% of GBP notional was in LIBOR. Now that volatility has died down somewhat there is less short-dated trading activity. Can we consider the market standard as SONIA yet? The first Monday in March 2020 will likely be remembered for many reasons. […]

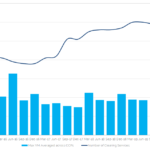

SOFR Futures and Swaps – June 2020

An update to SOFR Futures and Swaps – May 2020 Volume and Open Interest in SOFR Futures is down Swaps Volume also down, but OI is up US persons data shows activity recovering in June SEF volume remains much lower than Off SEF Clarus Data Products provide more insights Volumes and Open Interest In CCPView we can view both […]

LIBOR Discontinuation has been Preannounced

LIBOR will probably see an announcement towards the end of this year that it will be discontinued. This was announced by the FCA on 22nd June. This has moved markets already because it impacts the dates to be used to calibrate the fallback spreads. This means that we have already seen the last 6 month […]

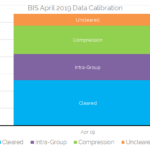

What Is the Total Size of Rates Markets?

Rates markets have grown to stand at over $350tn in monthly volumes. Our data product, CCPView, provides transparency data covering 93% of these global volumes on a daily basis. We benchmark our data versus periodic BIS data below. Data analysis needs to be timely and accurate. Contact us today for a CCPView subscription. During recent […]

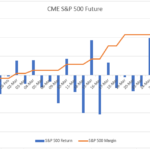

CME S&P 500 Futures Margins in March 2020

In a recent blog, procylical margins in the time of covid-19, I reproduced a chart from a BIS Bulletin showing that IM requirements for US Equity Index Futures doubled during March, the peak of the covid-19 market crisis. Today I will take a detailed look into these margin changes, concentrating on the S&P 500 index. […]